Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Lost Farm is stocked at 1,431 licensed dispensaries across California, Michigan, and 9 other states, 546 of them in California, with the deepest coverage in Los Angeles, San Francisco, Sacramento, San Diego, and Santa Ana. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

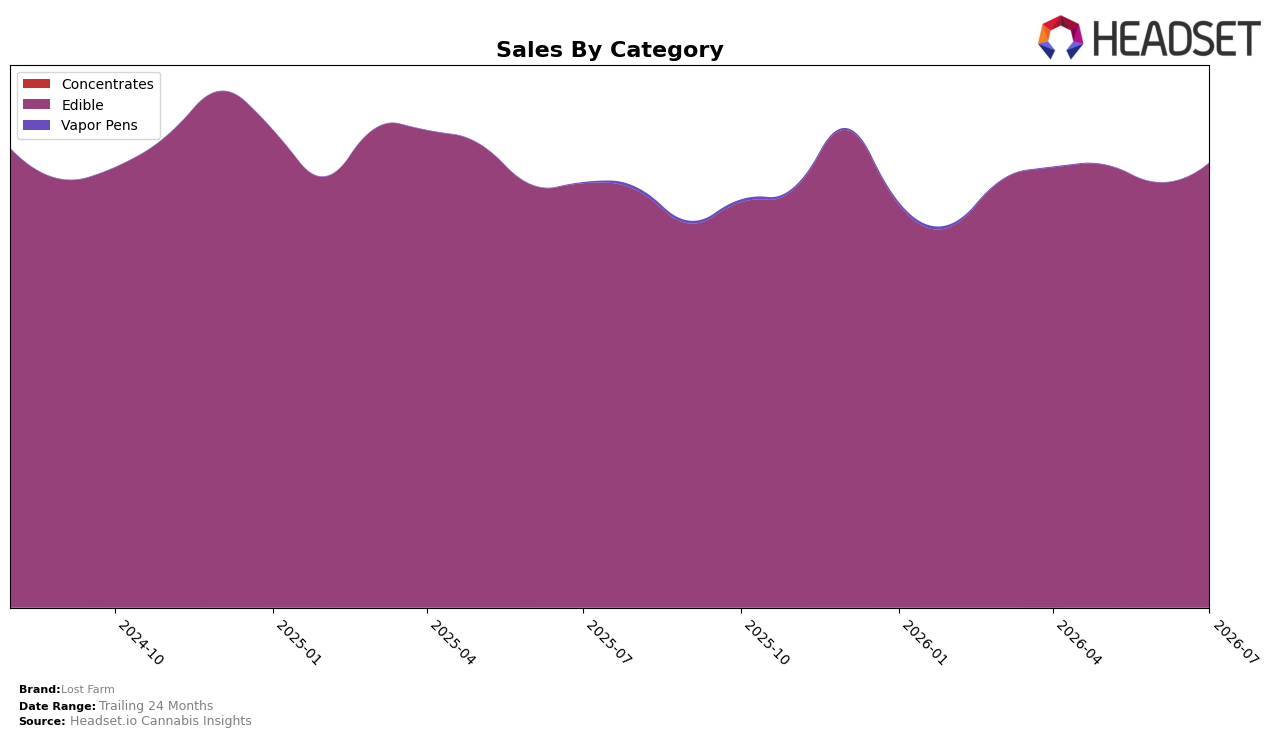

Edible accounted for 99.98% share in July 2026, up 4.81% year over year and 4.64% month over month, while average price slipped 1.20% YoY to $18.73 alongside a 4.64% MoM sales lift, indicating volume-led growth. Concentrates held 0.02% share with a 50.76% YoY increase but a 1.34% MoM decline and a far lower $9.70 average price, leaving mix concentration essentially unchanged at a 99.98%/0.02% split. The brand’s 4.64% YoY sales growth paired with a 4.38% decline over 24 months suggests recent recovery is driven by Edible momentum rather than mix expansion, implying near-term performance depends on sustaining Edible velocity while Concentrates remains immaterial to totals.

Maintaining rank 4 in Edible in July 2026 in California amid a 1.20% YoY price dip signals competitive traction via price-to-volume trade-offs, while Edible share density at 99.98% concentrates positioning in a single category. The 4.64% MoM sales rise in Edible against a 1.34% MoM dip in Concentrates indicates that incremental gains are coming from core SKUs, not diversification, and the 50.76% YoY uptick in Concentrates off a 0.02% base is too small to shift rank or mix. This pattern implies Lost Farm’s positioning is that of a category specialist in Edible where sustaining a top-5 rank hinges on defending price architecture and promo efficiency rather than expanding into peripheral formats.

