Where to Buy

Canna Club is stocked at 18 licensed dispensaries across Colorado, with the deepest coverage in Denver, Colorado Springs, Durango, Fort Collins, and Golden. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

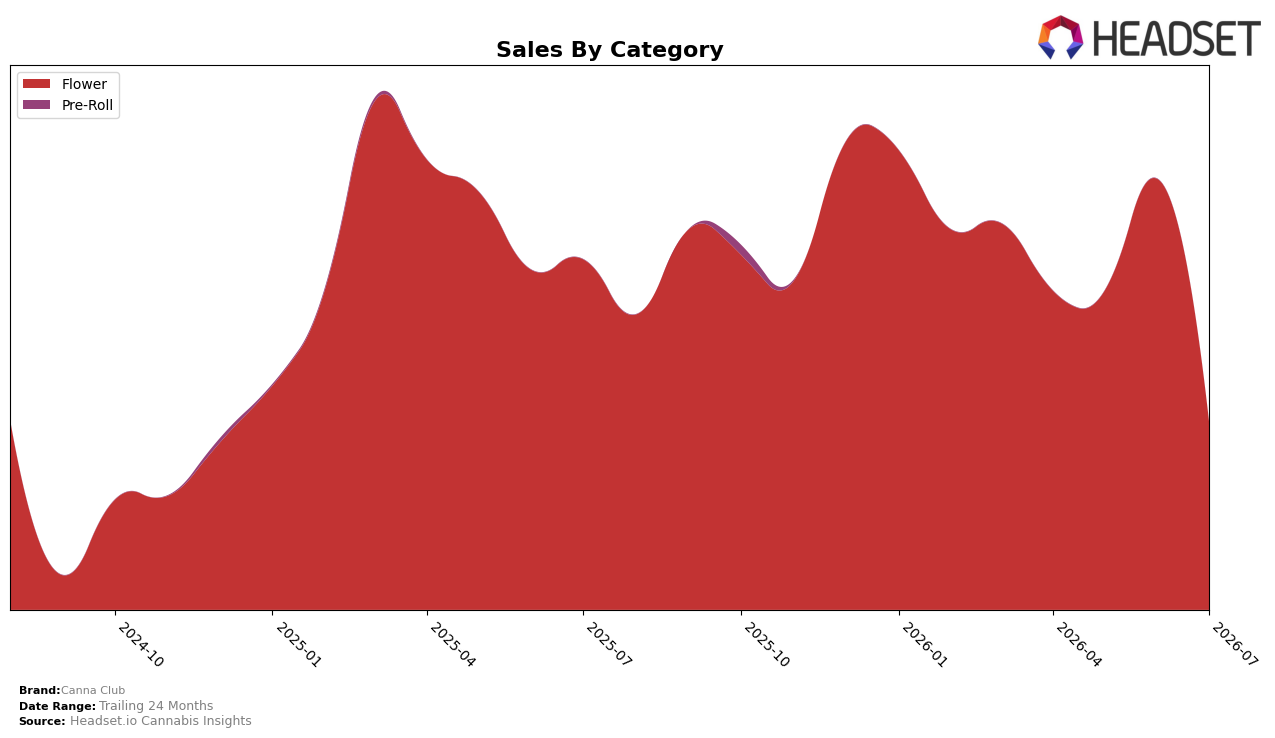

Canna Club operated as a single-category brand in July 2026, with Flower at 100.0% of mix and a month-over-month sales change of -56.44% alongside a year-over-year decline of -46.47%. Average price rose 59.23% year over year to $11.42 while unit-driven volume likely fell, and Flower’s rank in Colorado placed at 41 within Flower, signaling share contraction despite a 24‑month sales change of 1.88%. The pattern implies a price-led repositioning in Flower that compressed velocity faster than mix could diversify, concentrating risk in a single category while sliding in rank.

With 100.0% of sales tied to Flower and a rank of 41 in Colorado, the 56.44% month-over-month drop combined with a 46.47% year-over-year decline suggests Canna Club is trading margin for velocity, as a 59.23% price increase outpaced consumer tolerance and hindered repeat purchase. The 1.88% 24‑month gain against the current month’s contraction indicates an eroding base, implying that without mix expansion beyond Flower or recalibration of price architecture, the brand’s positioning will skew toward a narrower, lower-frequency buyer segment and leave it vulnerable to further rank slippage.

