Market Insights Snapshot

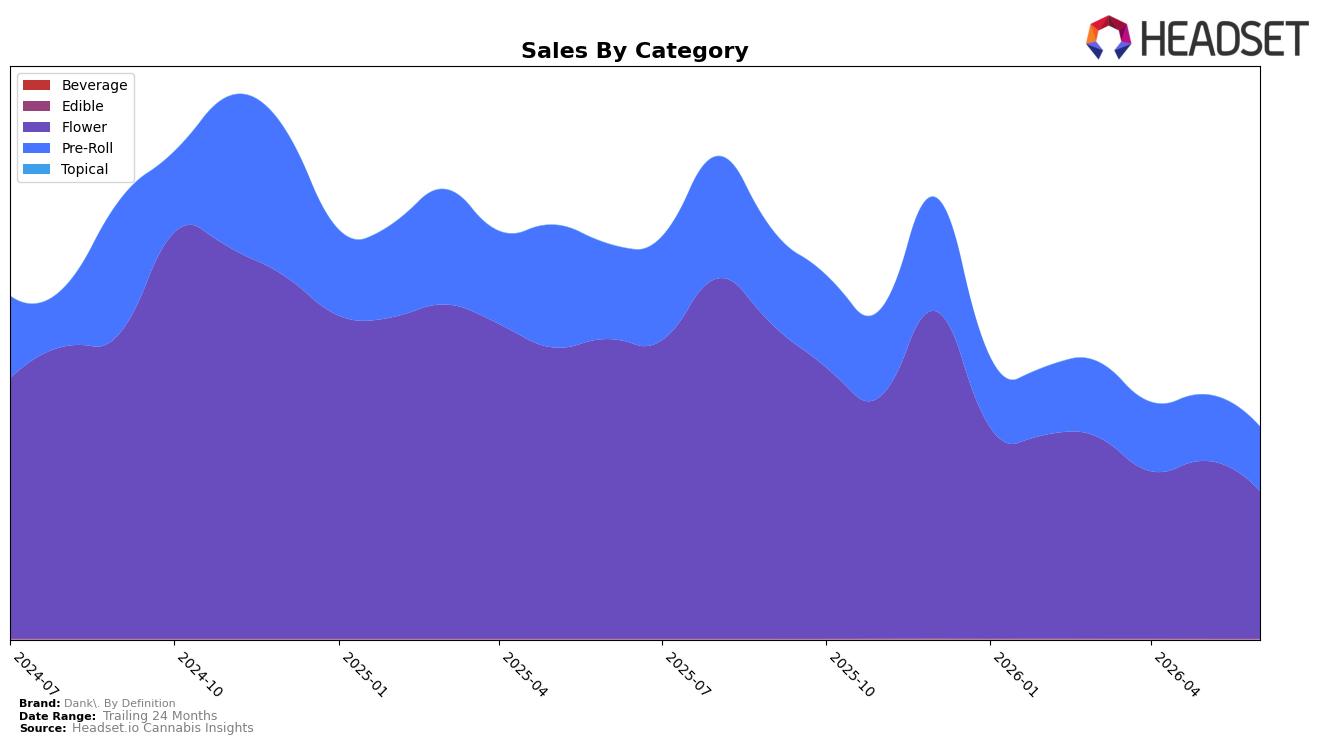

June 2026 category mix concentrated 69.71% in Flower and 30.29% in Pre-Roll, with Flower down 50.73% year over year and 16.92% month over month, while Pre-Roll declined 32.52% year over year and 3.01% month over month. Despite the overall brand sales decline of 46.35% year over year and a 3.70% year-over-year drop in average price to $39.55, Dank. By Definition held a Flower rank of 3 in New York, indicating category concentration outweighed price as the near‑term risk factor. The pattern suggests the heavier exposure to Flower amplified volatility versus the less negative Pre-Roll trajectory, implying the mix itself, rather than pricing alone, is the main driver of the downturn.

With Pre-Roll only 30.29% of sales yet posting a shallower month-over-month decline of 3.01% compared with Flower’s 16.92%, the mix skews toward the more volatile piece even as a less volatile segment underperforms less severely. The 50.73% Flower year-over-year decline versus 32.52% in Pre-Roll, combined with holding rank 3 in New York Flower, implies positioning is anchored to Flower share leadership but at the cost of exposure to sharper category contractions; rebalancing toward Pre-Roll could stabilize month-to-month performance while maintaining visibility in Flower.

