Where to Buy

Leal is stocked at 160 licensed dispensaries across New York and Michigan, 158 of them in New York, with the deepest coverage in New York, Queens, Buffalo, Albany, and Farmingdale. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

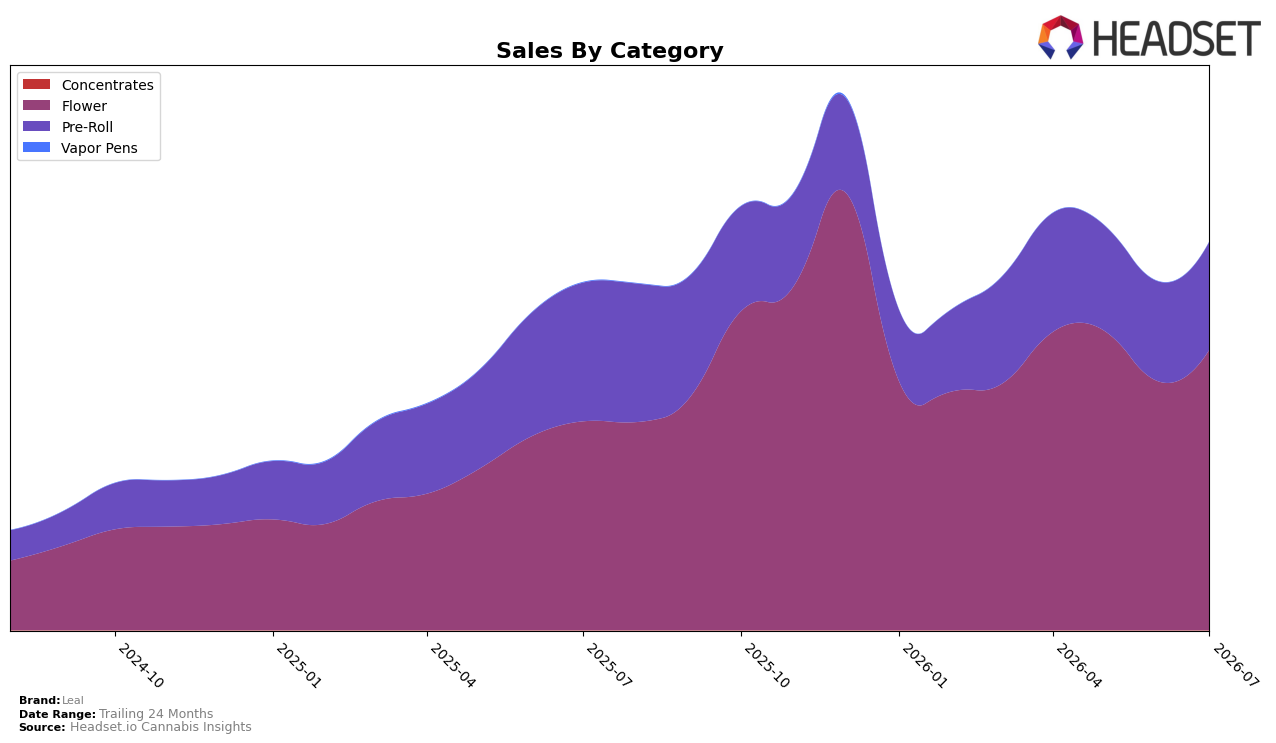

Market Insights Snapshot

In July 2026, Leal’s category mix concentrated 72.22% share in Flower and 27.78% in Pre-Roll, with Flower up 34.39% year over year and 12.72% month over month while Pre-Roll declined 22.08% year over year but rose 8.27% month over month; the average price rose 21.56% year over year alongside a brand-level sales increase of 11.76% year over year. Within Flower specifically, the average price reached $44.06 as share tilted further toward the category, and Leal held rank 2 in Flower in New York, indicating mix-driven growth concentrated in higher-priced Flower while Pre-Roll serves as a smaller, partially recovering secondary lane.

The shift toward Flower’s 72.22% share combined with July 2026 month-over-month gains in both categories (12.72% in Flower vs. 8.27% in Pre-Roll) implies Leal is reinforcing a premium-leaning positioning anchored in Flower, using price to support revenue density amid softer Pre-Roll demand. With rank 2 in New York Flower and a 34.39% year-over-year Flower lift versus a 22.08% Pre-Roll decline, the brand’s near-term path is to defend Flower share while selectively stabilizing Pre-Roll to prevent margin drag, implying pricing power in core Flower and targeted promotion or assortment pruning in Pre-Roll to balance mix without diluting the Flower-led trajectory.

