Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Amber is stocked at 109 licensed dispensaries across Ohio, Colorado, and 9 other states, 37 of them in Ohio, with the deepest coverage in Marietta, Cincinnati, Cleveland, Columbus, and Dayton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

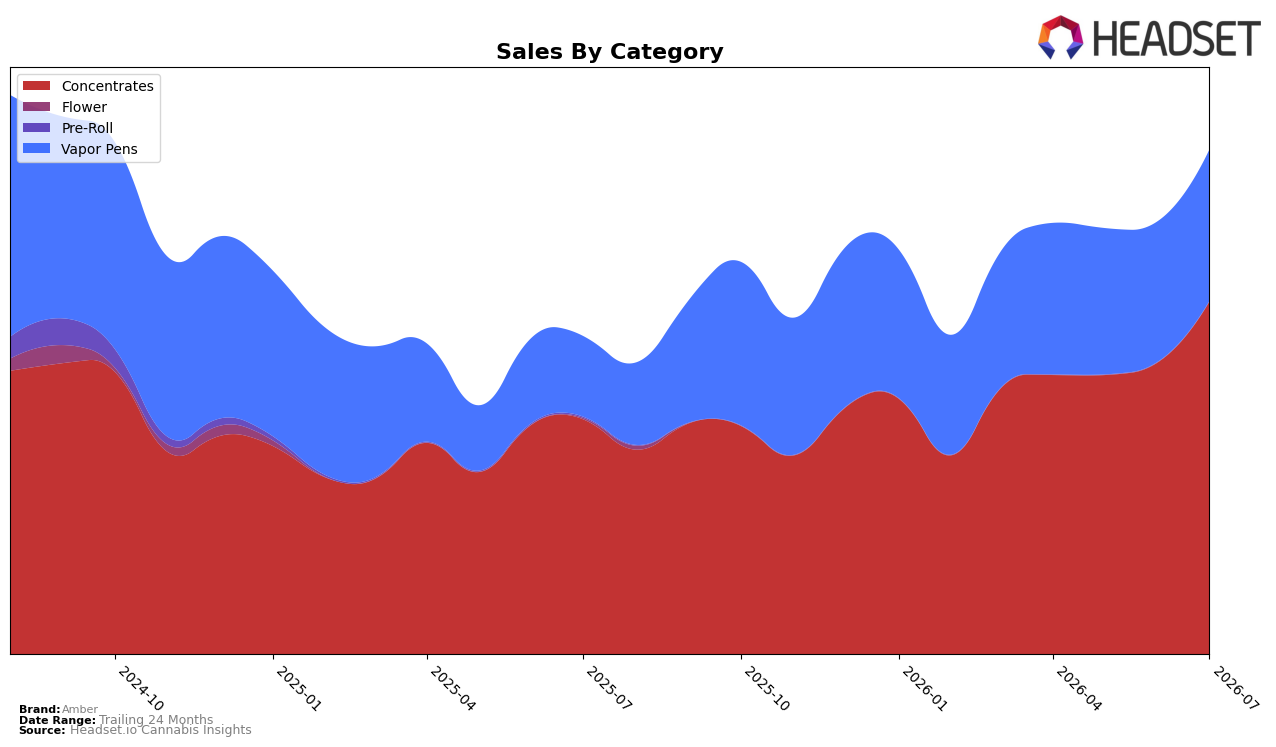

Amber’s July 2026 mix concentrated 69.97% of sales in Concentrates and 30.03% in Vapor Pens, with Concentrates up 50.24% year over year and 20.82% month over month while Vapor Pens rose 88.10% year over year and 7.74% month over month; the overall brand advanced 58.90% year over year alongside a 1.81% decline in average price. With Concentrates holding rank 1 in Colorado and Vapor Pens growing share without overtaking the core, the pattern implies Amber is extending into higher-price formats while protecting a category leadership base.

