Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Bloom is stocked at 983 licensed dispensaries across California, New Mexico, and 14 other states, 353 of them in California, with the deepest coverage in Los Angeles, San Francisco, Long Beach, Sacramento, and San Diego. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

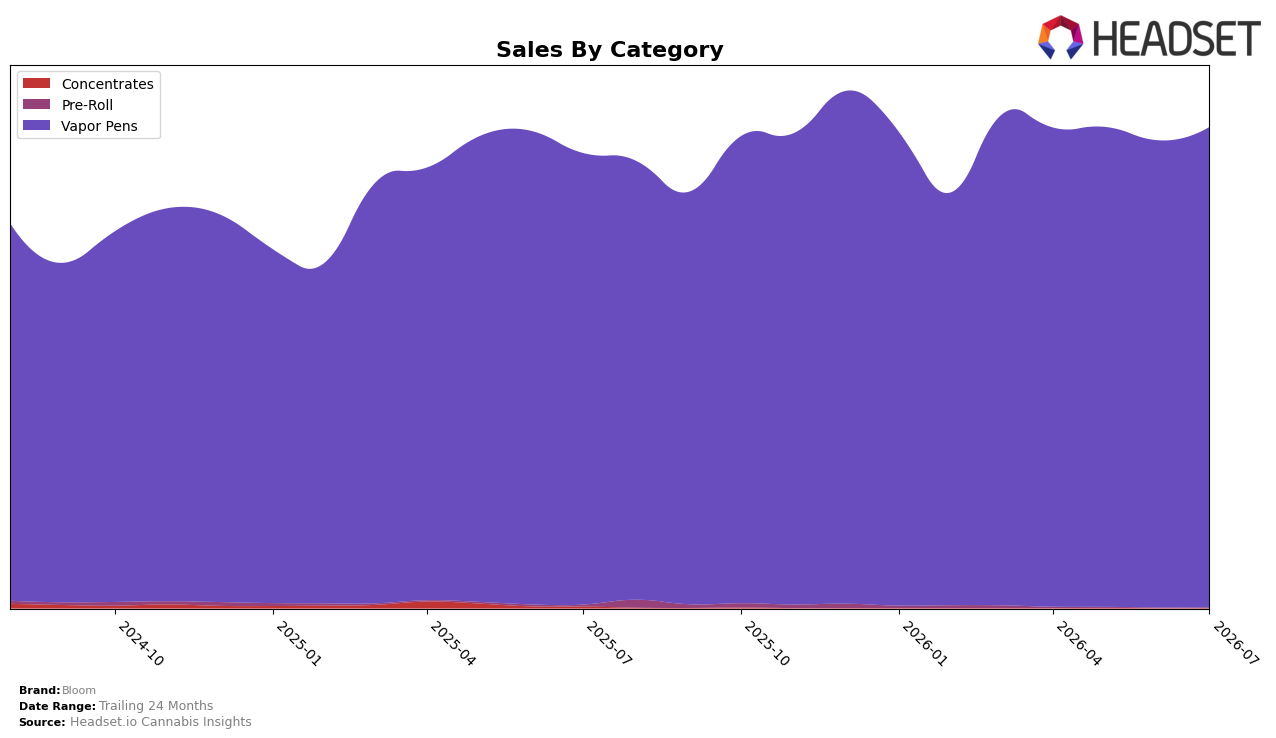

In July 2026, Bloom remained overwhelmingly concentrated in Vapor Pens at 99.94% share, with that core up 6.38% year over year and 2.82% month over month, while brand-level sales were up 5.74% YoY and average price fell 5.67% YoY to $30.24. Peripheral categories were de minimis: Pre-Roll held 0.04% share with a 19.25% MoM uptick but an 88.28% YoY decline, and Concentrates sat at 0.02% share with a 92.45% YoY drop and no MoM datapoint. The pattern implies category monoline behavior where Vapor Pens growth is doing the heavy lifting and price compression is being used to protect share rather than diversify mix.

