Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Regulator is stocked at 140 licensed dispensaries across Washington, with the deepest coverage in Seattle, Spokane, Bellevue, Everett, and Bellingham. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

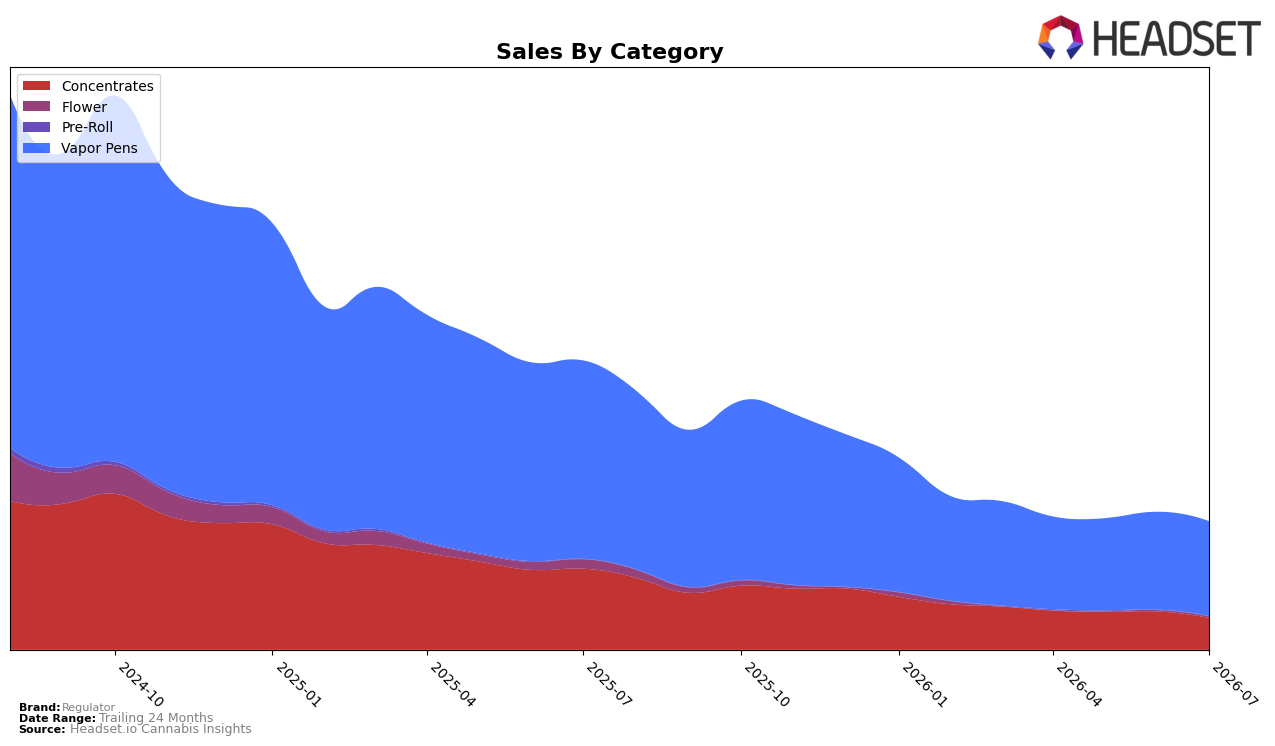

In July 2026, Regulator concentrated 74.24% of sales in Vapor Pens with a year-over-year decline of 52.31% and a month-over-month dip of 3.13%, while Concentrates held 24.73% share but fell 61.03% YoY and 17.13% MoM. Minor lines diverged: Flower represented 0.97% share with an 86.55% YoY drop but a 15.84% MoM uptick, and Pre-Roll at 0.06% share slipped 3.37% YoY and 26.46% MoM. With overall brand sales down 55.83% YoY and average price down 7.92% YoY to $11.00, the mix skews toward a shrinking core and contracting secondary category, implying the portfolio is over-indexed to categories under sharper contraction than the brand’s aggregate.

Given Vapor Pens’ 74.24% share alongside a category rank of 27 in Vapor Pens in Washington, the combination of a 52.31% YoY decline in that core and a 61.03% YoY drop in Concentrates concentrates risk in the mid-price inhalable space rather than diversifying into steadier segments. The 15.84% MoM lift in Flower from a 0.97% share base and the 26.46% MoM pullback in Pre-Roll at 0.06% share indicate micro-tests are too small to offset core erosion, implying that July 2026 positioning relies on price-led defense within Vapor Pens while lacking scale in counter-cyclical categories.

