Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Double Delicious is stocked at 161 licensed dispensaries across Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Olympia, and Vancouver. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

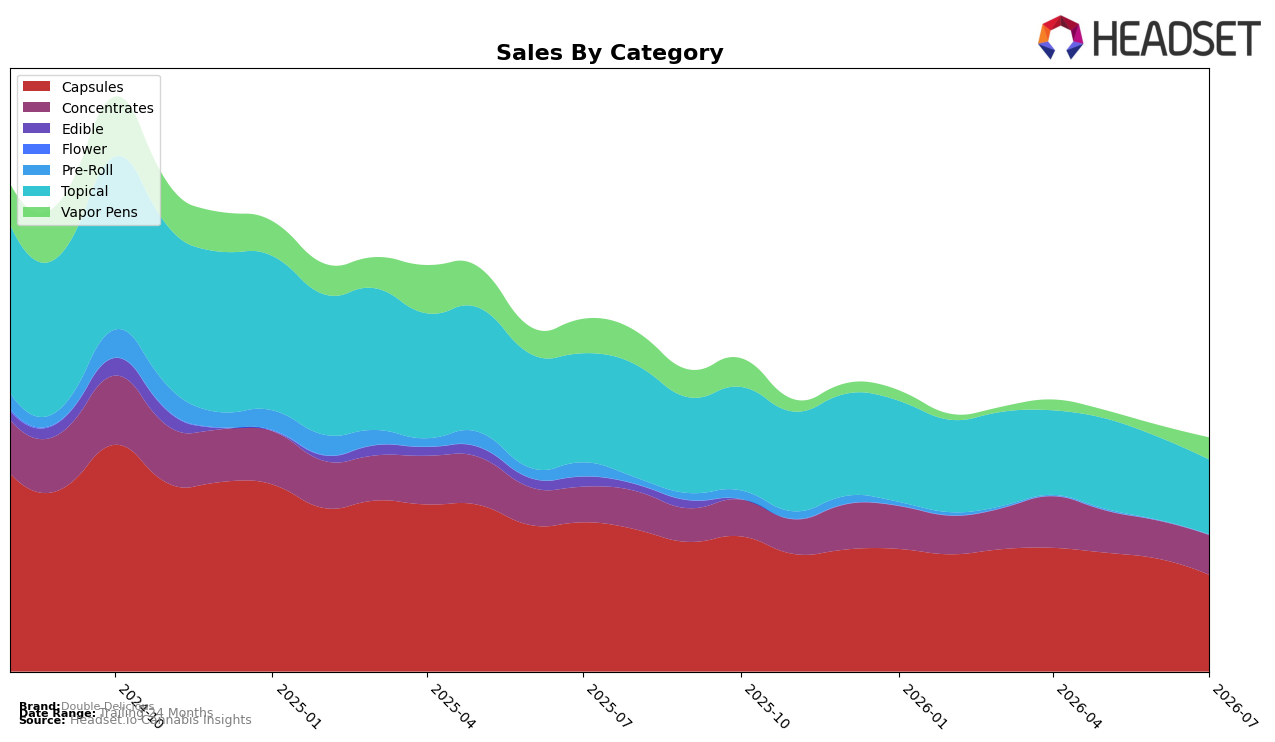

In July 2026, Double Delicious concentrated 41.50% of sales in Capsules and 32.08% in Topical, while Concentrates and Vapor Pens accounted for 17.00% and 9.40% respectively, indicating a two-tier mix anchored by Capsules yet diversifying at the margin. Year over year, Capsules fell 35.21% and Topical declined 31.40%, but Concentrates rose 11.69% and Vapor Pens spiked 87.45% month over month; meanwhile, Capsules slipped 14.34% MoM and Topical eased 9.89% MoM. With a state-category rank of 1 in Capsules within Washington and a brand-level sales decline of 33.74% YoY, the pattern implies reliance on a leading Capsule position even as growth pockets shift toward Concentrates and near-term recovery in Vapor Pens.

The mix shift suggests repositioning headroom: Concentrates’ 11.69% YoY gain and 4.44% MoM lift against double-digit MoM declines in Capsules (-14.34%) and Topical (-9.89%) signals that expanding assortment and visibility in value-oriented extract formats could offset the 33.74% YoY brand contraction and the 1.69% YoY decrease in average price. Vapor Pens’ 87.45% MoM rebound alongside a 36.06% YoY drop indicates activation-driven volatility that can be harnessed tactically, while Pre-Roll’s 99.76% YoY and 82.08% MoM declines at a 0.01% share argue for deprioritization; taken together, the data imply a pivot from Capsule-dependence toward a balanced posture where Concentrates absorb share loss and Vapor Pens serve as episodic traffic drivers.

