Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

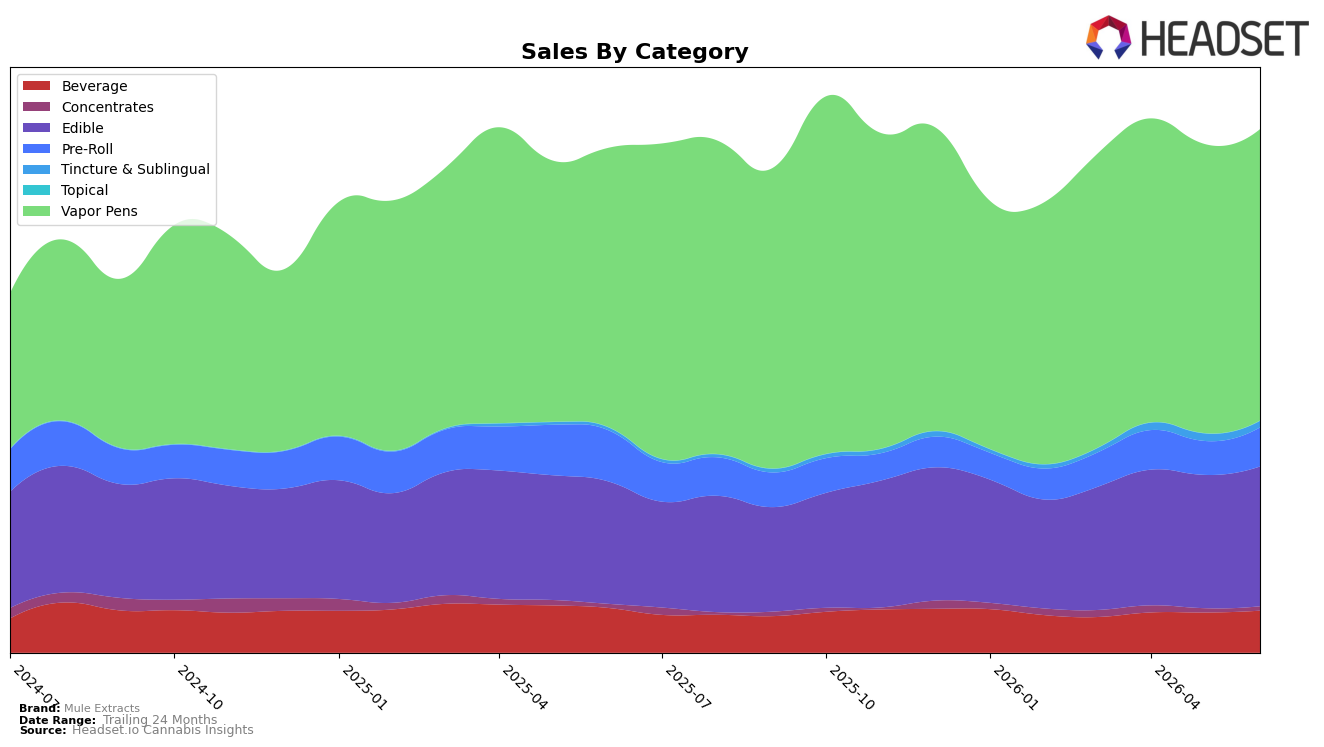

In June 2026, Mule Extracts concentrated 55.83% of sales in Vapor Pens with 0.79% MoM and 4.39% YoY growth, while Edible rose to a 26.75% share with 4.89% MoM and 14.22% YoY gains. Beverage held 8.02% share with a 4.58% MoM uptick despite a -6.12% YoY decline, and Pre-Roll at 7.42% share rebounded 15.24% MoM against a -23.88% YoY drop. Tincture & Sublingual, though only 1.19% share, surged 145.76% YoY but slipped -13.86% MoM, and Concentrates remained 0.78% share with 2.54% MoM and 7.96% YoY increases. The pattern implies Mule Extracts is leaning into a dual-engine mix where Vapor Pens anchors volume and Edible expands share, while cyclic MoM lifts in Pre-Roll and Beverage are not yet reversing their YoY contraction, keeping the brand’s growth rate (3.72% YoY overall) tied to stability in core inhalables.