The combination of a 20.82% month-over-month surge in Concentrates and an 88.10% year-over-year lift in Vapor Pens, paired with a 1.81% average price contraction against a $13.84 ticket, implies volume-led expansion where Vapor Pens act as an acquisition wedge and Concentrates sustain repeat depth. Given the 69.97% to 30.03% mix split and rank 1 position in Colorado Concentrates, the mix shift points to defensible leadership anchored in Concentrates with strategic spillover into Vapor Pens to diversify revenue without diluting the core.

Competitive Landscape

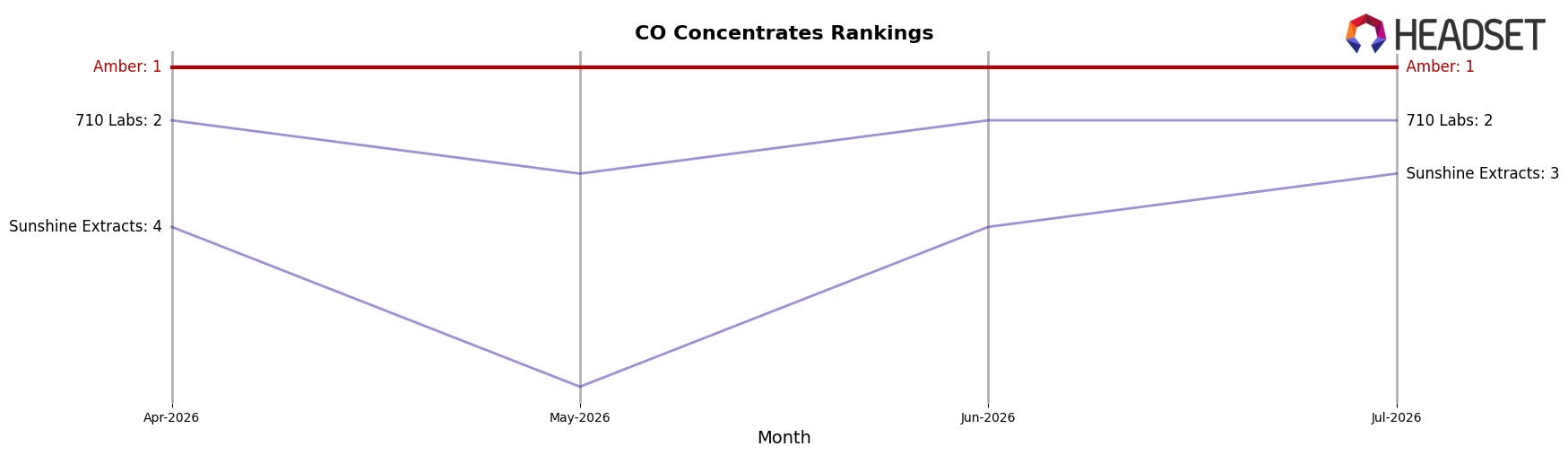

Amber is ranked #1 in CO Concentrates in July 2026, unchanged from #1 in July 2025, and it also held #1 three months ago, indicating a flat rank trajectory at the top while peers shifted beneath it; 710 Labs remains at #2 year over year with sales up 22.7%, whereas Sunshine Extracts climbed from #8 to #3 on 43.4% YoY growth, outpacing Spectra which slipped from #3 to #4 with a 10.4% decline. With Amber stationary at #1 while a challenger moved five ranks and another contracted, the pattern implies Amber’s leadership is durable but increasingly exposed to fast-rising competitors that can compress share without dislodging rank.

Notable Products

Ky Jealous Wax (4g) delivered the standout move in July 2026 with a +139.9% month-over-month surge to rank 1, while Honey Child Wax (1g) followed with a +136.5% jump at rank 2, and Sumo Grande Wax (1g) contrasted sharply with a -56.5% drop at rank 8. Chemdawg Wax (1g) inched up just +0.9% at rank 4, and eight of the top ten are Concentrates SKUs, concentrating revenue into a narrow form factor that heightens volatility on individual launches and discounts. The pattern implies Amber is leaning into higher-weight or promo-activated Concentrates to capture share quickly, accepting sharper troughs on legacy SKUs as attention and inventory cycle toward a few spike-prone items.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.