Competitive Landscape

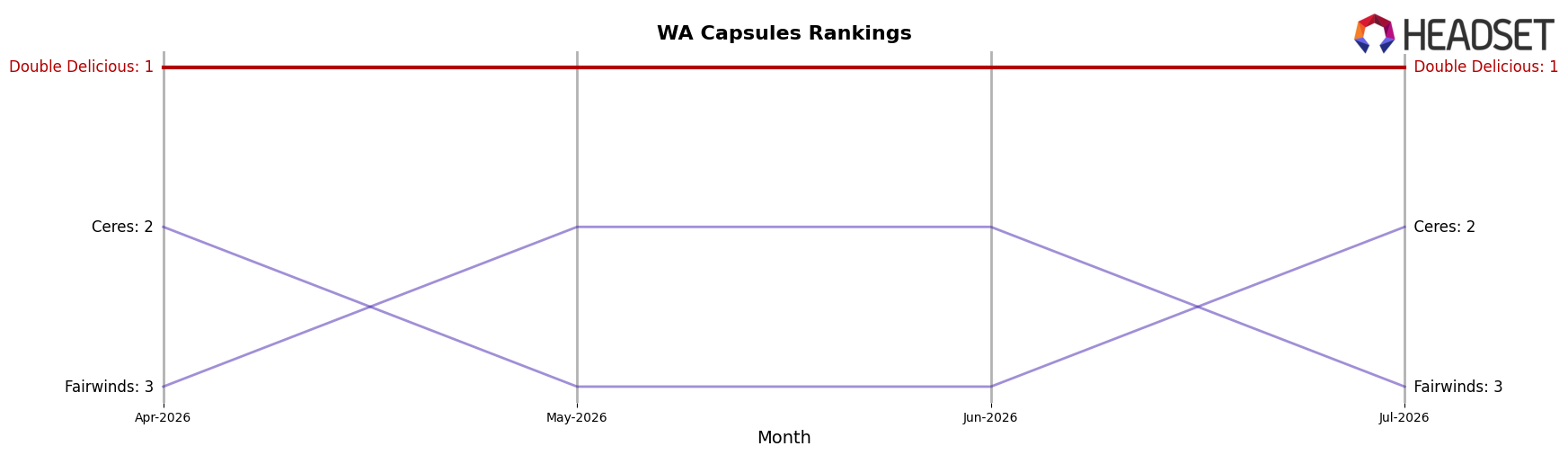

Double Delicious holds rank #1 in WA Capsules in July 2026, unchanged YoY from rank #1, while also holding #1 over the latest three months; in contrast, Ceres sits at #2 after moving up from #3 YoY with sales up 8.4%, and Fairwinds slid to #3 from #2 alongside a 33.2% YoY sales decline. Meanwhile, Constellation Cannabis remained at #4 YoY while growing sales 103.5%, and Essence Entourage Extracts climbed to #5 from #8 with 51.1% YoY growth; despite these upward moves, Double Delicious peaked at #1 in July 2026 and has not ceded share rank across the last three months, implying that even as challengers gain velocity the category’s leadership remains anchored unless a top-five brand converts growth into an actual rank shift.

Notable Products

Sativa RSO Capsules 10-Pack (100mg) posted the steepest decline in July 2026 at -19.7% MoM while holding rank 2, and Hybrid Capsules 10-Pack (100mg) fell -18.0% MoM at rank 3, indicating concentrated pressure on the capsule lineup near the top of the chart. Indica RSO Capsules 10-Pack (100mg) slipped -7.9% MoM yet remained rank 1, whereas Indica Super RSO Infusionz 3-Pack (600mg) dropped -22.2% MoM at rank 9, contrasting with CBD/THC 40:1 Capsules 10-Pack (1000mg CBD, 25mg THC) which grew 12.2% MoM at rank 7 and suggests a pivot within capsules toward functional CBD-heavy formats. Four of the top ten are Capsules, and three are Topical SKUs, with only one Topical posting a gain at +5.4% MoM for Sativa RSO Infusions 3-Pack (300mg); this split implies that Double Delicious is leaning on Capsules for rank stability while Topicals soften outside of isolated lifts. The pattern points to a near-term commercial direction favoring diversified capsule formulations and value-tier retention at the top, while discretionary Topicals may require pricing or pack-size adjustments to restore momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.