Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

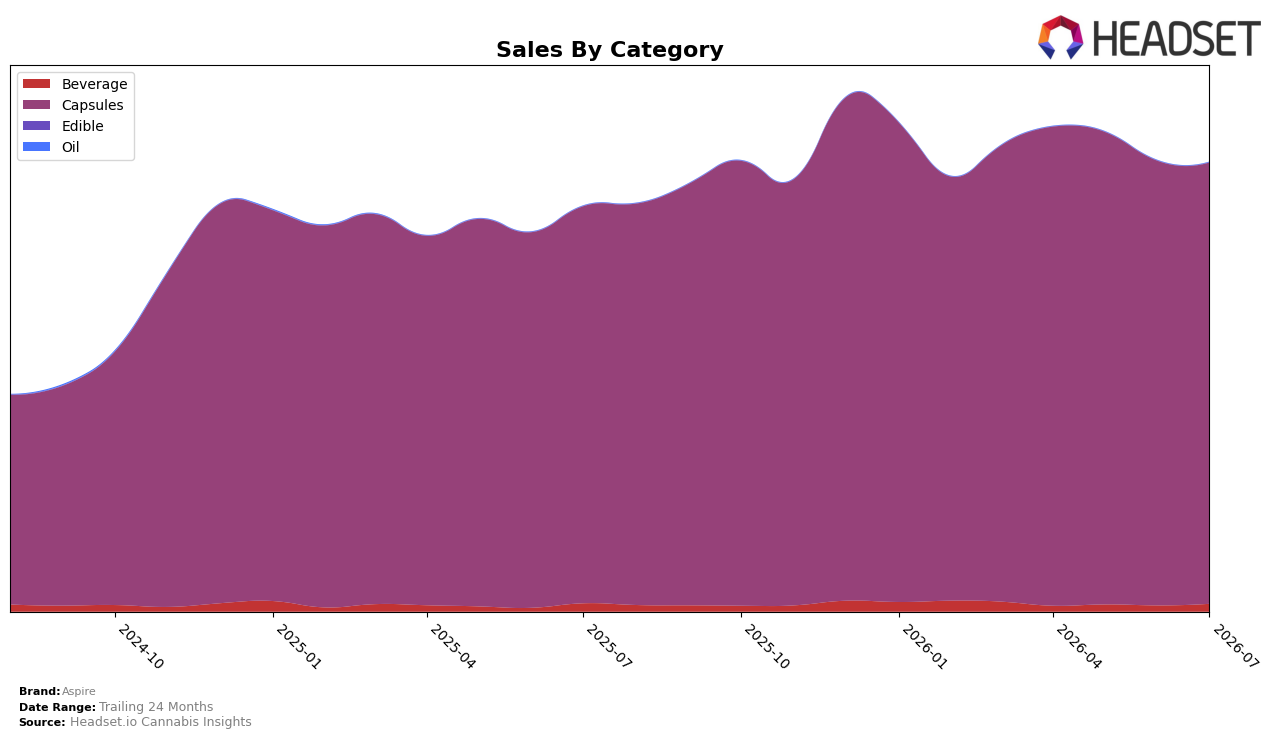

Aspire’s mix in July 2026 is concentrated in Capsules at 98.34% share with 11.18% year-over-year growth, while Beverage holds 1.66% share with a -6.53% year-over-year change; the month-over-month split tightened as Capsules slipped -0.70% and Beverage rose 26.88%. Average price climbed 12.49% year over year to $38.05, with Capsules priced at $38.89 versus Beverage at $16.69, and Aspire held rank 1 in Capsules in Ontario; the pattern implies the brand is consolidating leadership around a premium Capsule core while tolerating a small, volatile Beverage fringe.

The combination of a 98.34% Capsule share and a -0.70% Capsule month-over-month change alongside a 26.88% Beverage month-over-month lift suggests incremental trial is occurring in adjacent formats without diluting the Capsule engine. With Capsules growing 11.18% year over year as Beverage contracted -6.53% year over year, and rank 1 in Capsules in Ontario, Aspire’s positioning skews toward defensible premium utility where price elasticity supports a 12.49% annual price increase, implying near-term headroom in Capsules and a test-and-learn posture in Beverage.

