Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

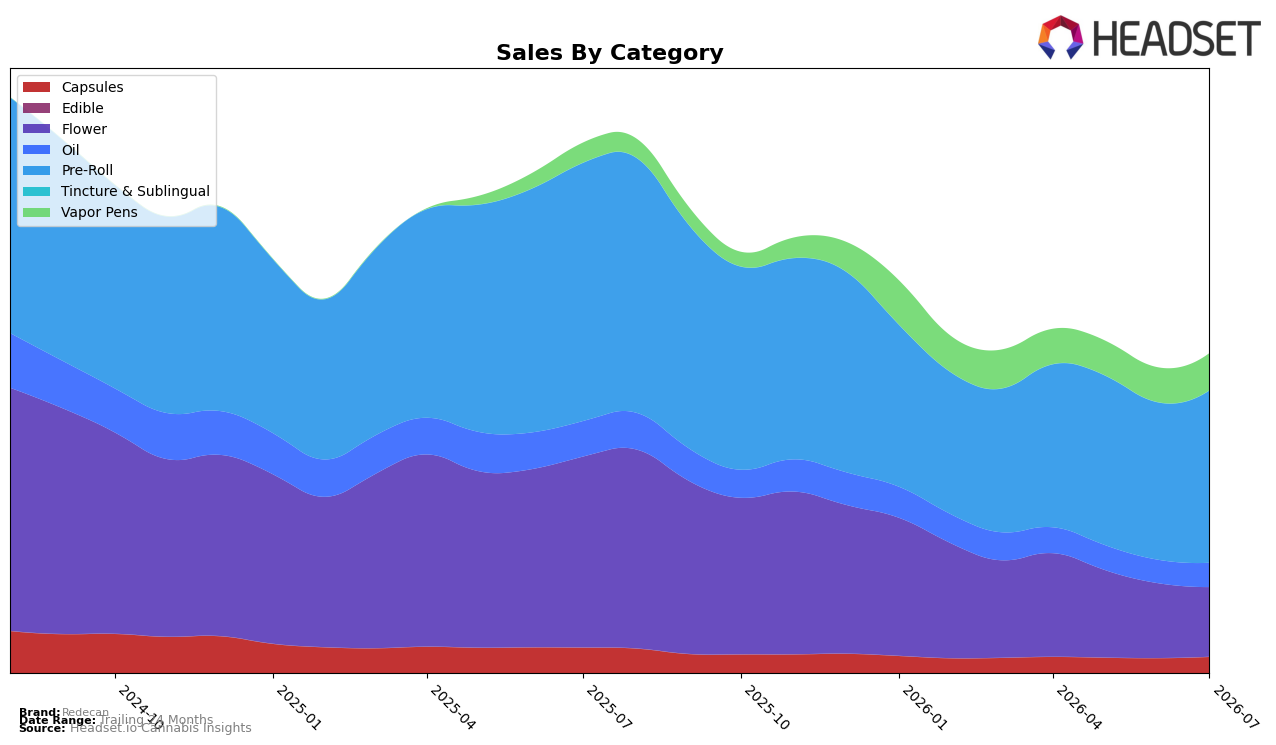

Pre-Roll expands to 53.99% share in July 2026 with month-over-month growth of 9.52% despite a year-over-year decline of 33.30%, while Flower contracts to 21.79% share with a 6.95% MoM drop and a 63.59% YoY slide. Vapor Pens rises to 11.59% share on 6.64% MoM and 85.83% YoY growth, and Capsules inches to 5.07% share with 8.73% MoM despite a 36.56% YoY decline; Oil holds 7.55% share with 3.68% MoM and a 31.80% YoY decrease. Average price edges down 0.84% YoY to $26.86 as Pre-Roll averages $23.79 and Vapor Pens sits at $41.60, indicating a mix shift toward higher-priced inhalables without price-led expansion. The pattern implies Redecan is consolidating around inhalables: Pre-Roll remains the volume anchor while Vapor Pens supplies the growth leg, offsetting Flower attrition but not fully reversing the brand’s 39.80% YoY sales decline.