Competitive Landscape

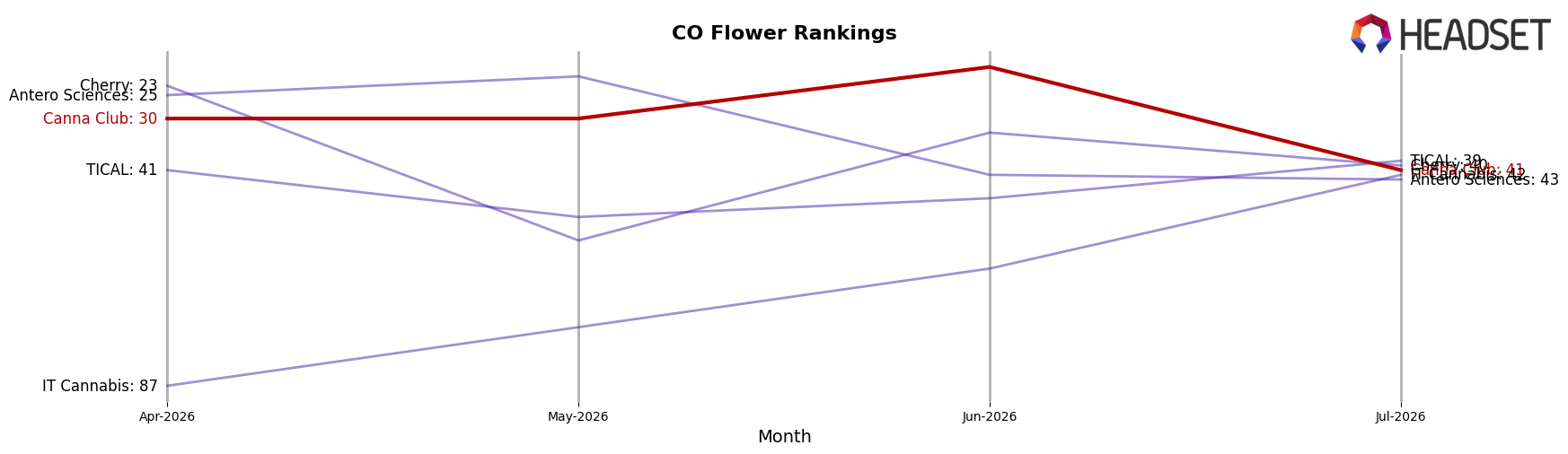

Canna Club sits at rank #41 in CO Flower in July 2026, sliding 11 positions YoY from #30, and down 11 positions versus April 2026’s #30, while still well below its March 2025 peak of #16 and 25 spots off that high; in contrast, Seed & Strain Cannabis Co. advanced from #2 to #1 with 76.2% YoY sales growth, and Natty Rems climbed from #23 to #5 alongside a 168.5% YoY increase, indicating Canna Club’s relative demand share has diluted as faster-rising peers compress its rank bandwidth and imply a need to reset velocity drivers to avoid further mid-tier drift.

Notable Products

MAC #1 (Bulk) posted the steepest decline in July 2026, falling 88.7% month over month while still holding rank 2, signaling a sharp pullback in bulk Flower even as it remains a top seller. Rainbow Zoap Popcorn (3.5g) at rank 1 also contracted 44.0% MoM, and Banana OG (7g) at rank 3 slid 25.7%, indicating that the top three positions were driven by units with double-digit declines rather than rising demand. Eight of the top ten are Flower SKUs, with two Banana OG formats present, pointing to SKU breadth within a single category rather than diversification, and the lone raw dollar anchor is Banana OG (7g) at $13,323. The pattern implies Canna Club is leaning into Flower variety while absorbing price or velocity pressure, suggesting a need to rebalance toward fewer, faster-moving Flower SKUs or adjacent categories to stabilize MoM volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.