Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Drops is stocked at 1,100 licensed dispensaries across California, Oregon, and 5 other states, 439 of them in California, with the deepest coverage in Los Angeles, Sacramento, San Diego, San Francisco, and Santa Rosa. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

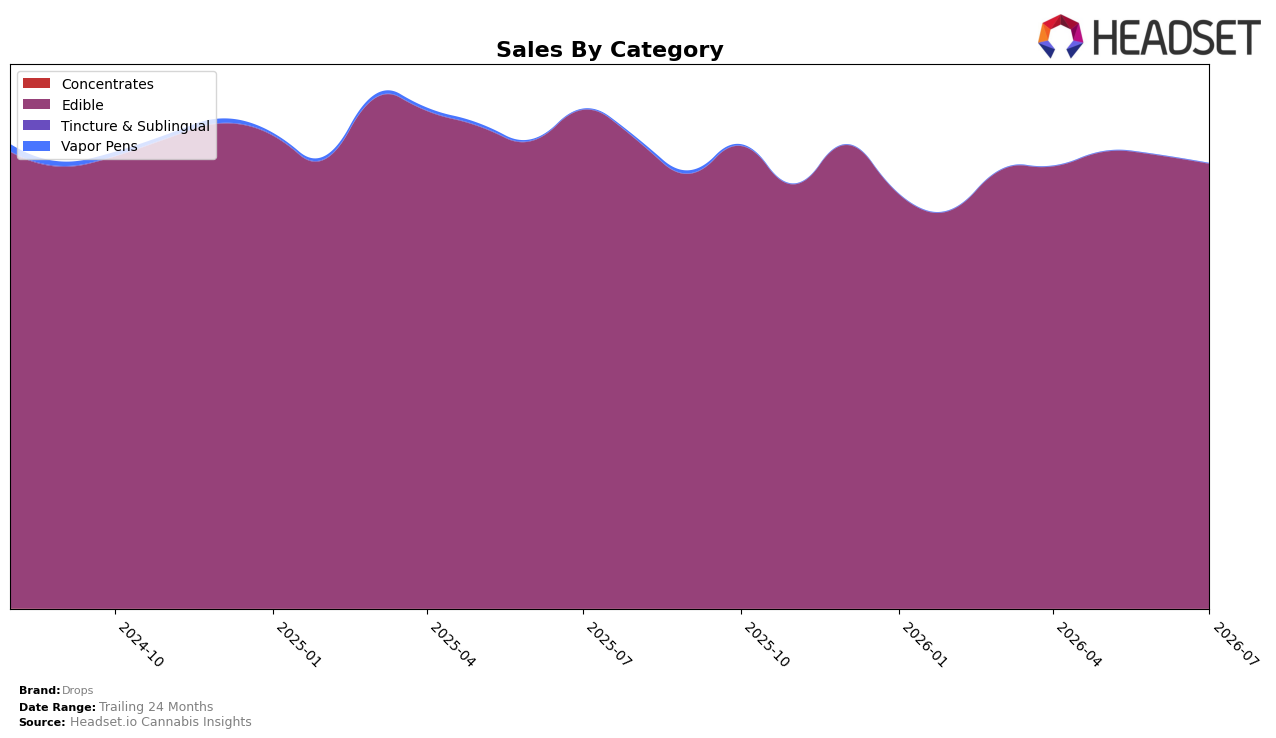

In July 2026, Drops remained fully concentrated in Edible with a 100.0% category share, while Edible sales declined year over year by 10.82% and slipped month over month by 1.88%. Brand-wide sales moved down 10.89% YoY alongside a 1.54% YoY increase in average price, indicating mix stability but softer unit velocity. With Edible holding all sales and the brand ranked 3 in Edible in Oregon, the pattern implies that single-category focus amplified exposure to category-level contraction and price resistance.

The combination of a full Edible mix at 100.0% and a 10.82% YoY category decline, paired with a 1.88% MoM dip in July 2026, suggests Drops is trading share on unit throughput rather than assortment breadth; the 1.54% YoY price lift likely pressured repeat volume. Holding the number 3 rank in Edible in Oregon amid a 10.89% brand sales decline YoY points to defensible placement but limited buffer against category swings; the implication is that near-term positioning depends on optimizing Edible pack-price architecture to recapture units without diluting rank.

