Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Choice is stocked at 545 licensed dispensaries across Michigan, Massachusetts, and 2 other states, 437 of them in Michigan, with the deepest coverage in New Buffalo, Detroit, Grand Rapids, Kalamazoo, and Monroe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

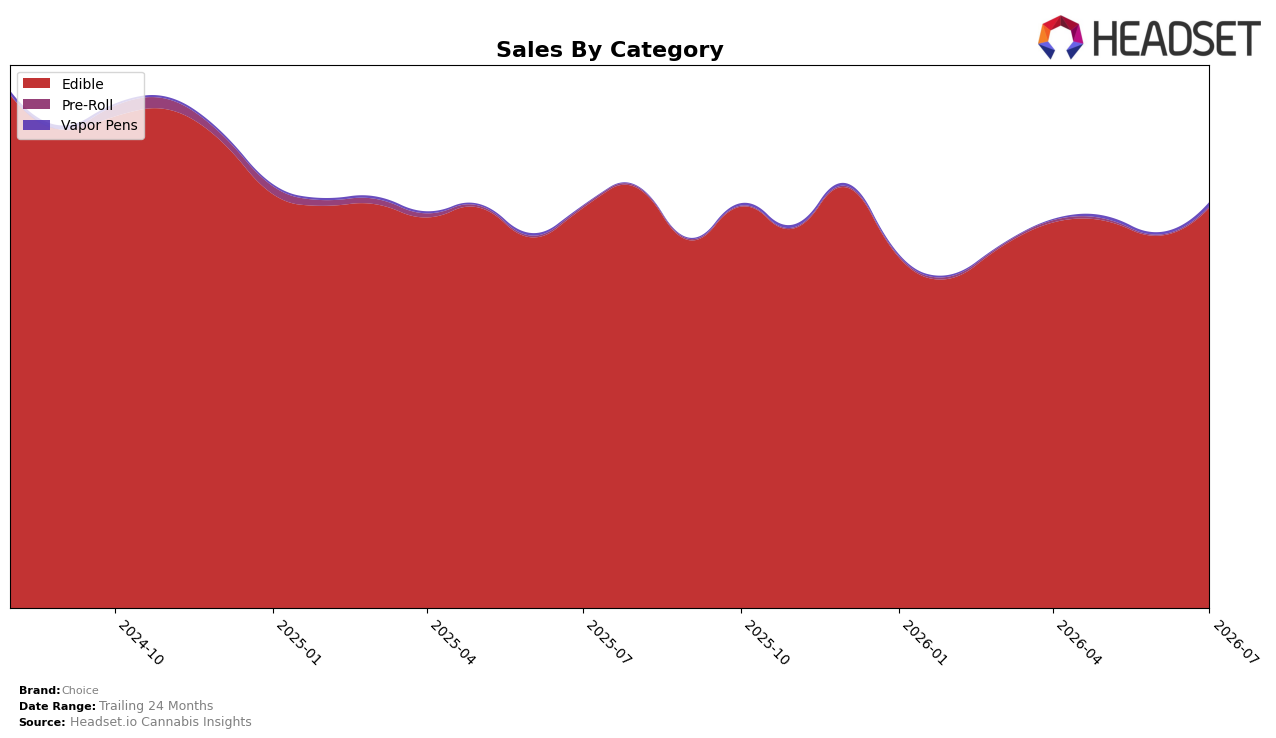

Choice’s mix in July 2026 is overwhelmingly concentrated in Edible at 98.68% share, with Edible up 1.59% year over year and 7.50% month over month, while Vapor Pens, though only 0.96% share, surged 457.70% YoY and 86.63% MoM, and Pre-Roll at 0.36% share fell 0.65% YoY but jumped 86.54% MoM. Average price across the brand rose 73.36% YoY to $3.88 as Edible pricing sat at $3.87, suggesting mix and price are pulling in the same direction. With Choice ranked 2 in Edible in Michigan, the pattern implies a category-led scale that still leaves headroom in small but fast-accelerating formats to diversify revenue without diluting the core.

The tilt toward Edible at 98.68% share, paired with brand-level sales growth of 80.79% YoY and only 1.59% YoY growth within Edible, implies that volume gains likely came from distribution or velocity expansion rather than category switching, while the 86.63% MoM jump in Vapor Pens signals a testable secondary pillar forming. The 19.56% decline over 24 months alongside a 73.36% YoY price increase indicates pricing power or pack-size shift that can sustain rank 2 in Edible but may cap household penetration if not balanced by sub-$4 laddering. Net, July 2026 points to maintaining Edible leadership in Michigan while leaning into Vapor Pens’ triple-digit growth to hedge against Edible-specific volatility.

Competitive Landscape

Choice is ranked #2 in MI Edible in July 2026, unchanged from #2 year over year, and steady at #2 over the last three months, while its peak at #1 came in November 2024; in contrast, Wyld held #1 but posted a -23.3% YoY sales change and Camino improved directionally from #4 YoY to #3 with +12.9% YoY sales, indicating that Choice’s static rank alongside a sliding category leader and a rising challenger implies a stable but pressured hold on the #2 position with limited upside without share capture from #1 or defense against #3.

Notable Products

Orange Creamsicle Gummies 10-Pack (200mg) posted the steepest move in July 2026, dropping 17.7% MoM to rank 4, while Chronic Cherry Berry Soft Chews 10-Pack (200mg) fell 20.1% MoM to rank 6, signaling flavor-specific fatigue even within top-10 placements. Offsetting that, Sativa Red Raz Haze Gummies 10-Pack (200mg) grew 10.1% MoM to hold rank 1 and Watermelon Kush Gummies 10-Pack (200mg) rose 11.8% MoM at rank 5, with Sunburst Peach Chews 10-Pack (200mg) adding 11.0% MoM at rank 7, indicating momentum clustered in fruit-forward SKUs that promise uplift or summer-aligned profiles. With all top-10 entries in Edible and eight of the ten carrying gummy or soft chew formats, the mix implies Choice is consolidating around chewable edibles where incremental flavor bets drive swings rather than format shifts.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.