Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

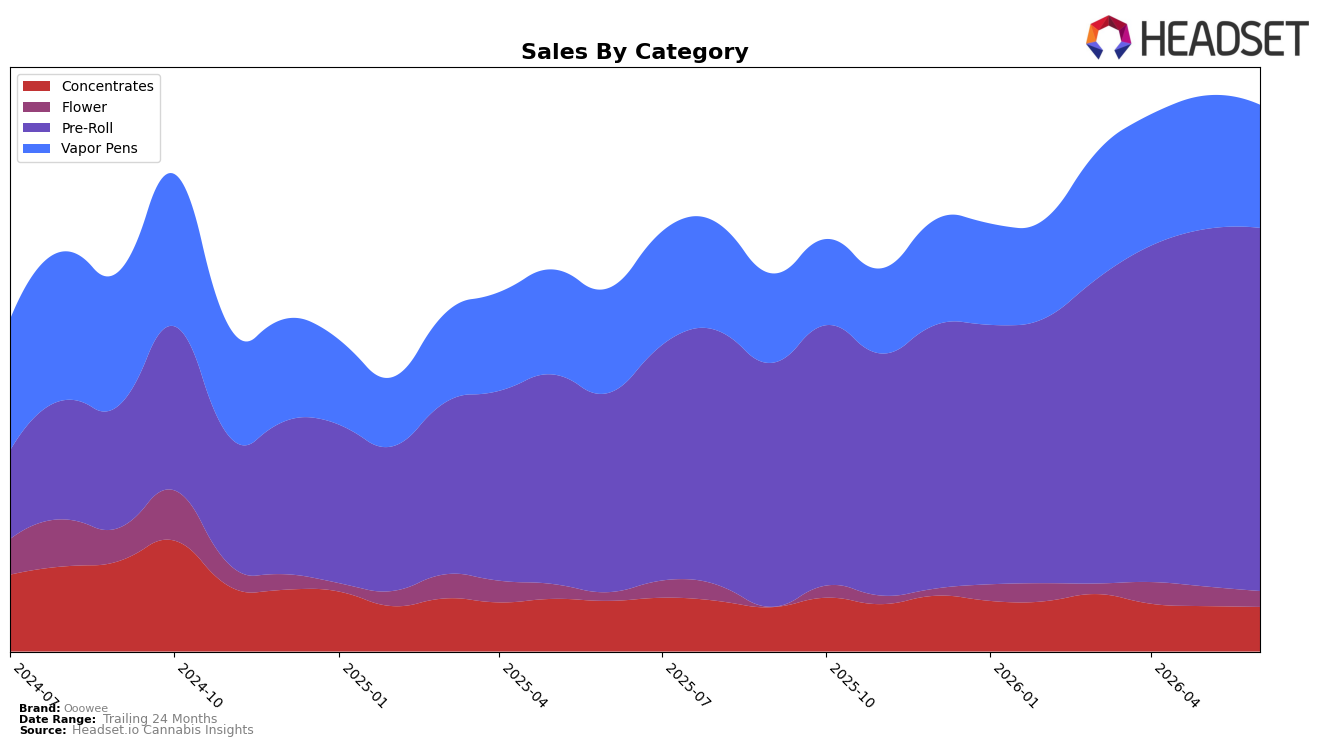

In June 2026, Ooowee’s category mix tilted further toward Pre-Roll at 57.27% share, with year-over-year sales up 68.92% and month-over-month up 1.50%, while Vapor Pens held 23.08% share but declined month-over-month by 6.02% despite a 12.83% year-over-year gain. Concentrates accounted for 11.87% share with a 6.77% year-over-year decline and a 0.95% month-over-month dip, and Flower at 7.78% share grew 15.20% year-over-year but fell 6.55% month-over-month. With an average price up 3.19% year-over-year to $10.03 and Pre-Roll pricing at $9.12, the mix suggests demand consolidation in value-accessible formats; the pattern implies Ooowee is leaning into Pre-Roll strength to offset Vapor Pens and Flower month-over-month pressure, supporting overall brand sales growth of 35.41% year-over-year.