Given a Vapor Pens rank of 10 in Illinois and a 2.82% MoM lift in the core alongside a 19.25% MoM bounce in a tiny Pre-Roll base, Bloom’s positioning skews toward defending a top-10 pen slot rather than building secondary pillars. With 6.38% YoY category growth outpacing the 5.74% total-brand YoY and a 0.00–0.04% tail in other formats, the portfolio signals specialization that can win on depth but risks sensitivity to Vapor Pens pricing cycles. The implication is to leverage Vapor Pens strength to sustain rank while using selective, low-cost tests in adjacent formats to reduce overdependence without diluting the 99.94% core.

Competitive Landscape

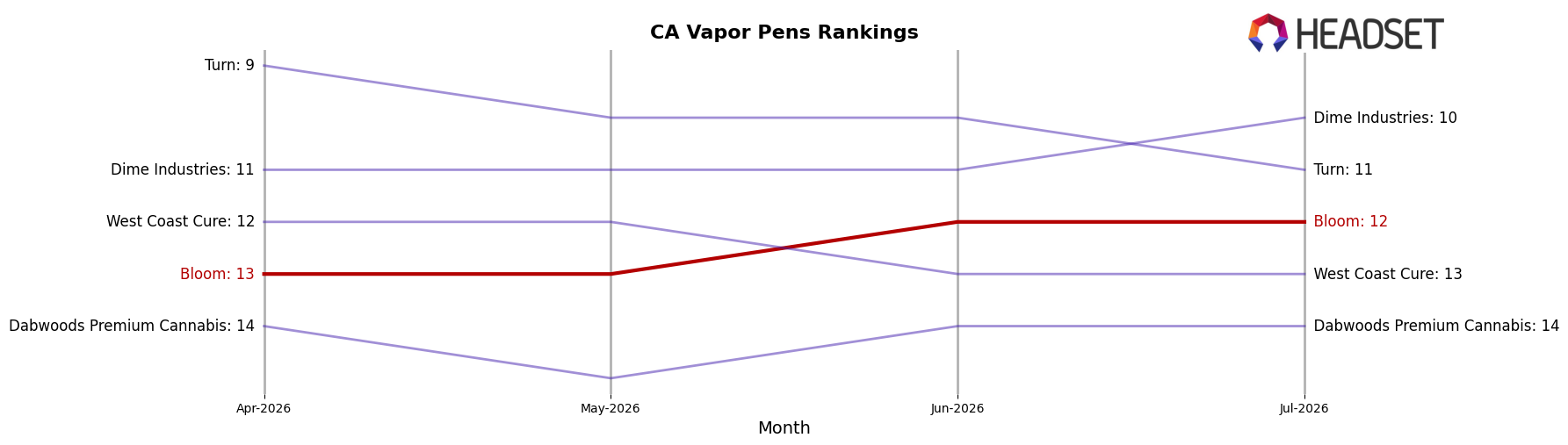

Bloom ranks #12 in California Vapor Pens in July 2026, improving 4 positions year over year from #16, and edging 1 spot ahead of its April 2026 standing at #13; this puts the brand at its peak rank of #12 while category leaders remain entrenched, with STIIIZY steady at #1 despite a -6.8% YoY sales change and Jetty Extracts climbing from #4 to #3 on 41.7% YoY growth. In contrast, Plug Play slipped from #3 to #4 with an -8.5% YoY decline while Raw Garden held #2 with a 4.6% YoY gain, indicating Bloom’s upward movement is occurring amid mixed competitor momentum. The pattern implies Bloom’s rank trajectory is one of incremental share capture against softening from some incumbents, but sustaining gains will require outpacing fast risers like Jetty Extracts rather than merely benefiting from rivals’ declines.

Notable Products

Maui Wowie Distillate Disposable (1g) posted the steepest decline at -13.8% month over month while sitting at rank 7, contrasting with Classic - Maui Wowie Live Resin Surf Disposable (1g) up 31.1% at rank 1. Classic - Blue Dream Live Resin Surf Disposable (1g) advanced 22.6% at rank 4 versus Pineapple Express Distillate Surf Disposable (1g) rising 17.1% at rank 3, signaling that Live Resin Surf formats are outpacing distillate variants in velocity. Nine of the top ten are Vapor Pens, and Live Resin Surf SKUs occupy three of the top four ranks, which implies the product mix is consolidating around premium Live Resin Surf devices as Bloom shifts emphasis toward higher-traction formulations.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.