Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Green Dot Labs is stocked at 317 licensed dispensaries across Colorado, Arizona, and Oklahoma, 253 of them in Colorado, with the deepest coverage in Denver, Colorado Springs, Aurora, Boulder, and Pueblo West. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

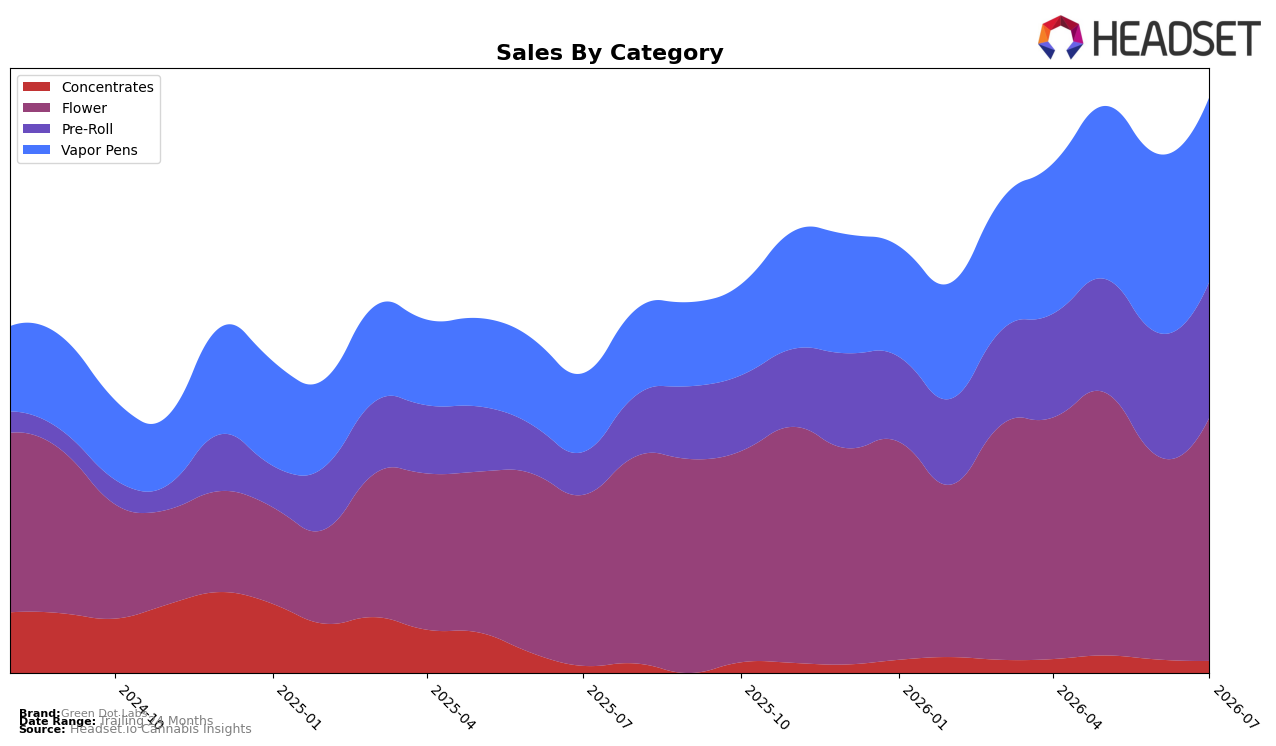

Green Dot Labs concentrated 37.83% of July 2026 sales in Flower with 32.85% year-over-year growth and 15.88% month-over-month expansion, while Vapor Pens held 30.24% share on 82.50% YoY growth and a 2.59% MoM uptick; Pre-Roll climbed to 23.93% share with 100.51% YoY and 7.16% MoM, as Concentrates slipped to 8.00% share with 8.72% YoY and a -2.17% MoM decline. With average price down 10.13% YoY to $31.11 alongside a 55.43% YoY brand sales increase, the mix shift toward lower-priced, faster-growing Pre-Roll and Vapor Pens implies volume-led scaling rather than price-driven gains.