Competitive Landscape

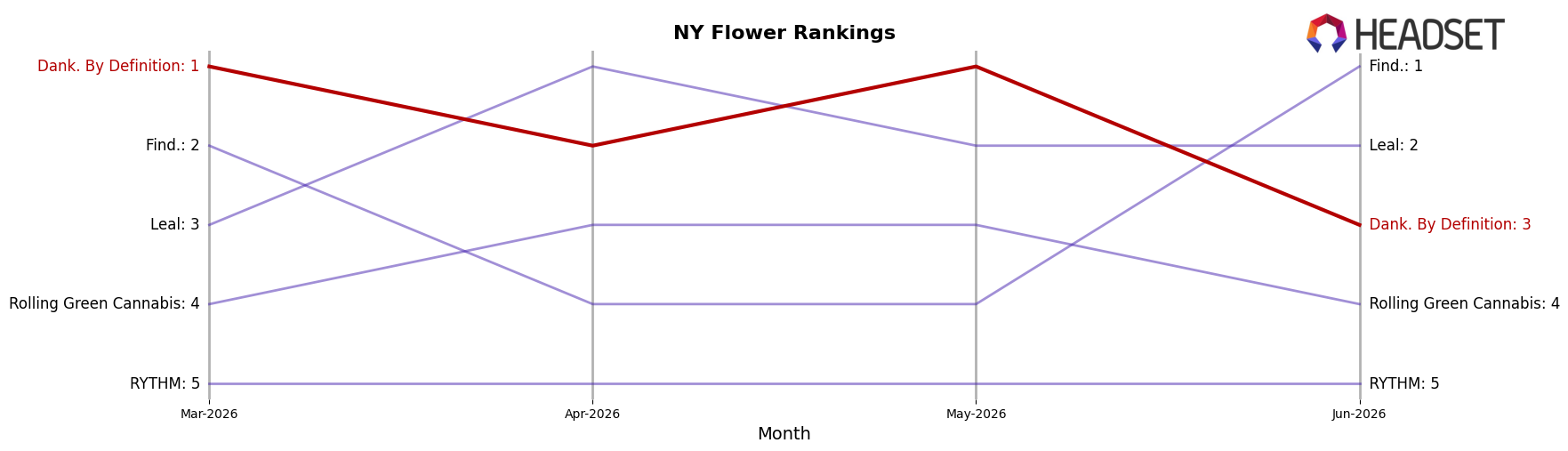

Dank. By Definition is ranked #3 in NY Flower in June 2026, sliding 2 positions from its #1 peak in May 2026 while still improving 1 rank year over year, and its 3-month position moved from #1 to #3, indicating a near-term pullback against a longer-term climb; meanwhile, Find. leads at #1 after rising 2 spots from a year-ago #3 with sales up 35.6%, and Leal advanced to #2 from #7 year over year with a 44.4% sales increase, while Rolling Green Cannabis sits at #4 after a 2-rank improvement despite a 7.1% sales decline; this pattern implies Dank. By Definition’s rank trajectory is stabilizing below the top two as faster YoY climbers compress share at the top despite its prior #1 peak.

Notable Products

Randy Marsh (3.5g) posted the steepest pullback in June 2026 at -20.8% and slid to rank 6, while Golden Ticket Pre-Roll (0.5g) fell -42.5% to rank 8, indicating price-sensitive or format-specific fatigue against a backdrop where Green Crack Pre-Roll 7-Pack (3.5g) still rose +23.0% at rank 1. Four of the top ten are Pre-Roll SKUs and they span ranks 1, 2, 3, 7, 8, 9, and 10, yet the category is bifurcated with Alien Cookies Pre-Roll (1g) inching up +4.0% at rank 7 as Green Crack Pre-Roll (1g) gained +13.9% at rank 10, contrasting with the underperformance of the half-gram value format; this split implies consumers are concentrating spend in premium multi-packs and familiar 1g singles over sub-gram entries. Hawaiian Haze (3.5g) advanced +10.2% at rank 5 while Chemdawg (3.5g) held rank 4 on a larger base near $44,000, framing Flower as stable-to-mixed while Pre-Roll volatility sets the pace; the product mix points to prioritizing higher-yield Pre-Roll pack sizes and a tighter Flower lineup to defend top ranks and reduce downside from lagging SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.