Competitive Landscape

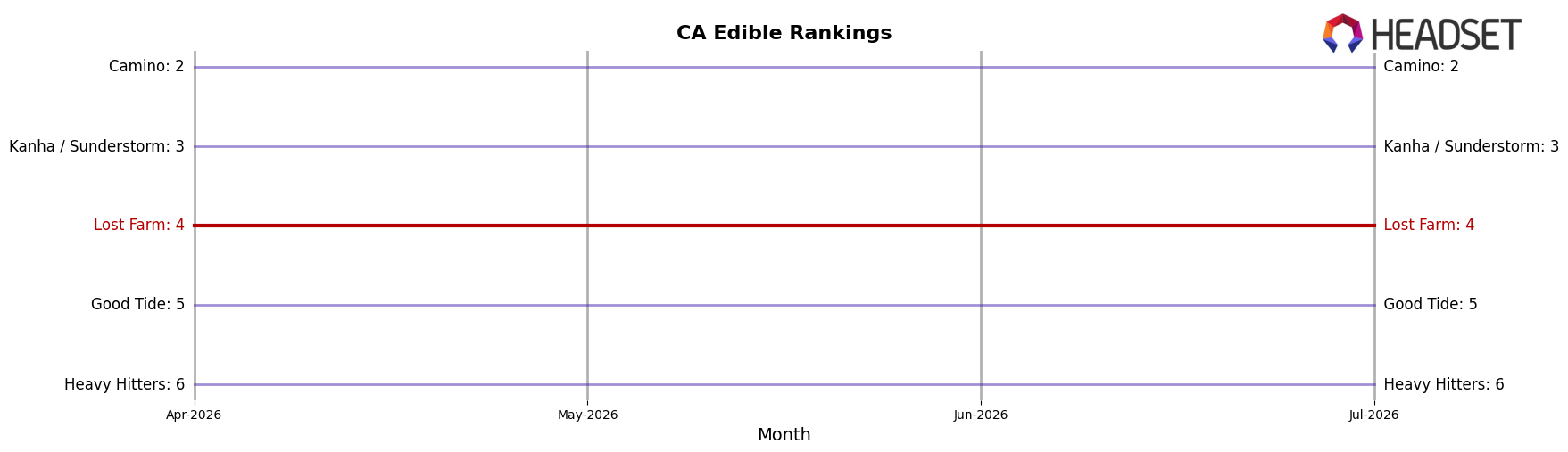

Lost Farm holds rank #4 in California Edible for July 2026, unchanged from #4 year over year, and flat versus three months ago at #4 as well; this stability contrasts with Wyld maintaining #1 while growing sales by 2.20% YoY and Camino holding #2 with a 14.77% YoY sales increase. With Kanha / Sunderstorm steady at #3 alongside a 14.64% YoY rise and Good Tide fixed at #5 despite a 22.07% YoY lift, Lost Farm’s unshifted #4 and new peak rank in July 2026 imply its share position is capped by faster-growing neighbors above and below, signaling a need to convert stable placement into upward mobility as competitors expand at double-digit rates.

Notable Products

Dark Cherry x Illuminati OG Live Rosin Gummies 10-Pack (100mg) posted the biggest movement in July 2026 with a +6.9% MoM gain as it climbed to rank 9, while Watermelon x Gelato Live Resin Fruit Chews 10-Pack (100mg) rose +5.5% MoM at rank 3, indicating momentum in both rosin and resin formats. In contrast, Raspberry x Wedding Cake Live Resin Gummies 10-Pack (100mg) declined -5.1% MoM at rank 7 as the top two SKUs slipped modestly (rank 1 at -1.7% MoM and rank 2 at -0.9% MoM), pointing to a reshuffle within the top tier rather than a category-wide drop. Eight of the top ten are Edible gummies or chews in 10-pack, 100mg formats, and the two functional SKUs each gained between +4.2% and +5.7% MoM, suggesting that flavor breadth and minor-cannabinoid differentiation are starting to carry more of the mix than legacy leaders. The pattern implies Lost Farm is tilting toward a diversified gummy portfolio where mid-rank climbers and functional variants capture incremental share from slightly softening flagships.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.