May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

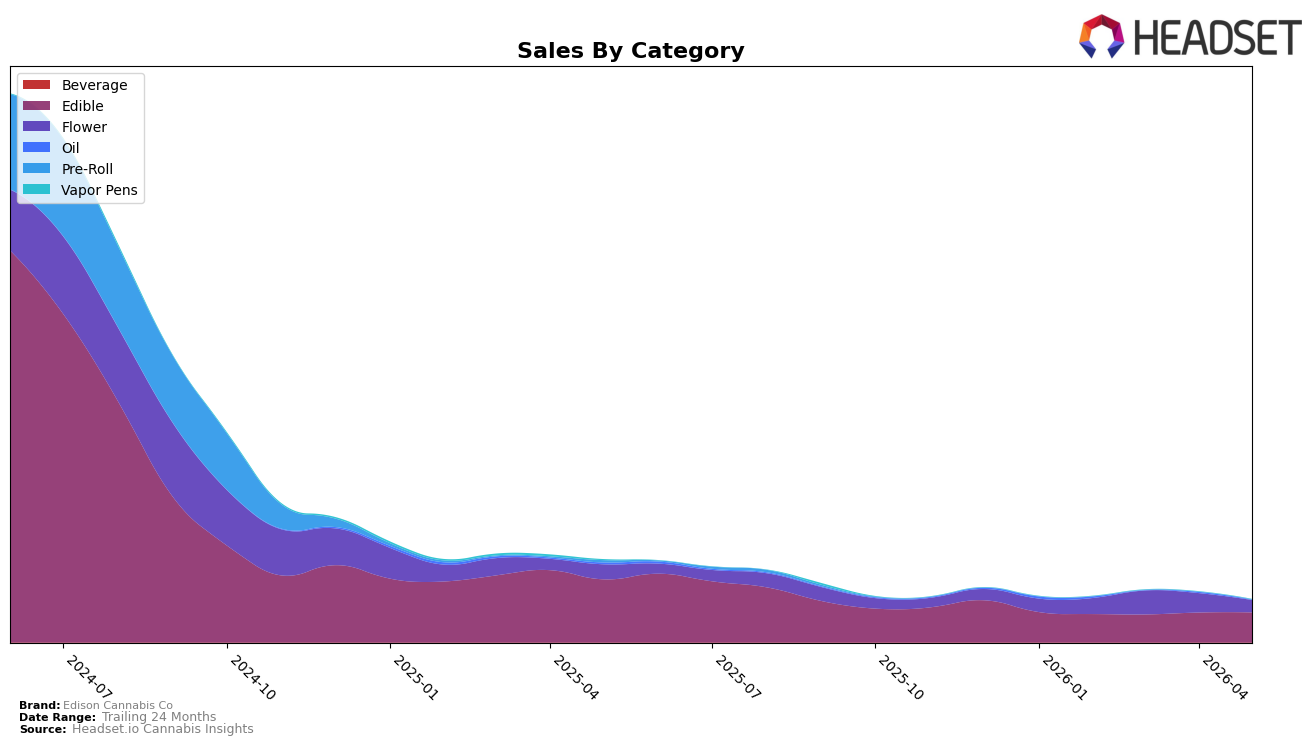

In May 2026, Edison Cannabis Co concentrated 71.25% of sales in Edible with a 0.45% MoM uptick but a -52.61% YoY decline, while Flower held 28.75% share with a -36.93% MoM drop and a -17.91% YoY contraction; the mix therefore pivoted further toward Edible even as both categories contracted YoY. Average price rose 150.77% YoY to $15.00, with Edible pricing at 11.26 and Flower at 84.64, and brand sales fell -48.74% YoY against a -92.18% 24‑month slide; this spread implies price-led dollar retention in Edible even as unit velocity likely softened.

