Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Ceres is stocked at 257 licensed dispensaries across Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Olympia, and Bellingham. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

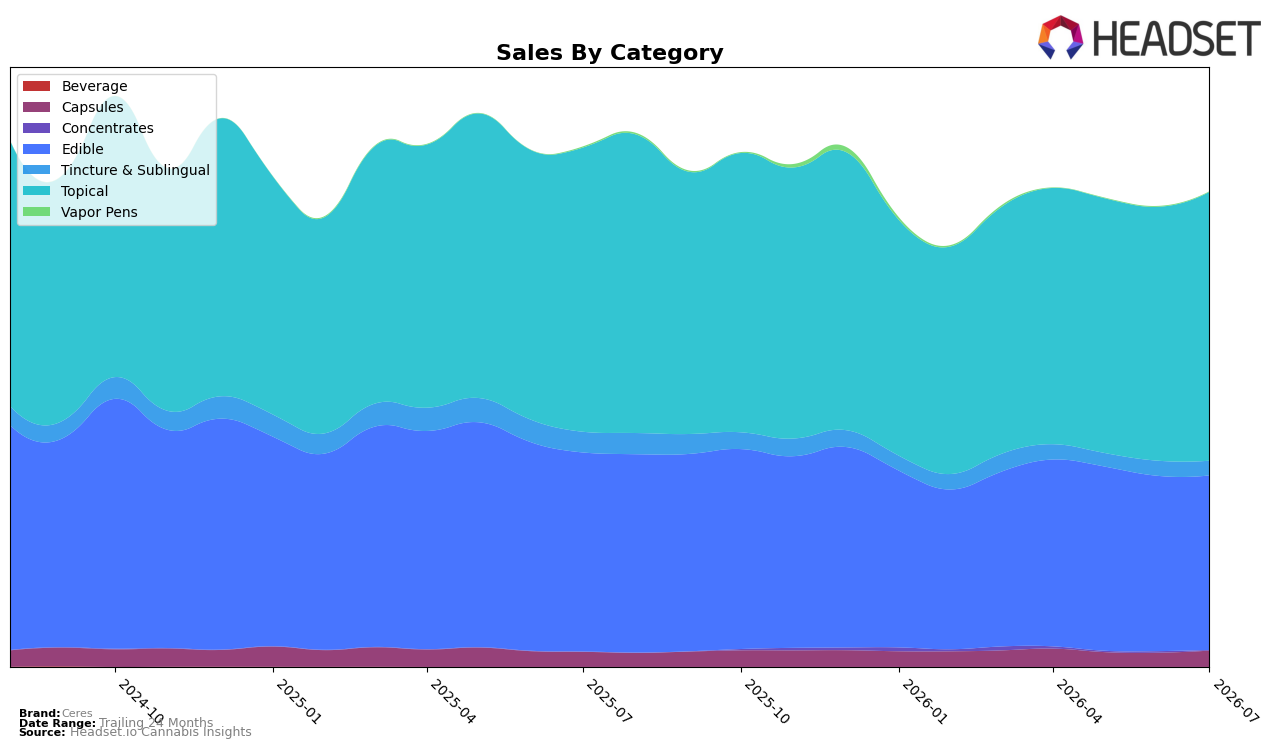

Ceres concentrated 56.66% of July 2026 sales in Topical, where year-over-year declined 5.44% but month-over-month rose 5.87%, while Edible at 36.78% fell 12.29% YoY and 0.40% MoM. Smaller lines moved unevenly: Capsules at 3.39% climbed 8.42% YoY and 15.09% MoM, Tincture & Sublingual at 3.04% contracted 29.51% YoY and 3.02% MoM, and Vapor Pens at 0.07% sank 62.17% YoY and 40.38% MoM. Despite a brand-level sales decline of 8.66% YoY alongside a 2.83% YoY rise in average price, the Topical-heavy mix plus Capsule momentum signals a shift toward format-specific resilience that can buffer volatility elsewhere.

With Topical anchored at rank 1 in Washington and expanding 5.87% MoM against a 12.29% YoY drop in Edible, the portfolio is tilting toward a defensible core rather than broad-category breadth. The 15.09% MoM lift in Capsules alongside a 29.51% YoY pullback in Tincture & Sublingual implies consumers are consolidating around easy-dose and wellness-adjacent formats, while the 40.38% MoM contraction in Vapor Pens after a 62.17% YoY slide reduces exposure to high-churn segments. The pattern implies Ceres’s positioning in July 2026 is to lean into Topical leadership while using Capsules as a secondary growth vector to offset persistent drag from Edible and Tincture & Sublingual.