Holding rank 1 in Pre-Roll in Washington while Pre-Roll share sits at 57.27% and climbs 68.92% year-over-year signals a scale moat in the lead category, whereas simultaneous month-over-month declines of 6.02% in Vapor Pens and 6.55% in Flower point to near-term volatility outside the core. The 11.87% share in Concentrates with a 6.77% year-over-year contraction, contrasted against a modest 1.50% month-over-month Pre-Roll lift, indicates that incremental gains are coming primarily from the flagship format rather than breadth. The implication is a positioning anchored in value-forward Pre-Rolls that can carry portfolio momentum even as premium-priced Flower at a $26.63 average and Vapor Pens at $13.61 experience month-over-month pullbacks, suggesting future share defense hinges on deepening Pre-Roll dominance while selectively stabilizing the secondary categories.

Competitive Landscape

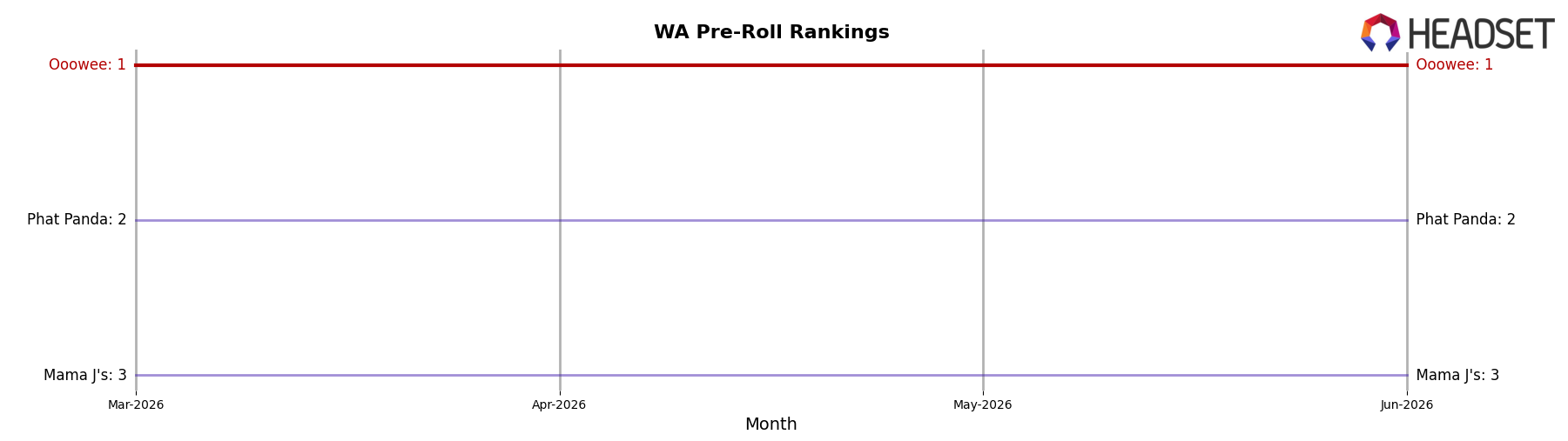

Ooowee ranks #1 in WA Pre-Roll in June 2026 after a YoY climb of 1 position from #2, and it has held #1 since April 2026 while remaining #1 over the last 3 months; meanwhile, Phat Panda sits at #2 after slipping 1 position YoY from #1 even with a 1.77% sales lift, and Lifted Cannabis Co advanced from #6 to #4 YoY with 16.80% sales growth. Mama J's held steady at #3 YoY despite 39.28% sales growth, while Stingers stayed at #5 with a 6.29% sales increase; Ooowee also hit its peak rank of #1 in June 2026, marking a 1-position improvement from its YoY standing. The pattern implies Ooowee’s top slot is driven more by relative rank stability and competitor churn than by outsized growth signals, meaning the brand’s short-term priority is defending #1 against mid-pack climbers converting growth into rank gains.

Notable Products

FaceLock Pre-Roll 5-Pack (5g) posted the sharpest movement in June 2026 with a -18.8% month-over-month slide and sat at rank 8, while Crunch Berries Pre-Roll 5-Pack (5g) gained 17.3% and held rank 1. White Peach Pre-Roll 5-Pack (5g) advanced 21.2% at rank 3, contrasting with Cheat Code Pre-Roll 5-Pack (5g) down 8.3% at rank 4. Eight of the top ten are Pre-Roll 5-Packs, and with one leading SKU at $87,702 alongside mixed mid-pack declines, the pattern implies Ooowee is consolidating around multi-pack pre-rolls but must refresh weaker variants to protect share at the lower top-10 ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.