Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Jaunty is stocked at 337 licensed dispensaries across New York, with the deepest coverage in New York, Buffalo, Rochester, Queens, and Syracuse. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

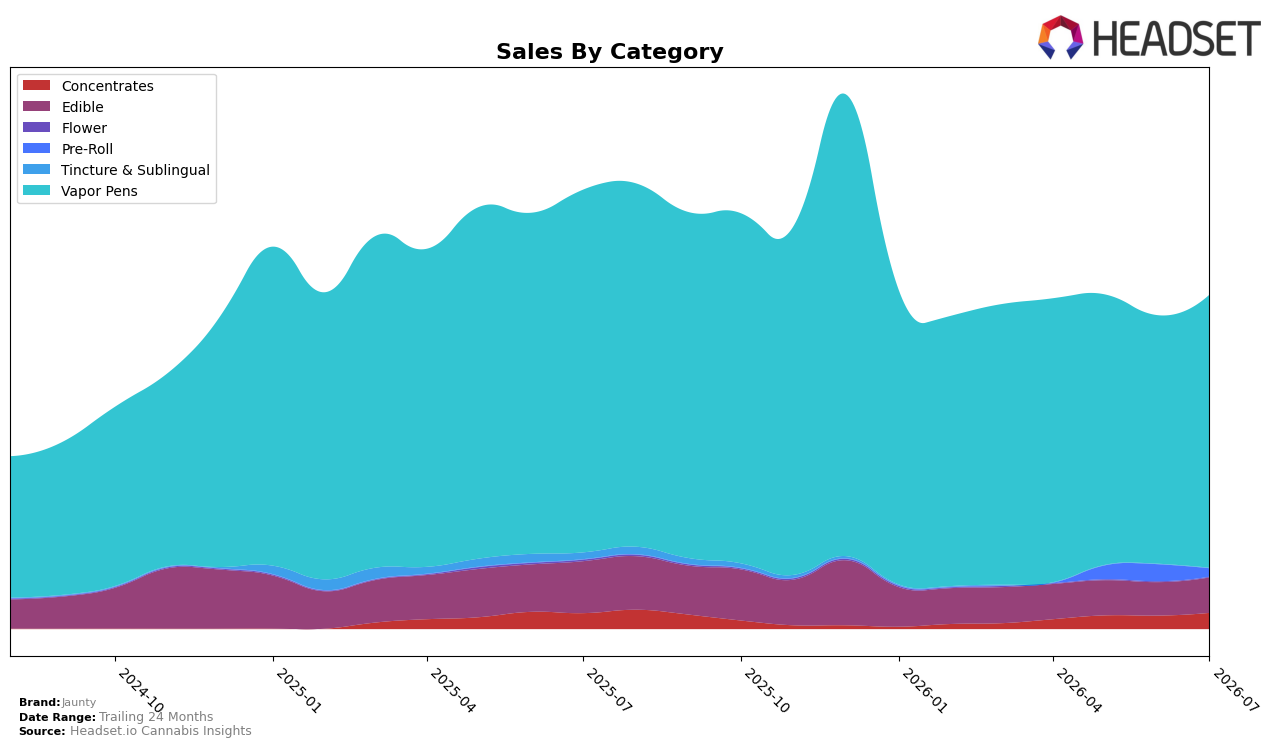

Jaunty concentrated 82.16% of July 2026 sales in Vapor Pens with a month-over-month gain of 9.88% but a year-over-year decline of 24.77%, while Edible held 10.56% share with 6.10% MoM growth against a 32.01% YoY drop. Concentrates, at 4.77% share, grew 20.71% MoM and 1.61% YoY, contrasting with Pre-Roll’s 2.41% share and a 51.80% MoM fall, and Flower’s 0.08% share with a 38.97% MoM and 74.84% YoY decline; Tincture & Sublingual remained negligible at 0.02% share despite a 142.15% MoM spike and a 98.81% YoY contraction. With Vapor Pens ranked 2 in New York and average prices down 11.60% YoY to $36.48, the pattern implies Jaunty’s scale is anchored in a single category that is stabilizing sequentially but compressing annually, while small but faster-moving niches like Concentrates are the only YoY offsets.

The mix shift implies Jaunty is trading deeper into value within Vapor Pens while losing breadth in Flower and Pre-Roll, which reduces cross-category capture even as sequential gains arrive from price-accessible formats. The 20.71% MoM increase and 1.61% YoY growth in Concentrates, alongside Vapor Pens’ 9.88% MoM rise and 24.77% YoY drop, suggest positioning that leans on core pen loyalty for volume while relying on Concentrates for incremental growth; however, the 51.80% MoM decline in Pre-Roll and 74.84% YoY slide in Flower indicate weakened entry points for new customers. Net, the pattern implies Jaunty’s defensible spot is a price-tempered Vapor Pens franchise in New York (rank 2) with a need to reinstate lighter-weight formats to prevent further category concentration risk.

Competitive Landscape

Jaunty sits at rank #2 in New York Vapor Pens in July 2026, down 1 position year over year but down from a peak rank of #1 reached in May 2026; over the last three months Jaunty slipped from #1 to #2 while Fernway moved from #3 year over year to #1 currently, and Jetty Extracts surged from #22 year over year to #4 alongside a 199.3% YoY sales jump. With Ayrloom declining from #2 to #3 on a -16.0% YoY sales change and Mfny (Marijuana Farms New York) holding at #5 with -7.9% YoY sales, the movement suggests Jaunty’s slight rank erosion is less about broad category softness and more about being outpaced at the top by faster climbers, implying the brand must counter accelerating competitor momentum to avoid further slippage from its prior #1.

Notable Products

Classic - Amnesia Haze Distillate Cartridge (1g) delivered the most notable movement in July 2026 with a 29.8% month-over-month increase, climbing to rank 6 while Classic - Sour Diesel Distillate Cartridge (1g) at rank 1 rose 9.1%, indicating momentum broadening beyond the top SKU. Vapor Pens occupy eight of the top ten, with Palms - Blue Dream Distillate Disposable (1.5g) up 18.5% at rank 4 and Classic - Pineapple Express Distillate Oil Cartridge (1g) up 14.3% at rank 5, while Classic- Blueberry Kush Distillate Cartridge (1g) slipped 5.6% at rank 7. The concentration in Vapor Pens alongside double-digit gains and minimal declines implies Jaunty is consolidating share around cartridge-led demand rather than diversifying toward Edibles in July 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.