Where to Buy

Eaton Botanicals is stocked at 225 licensed dispensaries across New York, with the deepest coverage in New York, Queens, Brooklyn, Rochester, and Buffalo. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

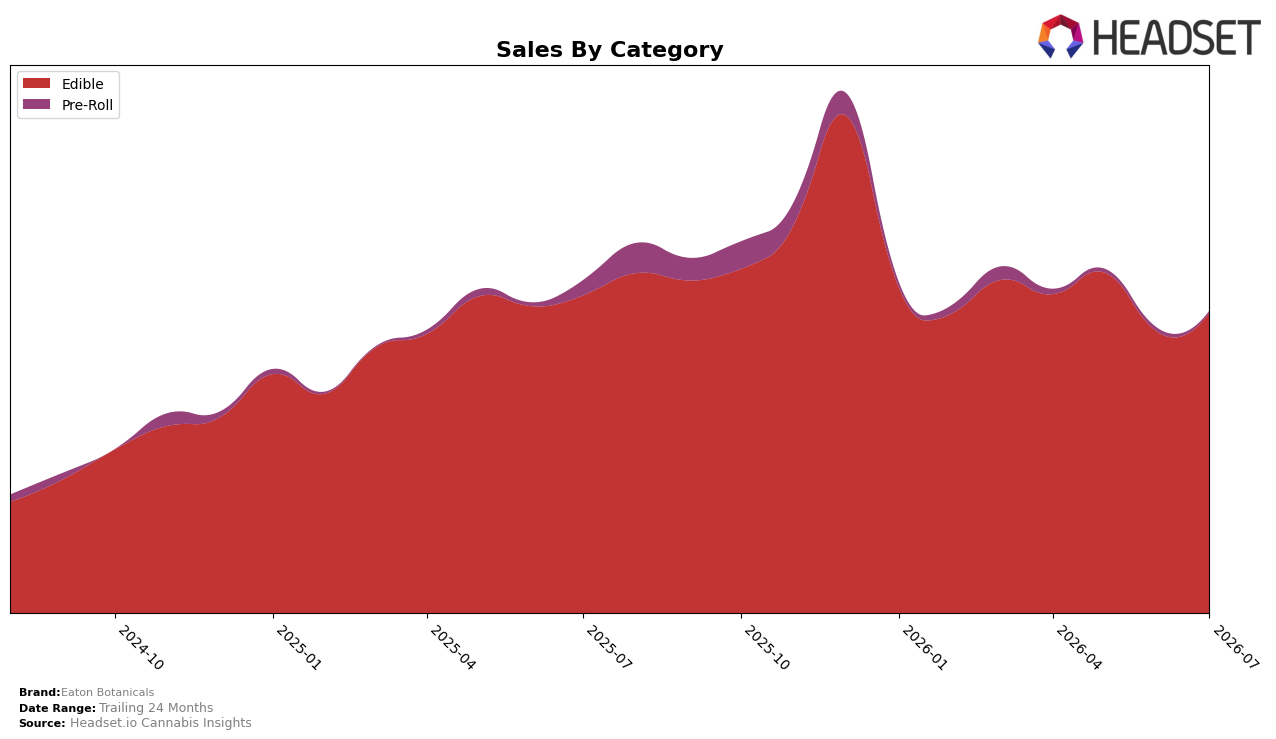

Eaton Botanicals concentrated 98.24% of July 2026 sales in Edible, with Pre-Roll at 1.76%, while Edible grew 7.08% month over month and fell 5.22% year over year versus Pre-Roll’s 29.93% month-over-month decline and 71.51% year-over-year drop; the aggregate brand sales contracted 8.94% year over year alongside a 0.11% average price decrease, and the Edible average price at $30.91 sat above the brand’s $30.42 blended level. Within New York Edible, the brand held rank 9, indicating deeper share concentration in a single category even as Pre-Roll retrenched, which implies near-term reliance on Edible volume recovery rather than multi-category breadth.

The mix shift—Edible up 7.08% month over month while Pre-Roll fell 29.93%, combined with Edible’s 5.22% year-over-year decline versus a 71.51% Pre-Roll decline—positions Eaton Botanicals to defend and potentially expand its rank 9 footprint in New York Edible if price discipline (brand average price down 0.11% year over year) is maintained and category elasticity favors mid-$30 price points. The pattern implies the brand should treat Pre-Roll as a low-impact tail (1.76% share) and concentrate promotional and assortment depth where 98.24% of sales already sit, because incremental Edible gains can offset the 8.94% year-over-year brand contraction more efficiently than reviving a subscale, highly volatile Pre-Roll line.

