Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Delectable Dabs is stocked at 124 licensed dispensaries across Washington, with the deepest coverage in Spokane, Olympia, Seattle, Tacoma, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

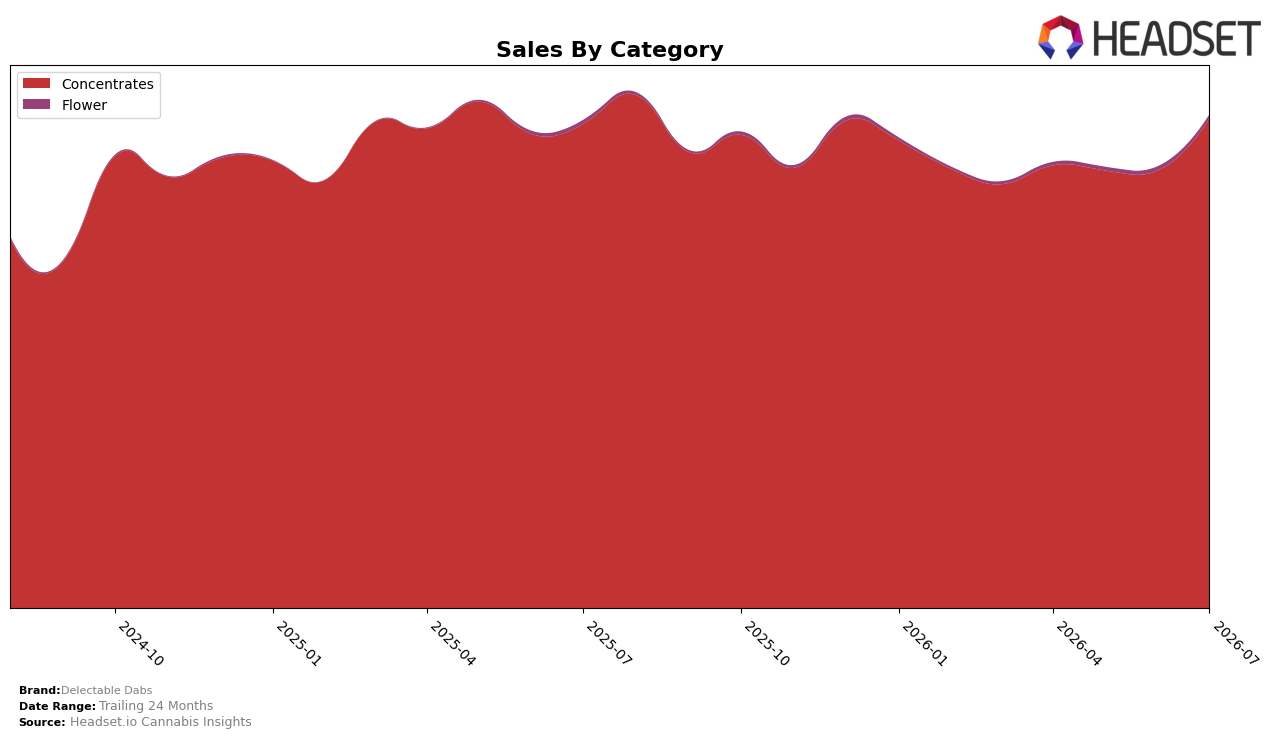

In July 2026, Delectable Dabs concentrated 99.15% of sales in Concentrates while Flower held 0.85%, with Concentrates up 1.12% year over year and 11.83% month over month, versus Flower up 2.66% YoY but down 2.81% MoM. The brand’s overall sales rose 113.28% YoY alongside an 11.35% YoY decline in average price, and within category details Concentrates averaged $5.42 while Flower averaged $8.03, indicating mix-led volume leverage; the implication is that volume gains are concentrated in a single category where MoM momentum outpaces the minor YoY increase, pointing to a strategy leaning on short-cycle promotions or velocity lifts in Concentrates.