Competitive Landscape

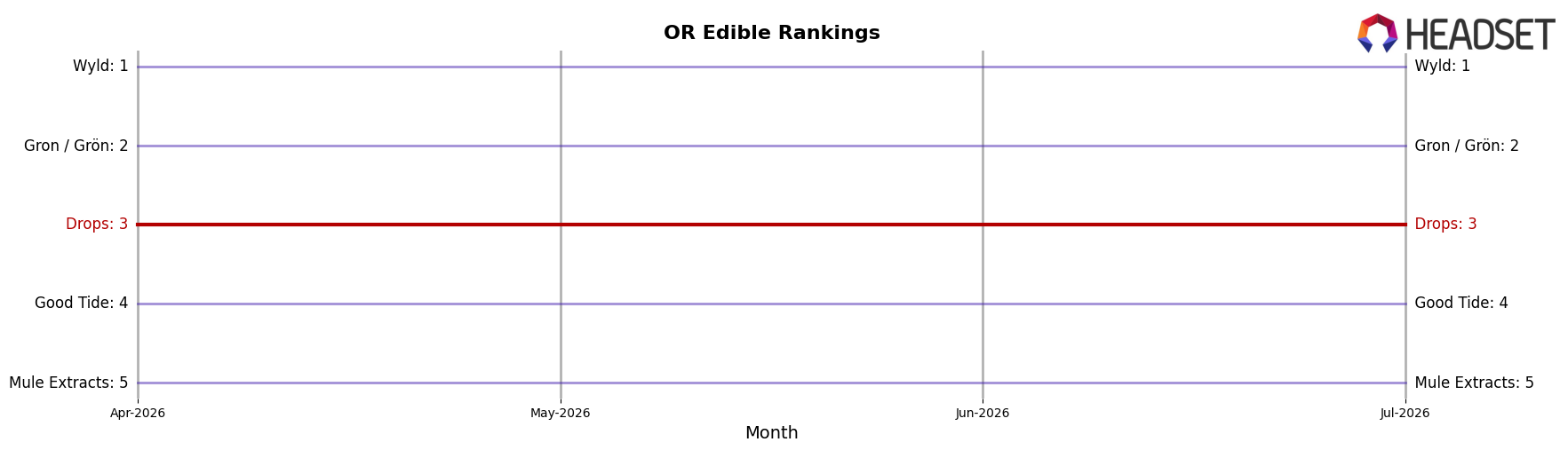

Drops is currently ranked #3 in OR Edible, unchanged from #3 year over year, and it has held #3 for the last three months, which contrasts with Wyld holding #1 with a 2.53% year-over-year sales increase and Gron / Grön fixed at #2 despite a -0.09% year-over-year sales change. Compared with Good Tide staying at #4 while declining -9.80% year over year and Mule Extracts remaining #5 with a 7.54% year-over-year gain, Drops’ flat rank at #3 and matching peak at #3 in July 2026 indicate that the brand is boxed in by a stable #1–#2 pair above and a mixed-growth pack below, implying that rank mobility will require either displacing a flat-to-slightly-negative #2 or outpacing a faster-growing #5 rather than defending against a weakening #4.

Notable Products

CBN/CBD/THC 1:1:1 Black Currant Rosin Gummies 20-Pack (100mg CBN, 100mg CBD, 100mg THC) held rank 1 despite a -1.45% month-over-month decline, while Active - Lemon Jelly (100mg) climbed 9.75% at rank 2 and Creative - Orange Live Rosin Gummies 20-Pack (100mg) advanced 5.61% at rank 5. With eight of the top ten in the Edible category and CBD/THC ratio SKUs spanning ranks 1, 3, and 4 growing between 2.18% and 6.81%, the mix concentrates around functional formulations rather than flavor-only plays, implying assortment depth is pulling repeat demand. Active - Lemon Live Rosin Jellies 2-Pack (100mg) slipped -6.94% at rank 6 as Chill - Watermelon Jelly (100mg) fell -5.16% at rank 10, contrasting with Lime Live Rosin Gummies 20-Pack (100mg) edging up 1.71% at rank 7; this divergence suggests smaller pack formats are ceding share to 20-Packs where one flagship alone cleared $189,892. The pattern implies July 2026 demand is consolidating around multi-cannabinoid 20-Packs with modest price elasticity, guiding Drops toward scaling ratio-led lines over 2-Packs to defend rank leadership.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.