Flower remains the anchor at 37.83% share yet is increasingly flanked by faster-growing Pre-Roll at 100.51% YoY and Vapor Pens at 82.50% YoY, indicating a pivot toward formats that typically favor repeat purchase and basket attachment, while Concentrates’ -2.17% MoM indicates under-allocation amid shifting consumer preference. Holding rank 4 in Flower in Colorado while shifting mix toward Pre-Roll and Vapor Pens suggests a hedge: defend core Flower position with 15.88% MoM momentum, but prioritize wallet-share capture in value-accessible formats where price elasticity (10.13% YoY price decline) converts into share gains.

Competitive Landscape

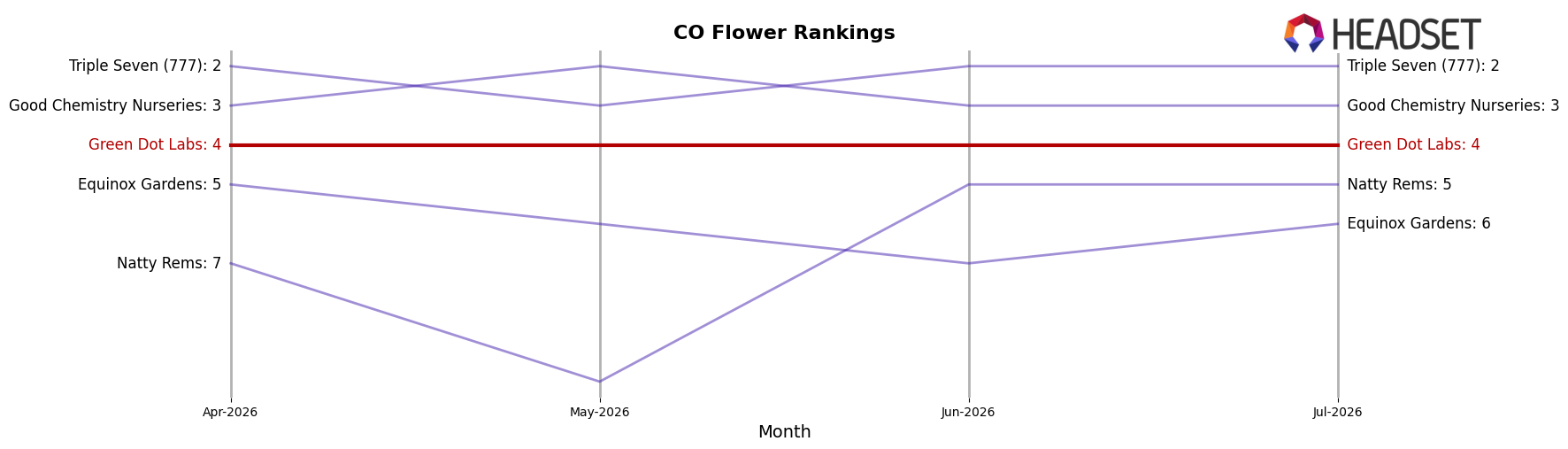

Green Dot Labs sits at rank #4 in Colorado Flower for July 2026, unchanged from #4 year over year, after peaking at #3 in January 2026 and holding #4 for the past three months, while category leadership shifted as Seed & Strain Cannabis Co. moved up from #2 to #1 and Good Chemistry Nurseries slid from #1 to #3 alongside an -8.7% YoY sales decline; meanwhile, Triple Seven (777) advanced from #3 to #2 with +56.8% YoY growth and Natty Rems surged from #23 to #5 on +168.5% YoY, indicating that Green Dot Labs’ static #4 amid upward moves by adjacent rivals points to a stable but compressing competitive position that will likely require share capture to avoid being bracketed by faster-rising peers.

Notable Products

Otoro Pre-Roll (1g) delivered the standout movement in July 2026 with a 189% month-over-month surge that vaulted it to rank 1, while Black Label - Bicycle Day Pre-Roll (1g) fell 40% to rank 7. Black Label - A5 Wagyu Pre-Roll (1g) inched up 12% to rank 3, and nine of the top ten SKUs were Pre-Rolls, indicating a concentrated tilt toward this form factor. Monet (3.5g) held rank 9 as the lone Flower SKU among the leaders with $93,922 in sales, reinforcing the imbalance toward Pre-Rolls. The pattern suggests Green Dot Labs is consolidating demand around Pre-Rolls, using breakout winners to earn top-tier shelf positions while Flower plays a secondary, selectively supported role.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.