Competitive Landscape

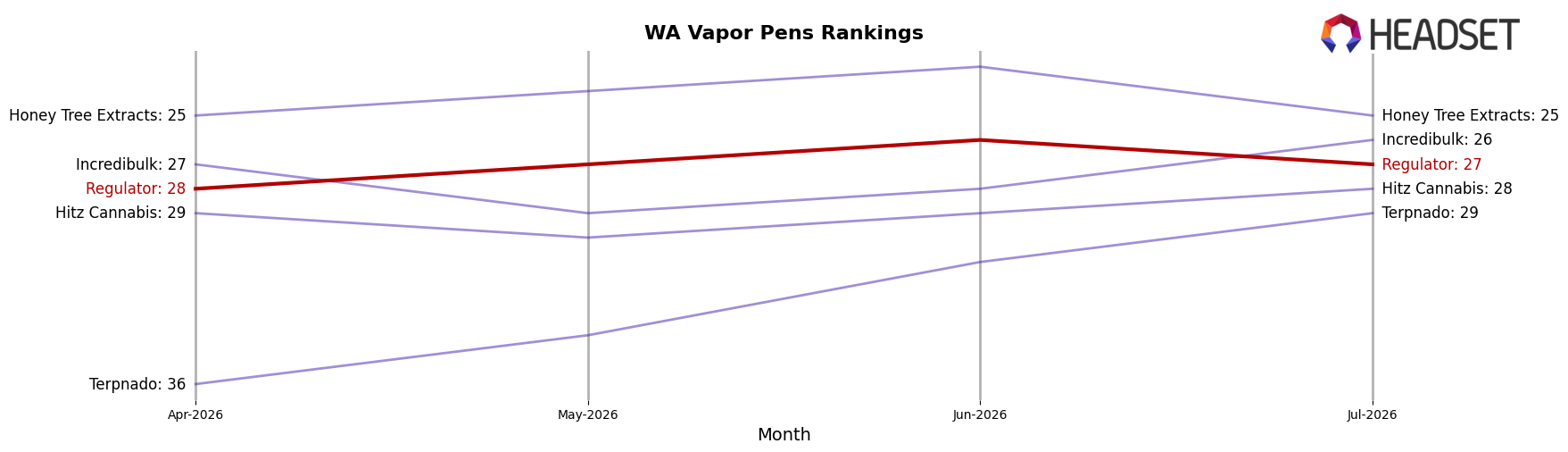

Regulator is currently ranked #27 in WA Vapor Pens, down 13 positions year over year from #14, and only one spot above its April 2026 three-month mark of #28; meanwhile, its historical peak was #9 in August 2024, placing today’s rank 18 places below that high. In contrast, Crystal Clear rose from #2 to #1 while posting a 12.6% year-over-year sales increase, and Mfused slipped from #1 to #2 alongside a 26.1% sales decline, indicating Regulator’s slide is not solely a market-wide contraction but a brand-specific loss of position. The pattern implies that without a reversal that closes a 13-rank YoY gap and narrows the 18-rank distance to its peak, Regulator is on a path toward lower visibility and reduced shelf priority within WA Vapor Pens.

Notable Products

Gelato Punch Sugar Wax (1g) posted the steepest movement in July 2026 with a -24.8% month-over-month decline and slid to rank 2, while Wedding Cake Sugar Wax (1g) rose 35.9% MoM to rank 1 and generated $9,291. Four of the top ten are Concentrates, and that cluster includes ranks 1, 2, 3, and 4, whereas Vapor Pens held ranks 6, 8, 9, and 10 with modest MoM shifts of -4.9% and -4.4% among the two ranked movers. Northern Lights Distillate Cartridge (1g) at rank 8 dipped 4.9% MoM and Pineapple Super Silver Haze Distillate Cartridge (1g) at rank 9 fell 4.4% MoM, signaling softer pen momentum as Concentrates volatility drives rank reshuffling. The pattern implies Regulator is leaning into sugar wax variants where upside and downside swings are sharper than in Vapor Pens, suggesting a short-term emphasis on high-velocity Concentrates while pens stabilize as a steadier baseline.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.