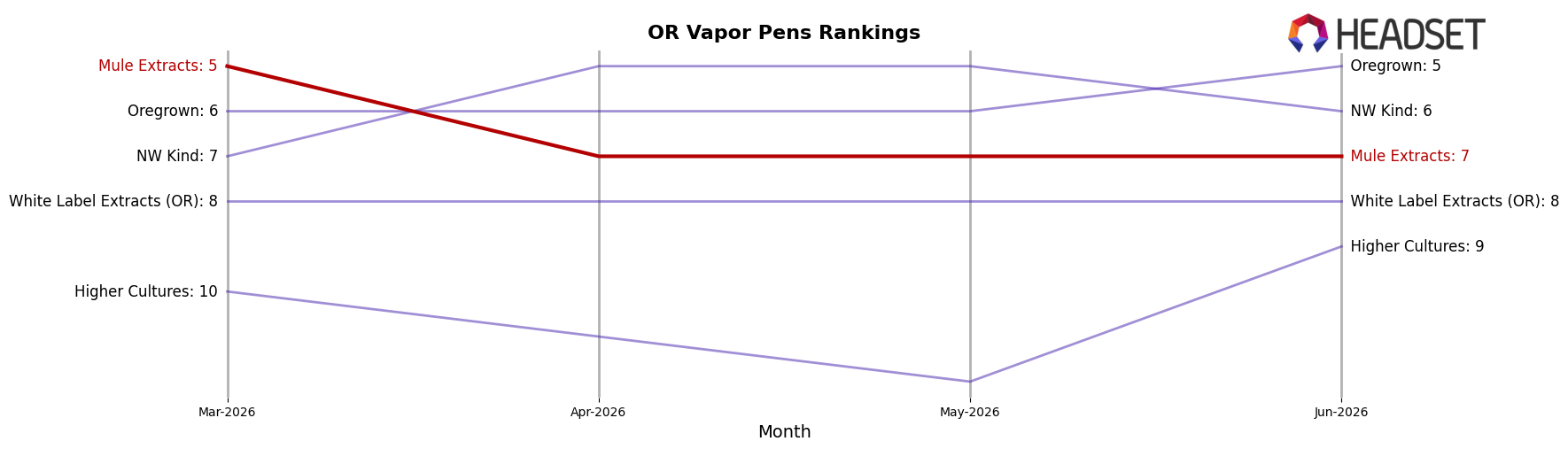

Average price rose 8.99% YoY to $11.91 alongside Vapor Pens’ 4.39% YoY and Edible’s 14.22% YoY growth, indicating pricing headroom in categories holding 82.59% combined share, while Pre-Roll’s -23.88% YoY with a 15.24% MoM bounce suggests promo-led volatility rather than structural recovery. Beverage’s -6.12% YoY amid a 4.58% MoM lift contrasts with Tincture & Sublingual’s 145.76% YoY on 1.19% share, implying niche trial without material mix impact. With Vapor Pens ranked 7 in Oregon, the category-weighted gains point to defensible placement in mainstream inhalables and an opportunistic push in Edible, while exposure to down-trending Pre-Roll and Beverage caps upside unless mix shifts further toward the two growth engines.

Competitive Landscape

Mule Extracts ranks #7 in OR Vapor Pens in June 2026, down 3 positions from #4 year over year, and 2 positions from #5 in March 2026; the brand’s peak of #3 in October 2025 contrasts with the current placement and signals a 4-rank slide from that high, while Buddies moved up from #2 to #1 and FRESHY climbed from #5 to #2 alongside an 81.5% YoY sales gain, indicating Mule Extracts is losing relative share of shelf movement as faster risers consolidate the top tier, which implies the trajectory points toward mid-pack stabilization unless velocity or distribution reclaim momentum.

Notable Products

Mule Kicker - CBD/THC 1:1 Dragon Fruit Gummies 2-Pack (100mg CBD, 100mg THC) posted the steepest decline in June 2026 at -20.9% and slid to rank 7, while Mini Kicker - Galactic Green Grape Full Spectrum Gummies 2-Pack (100mg) fell -20.3% to rank 8, signaling waning demand for balanced or full-spectrum formats even as top sellers held ground. Mule Kicker - Peachy Gummy (100mg) grew 26.1% to rank 1 and Mule Kicker - Twisted Citrus Live Resin Gummy (100mg) added 13.3% at rank 3, whereas Mini Kicker - Raspberry Pomegranate Gummies 10-Pack (100mg) dipped -3.1% yet remained rank 2, indicating momentum is consolidating in single-flavor 100mg Mule Kicker SKUs. Five of the top ten are multi-cannabinoid or ratio gummies, but two of those ratio-led entries dropped double digits while Nite Qaud Kicker - THC/CBD/CBN/CBG 2:1:4:1 Sour Blackberry Lemonade Gummies 2-Pack (100mg THC, 50mg CBD, 200mg CBN, 50mg CBG) still rose 14.6% at rank 5 off $59,043, implying consumer interest is concentrating around targeted multi-cannabinoid need-states rather than general 1:1 blends.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.