Competitive Landscape

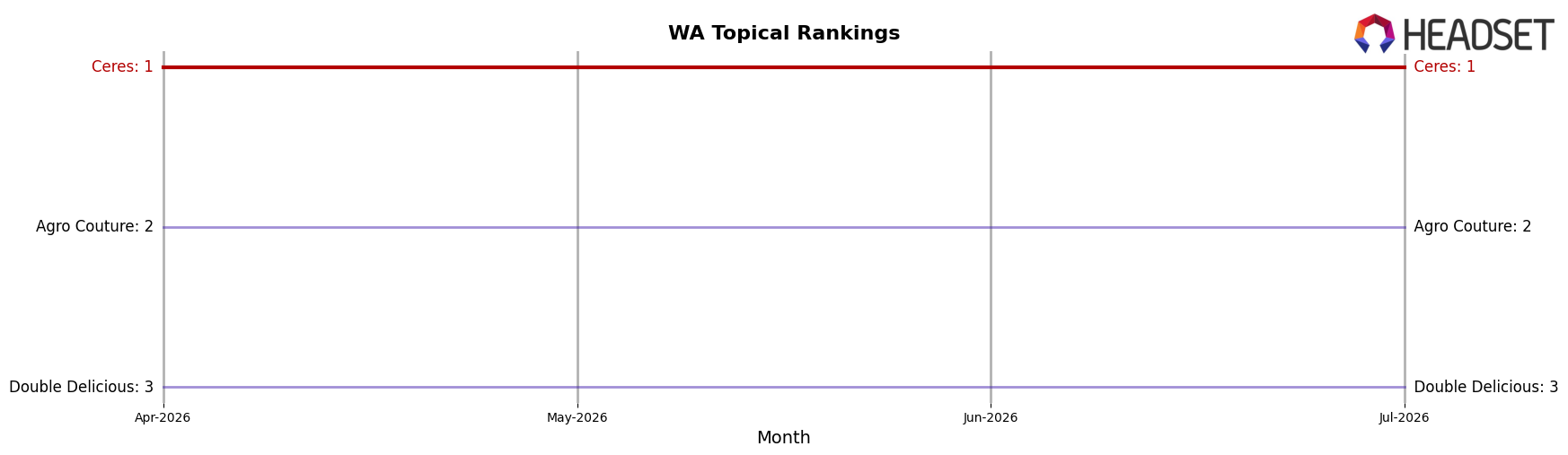

Ceres sits at rank #1 in WA Topical in July 2026, unchanged from #1 a year earlier, and has also held #1 for the past three months, while Agro Couture moved into #2 from #3 year over year on 10.2% sales growth and Double Delicious slipped to #3 from #2 with a 31.4% YoY sales decline; alongside this, Fairwinds stayed at #4 with a 27.5% YoY drop and SnacMe climbed to #5 from #6 with 57.5% YoY growth. The pattern implies Ceres’ flat YoY rank at the category peak consolidates leadership against upward pressure from faster-growing challengers like SnacMe and against contracting rivals such as Double Delicious, suggesting competitive stability at the top while share churn intensifies below.

Notable Products

CBD/THC/CBG/CBN 1:1 Xtra Strength Dragon Balm Roll on (1000mg CBD, 1150mg THC, 75mg CBG, 75mg CBN, 3.4oz, 100ml) set the tone with a -8.0% MoM dip while holding rank 1, as the CBG/CBN/CBD/THC 1:1 Gold Maximum Strength Dragon Pain Relieving Roll on (1300mg CBG, 100mg CBN, 100mg CBD, 1500mg THC, 3.4oz) rose +15.1% at rank 2, implying the highest-ranked demand is rotating within Topicals rather than exiting the segment. With four Edible SKUs concentrated in ranks 3–6 and 8–10, category breadth is widening even as the CBD/THC/CBG 1:1:1 Sativa Assorted Tropical Fruit Chews 10-Pack (100mg CBD, 100mg THC, 100mg CBG) advanced +24.6% to rank 6 and Sativa Sea Salted Caramel Chocolate Balls 10-Pack (100mg) gained +17.1% at rank 3, pointing to mixed-cannabinoid formats doing the incremental lifting. The CBD/THC/CBG/CBN 1:1 Xtra Strength Dragon Pain Relieving Squeeze Lotion (1000mg CBD, 1150mg THC, 75mg CBG, 75mg CBN, 3.4oz) added +6.2% at rank 7 while the CBD/THC 1:1 Indica Assorted Fruit Chews 10-Pack (100mg CBD, 100mg THC) in rank 4 rose +3.5%, suggesting price point and multi-cannabinoid positioning, rather than single-strain novelty, is capturing July 2026 basket share. Overall, the mix implies Ceres is concentrating on multi-cannabinoid, function-forward formats to defend Topicals leadership while letting faster-growing Edibles expand reach, with July 2026 revenue anchored by two Topicals over $100,000 and incremental growth coming from diversified Edible ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.