With Pre-Roll still the top category yet down 33.30% YoY and Flower down 63.59% YoY, the tilt toward Vapor Pens’ 85.83% YoY growth and 6.64% MoM suggests the brand is migrating demand to formats that can carry higher price points without broad discounting, as average price is only down 0.84% YoY. Capsules’ 8.73% MoM and Oil’s 3.68% MoM increases provide stability while share concentrates in inhalables to 65.58% combined, and Pre-Roll’s 9.52% MoM rebound indicates near-term traction. The implication is a positioning pivot: maintain scale in Pre-Roll to preserve reach while using Vapor Pens’ momentum to rebuild premium perception and margin, accepting a smaller Flower footprint as a trade‑off for a more defensible, inhalables-led mix.

Competitive Landscape

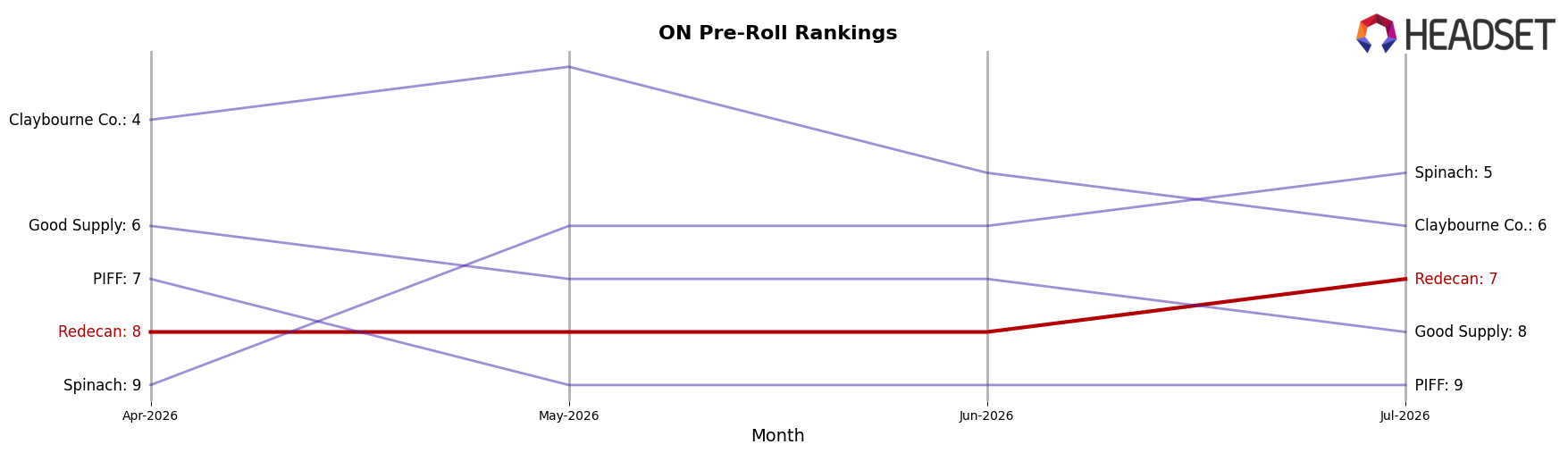

Redecan sits at rank #7 in ON Pre-Roll for July 2026, down 2 positions from #5 in July 2025, with a modest uptick from #8 in April 2026 yet still below its peak of #4 in November 2025; meanwhile, Back Forty / Back 40 Cannabis advanced from #2 to #1 as of July 2026 and Spinach rose from #14 to #5 on 65.34% YoY sales growth, outpacing Redecan’s trajectory. General Admission slipped from #1 to #2 alongside a 23.22% YoY sales decline and Thumbs Up Brand climbed from #9 to #4 with 52.75% YoY growth, signaling that Redecan’s two-rank YoY drop amid competitors climbing multiple positions implies share is concentrating among faster-rising rivals and Redecan’s current path risks further relative displacement without a pivot.

Notable Products

Animal Rntz (3.5g) posted the steepest decline in July 2026 at -9.1% MoM while sliding to rank 7, whereas Redees - Cold Creek Kush Pre-Roll 10-Pack (3.5g) gained 15.6% MoM and held rank 9. The flagship Redees - Cold Creek Kush Pre-Roll 10-Pack (4g) rose 13.3% MoM at rank 1, and Redees - Purple Churro Pre-Roll 10-Pack (4g) advanced 12.6% MoM at rank 3. Pre-Rolls account for eight of the top ten SKUs, with ranks 1 through 4 and 6 and 9 occupied by the format, and the top two SKUs together generated $1.65M. The pattern implies Redecan is concentrating demand into multi-pack Pre-Rolls while single-strain Flower like Animal Rntz loses share, signaling a shift toward value-oriented, repeatable formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.