Competitive Landscape

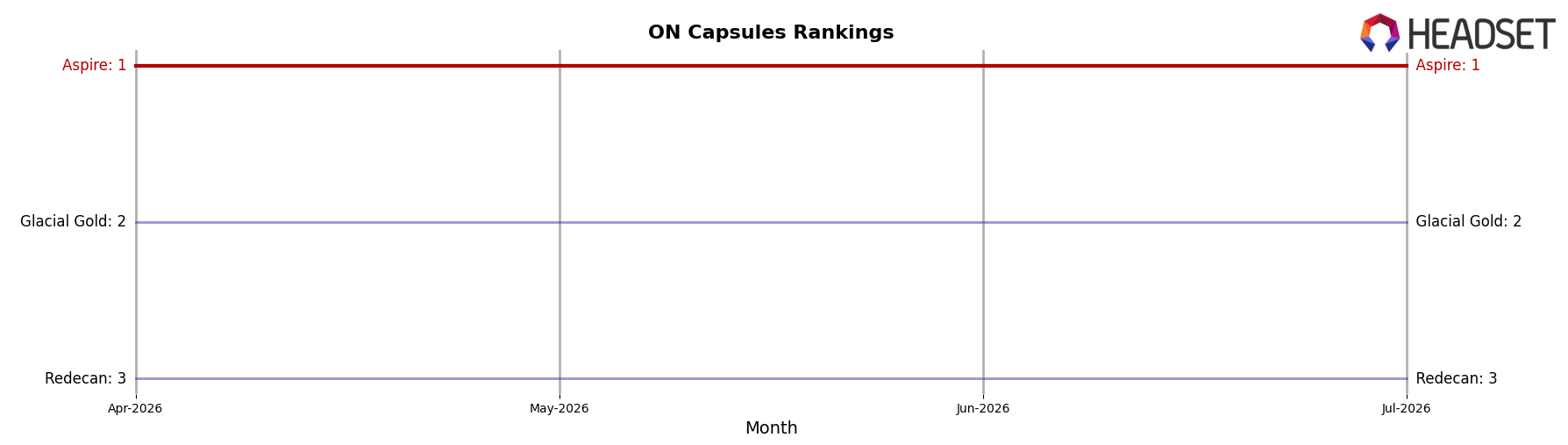

Aspire is ranked #1 in ON Capsules in July 2026 and held #1 a year ago, while Glacial Gold moved from #4 to #2 and Redecan slid from #2 to #3; this stability at #1 versus a +2 rank climb for Glacial Gold and a -1 rank drop for Redecan, alongside Glacial Gold’s 78.1% year-over-year sales growth and Redecan’s -34.7%, indicates Aspire’s leadership is steady but the competitive pressure is tightening from below, implying future defenses should anticipate an accelerating challenger rather than broad category churn.

Notable Products

SPARK THC Moonrocks Tablets 15-Pack (150mg) posted the steepest July 2026 decline at -12.5% MoM while sliding to rank 4, and Spark THC Moonrocks Live Rosin Reserve Capsules 30-Pack (300mg) also fell -9.2% at rank 1; in contrast, Spark THC Moonshot (100mg THC, 90ml) jumped +33.1% at rank 7. Six of the top ten are Capsules, concentrated across ranks 1 through 6, yet the lone Beverage winner advanced faster than any Capsule mover, implying early traction outside the core format that could diversify revenue risk.

Spark THC Moonrocks Capsules 50-Pack (500mg) in rank 2 grew +6.7% MoM while SPARK THC Rocket Moonrocks Capsules 100-Pack (1000mg) at rank 3 rose +5.7%, but CBD/THC 1:1 Spark Moonrocks Live Rosin Reserve Capsules 30-Pack (300mg CBD, 300mg THC) dropped -14.9% at rank 6 despite $19,420 in sales. With Capsules still occupying 80% of top-10 slots but mixed momentum across THC-only and 1:1 variants, the product mix points to Aspire leaning on high-dosage THC Capsule incumbents while selectively testing beverages as the next growth lane.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.