Competitive Landscape

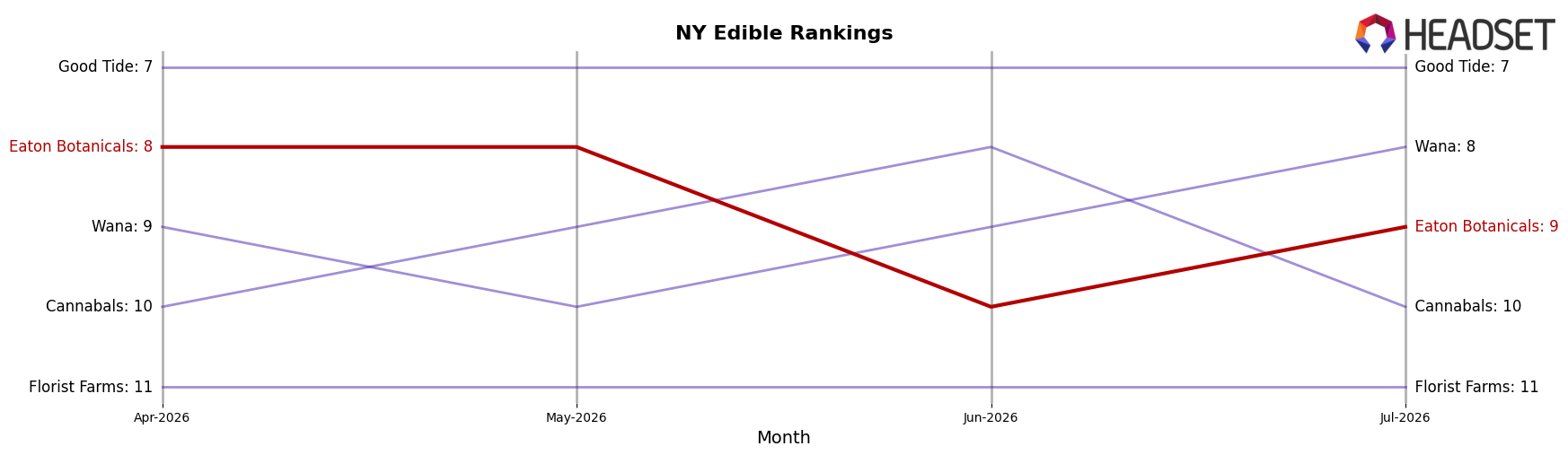

Eaton Botanicals ranks #9 in New York Edible for July 2026, slipping 1 position year over year from #8, after holding #8 three months ago and peaking at #7 in March 2026; by contrast, Off Hours fell from #1 to #2 with a 10.4% YoY sales decline while Wyld held steady at #3 alongside a 7.4% YoY sales increase, indicating that Eaton Botanicals’ mild rank erosion amid mixed competitor momentum implies the brand is losing relative velocity and must convert stability into share gains to avoid further drift from its March peak.

Notable Products

Fixer Upper - CBD/THC 1:1 Mango Ginger Gummies 20-Pack (100mg CBD, 100mg THC) marked the steepest decline at -14.1% MoM while dropping to rank 5, and Serenity Now - CBD/THC 4:1 Lemon Lavender Gummies 20-Pack (200mg CBD, 50mg THC) fell -10.6% at rank 3, signaling pressure within CBD-forward SKUs. In contrast, Nightly Nightcap - THC/CBN 1:1 Dark Cherry Gummies 20-Pack (100mg THC, 100mg CBN) climbed +34.4% MoM to hold rank 1 and Daily Elevation - CBG/THC 1:1 Peach Gummies 20-Pack (100mg CBG, 100mg THC) rose +10.7% at rank 2, while two Little Pandas Pre-Roll 5-Packs slid -26.4% and -45.8% at ranks 8 and 10. With eight of the top ten in Edibles and the sole dollar outlier at $137,948 coming from the leading Nightly Nightcap SKU, the mix implies Eaton Botanicals is tilting toward THC-led functional gummies while de-emphasizing Pre-Rolls and higher-CBD ratios.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.