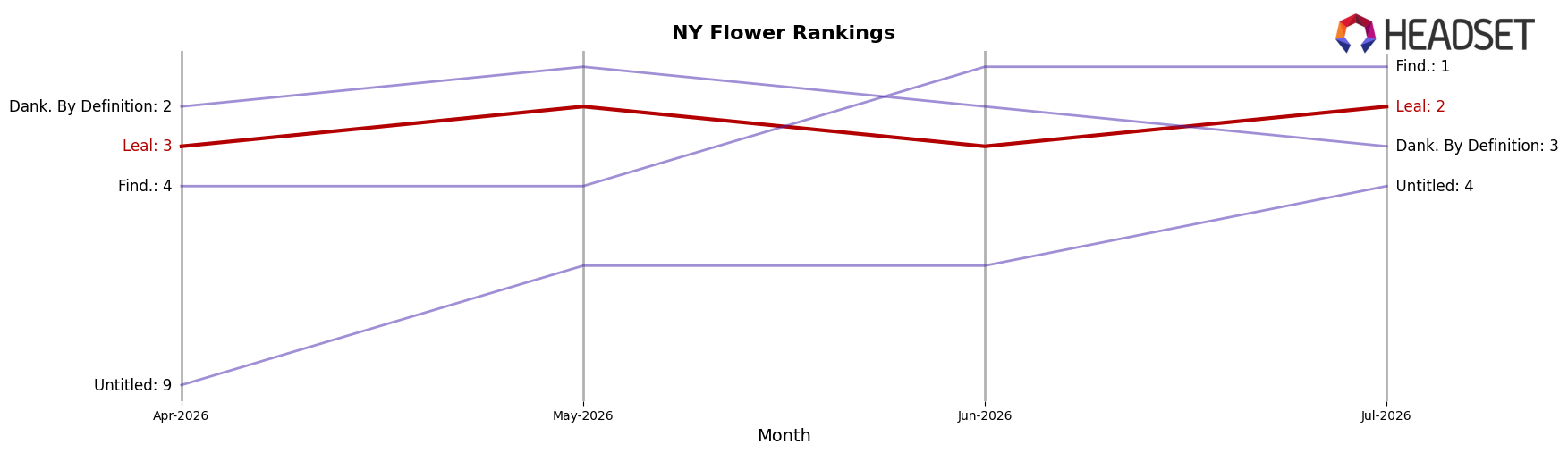

Competitive Landscape

Leal is ranked #2 in New York Flower in July 2026, climbing 5 positions year over year from #7, and edging up 1 spot since April 2026 when it sat at #3; this coincides with reaching a peak rank of #2 in July 2026 while remaining 1 place behind Find., which advanced from #8 to #1 with a 46.7% year-over-year sales increase. The immediate pressure below comes from Dank. By Definition, which slid from #1 to #3 amid a 51.5% year-over-year sales decline, while Grassroots jumped from #15 to #5 alongside a 79.8% year-over-year sales increase; these shifts indicate Leal’s ascent is enabled as much by competitor divergence as by its own upward mobility, implying that sustaining #2 or contending for #1 will depend on outpacing Find. while insulating against fast-risers like Grassroots.

Notable Products

Lemon Venom Pre-Roll (1g) posted the standout move in July 2026 with a 65.4% MoM surge to $31,730 while jumping into rank 8, outpacing Garlic Budder Pre-Roll (1g) at rank 7 with a 51.3% MoM rise and Platinum Lemon Cherry Gelato Pre-Roll (1g) at rank 3 with a 45.2% MoM gain. Hella Jelly Pre-Roll (1g) held rank 1 with a 33.3% MoM increase, whereas Caramel Cream Pre-Roll (1g) slipped 0.9% MoM at rank 5, and Animal Face Pre-Roll (1g) advanced to rank 4 with a 45.0% MoM lift. Eight of the top ten are Pre-Roll SKUs, with only one Flower SKU in rank 9, implying Leal’s product mix is consolidating around Pre-Rolls as the volume engine even as a single Flower entry tests the ceiling on unit economics.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.