Positioning-wise, ranking 2 in Concentrates in Washington while keeping 99.15% category share of brand sales and posting an 11.83% MoM uptick suggests defensible shelf presence in the core set, whereas the 2.81% MoM decline and 0.85% mix in Flower limit diversification. With a 30.60% two-year sales increase and an 11.35% price compression YoY, the path forward implies reinforcing price-pack architecture in Concentrates to sustain rank 2 while testing selective expansion in Flower where a 2.66% YoY lift indicates latent demand without diluting the core identity.

Competitive Landscape

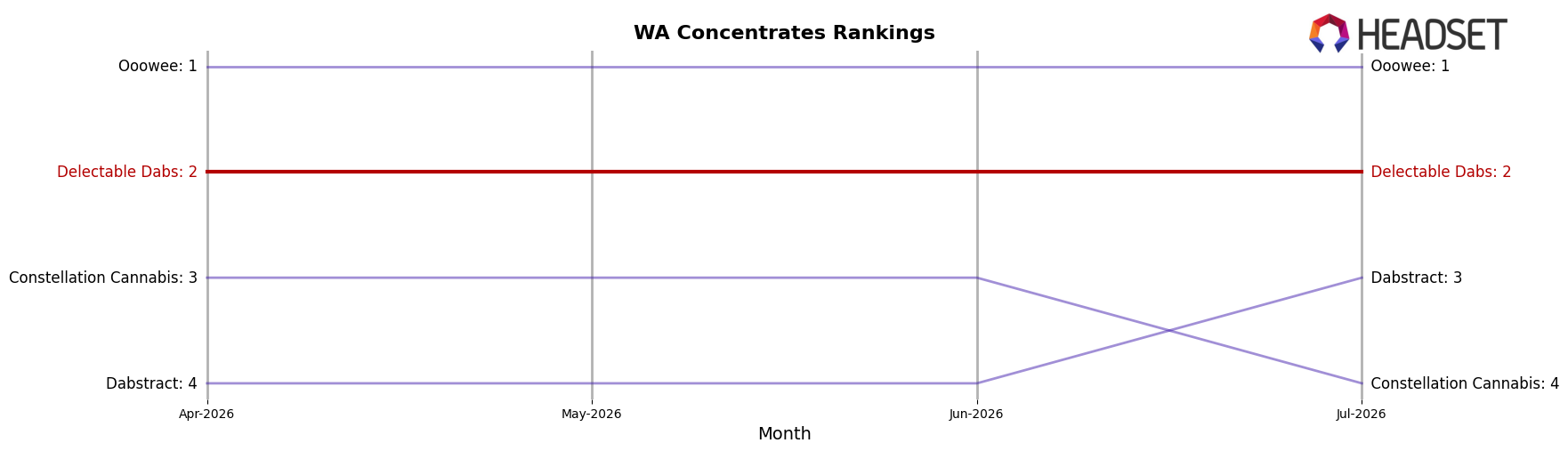

Delectable Dabs sits at rank #2 in WA Concentrates in July 2026 with no year-over-year rank change from #2, and no three-month change from #2, while category leader Ooowee holds #1 with a year-over-year decline of 6.9% in sales and Dabstract moved up from #4 to #3 on 5.2% year-over-year sales growth; in parallel, Constellation Cannabis climbed from #7 to #4 with an 18.9% increase, outpacing Oleum Extracts (Oleum Labs) which stayed flat at #5 with a 8.0% decline. The combination of a stable #2 position for Delectable Dabs across July 2026 and the widening pressure from faster-rising #3 and #4 competitors implies that holding share will increasingly depend on countering upward mobility below while exploiting softness at #1.

Notable Products

Maui Wowie Wax (1g) posted the standout move in July 2026 with a 38.0% month-over-month gain that lifted it to rank 3, while Lemon Walker OG Wax (1g) slipped 6.1% and held at rank 5. Indica Wax 3-Pack (3g) remained the anchor at rank 1 with a 9.1% increase, and Northern Lights Wax (1g) advanced 24.1% to stay at rank 4. With three 3-Pack formats sitting inside the top 10 and Hybrid Wax 3-Pack (3g) up 6.2% at rank 10, the mix signals a shift toward multi-gram value packs paired with a few fast-moving single-gram strains, pointing to a strategy that balances basket-building with trial of standout flavors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.