Edison Cannabis Co’s tilt toward Edible at 71.25% share alongside a -36.93% MoM retreat in Flower indicates a defensive reallocation away from higher-priced, more volatile Flower and toward lower-priced Edible, and the 0.45% MoM gain in Edible versus the brand’s -48.74% YoY sales decline suggests the category is stabilizing the base. Holding rank 13 in Edible within Alberta while Flower contracts -17.91% YoY positions the brand as an Edible-led player whose pricing architecture (150.77% YoY increase to $15.00) prioritizes margin over unit scale; the implication is that near-term share defense will come from Edible depth rather than Flower breadth.

Competitive Landscape

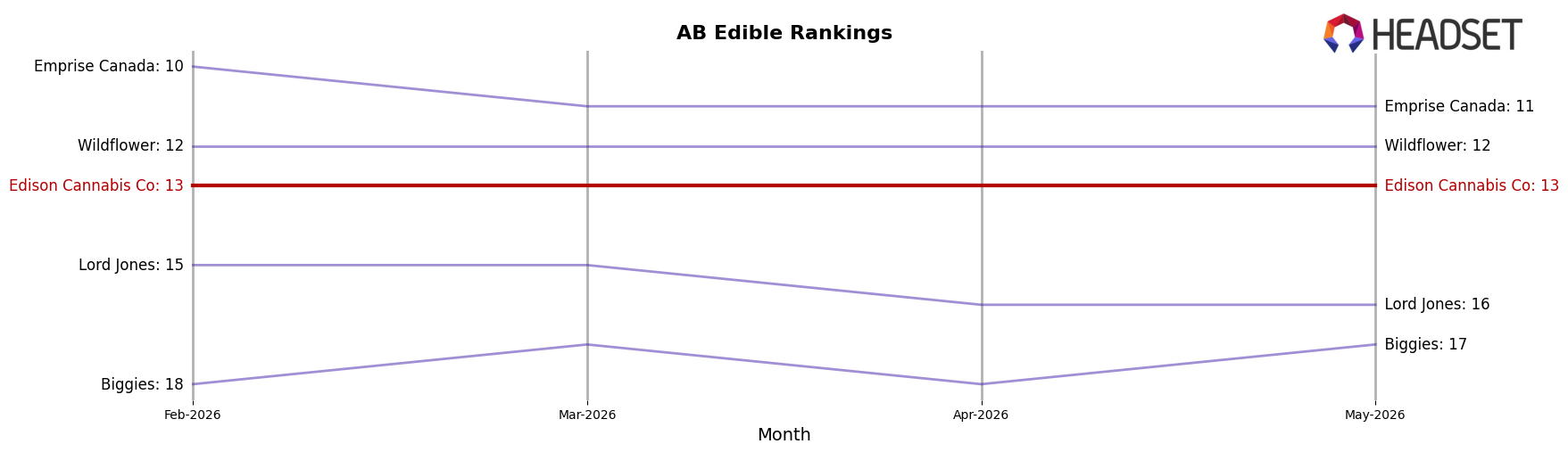

Edison Cannabis Co is ranked #13 in AB Edible in May 2026, a 1-position improvement from #14 year over year, while holding flat versus February 2026 at #13; this steadiness contrasts with Olli rising from #5 to #3 alongside a 53.6% YoY sales increase and Gron / Grön slipping from #3 to #4 with an 11.6% YoY decline, and both dynamics occurred as category leaders Spinach and Wyld held #1 and #2 with 21.2% and 17.9% YoY growth respectively; given Edison Cannabis Co’s current #13 versus a historical peak of #6 in September 2024 and a 0-position move over the last three months, the pattern implies the brand is stabilizing in lower-teens share-of-shelf positions while faster-rising peers compress headroom for upward mobility.

Notable Products

Mac n' Cheese Milled (7g) posted the steepest decline in May 2026 at -76.3% MoM while slipping to rank 9, and Blueberry Dream (28g) fell -33.4% to rank 5, indicating a pullback in Flower even as Jolts - Sativa Electric Lemon Lozenges 10-Pack (100mg) rose 31.5% at rank 10. Edibles occupied 7 of the top 10 positions and the two highest ranks, with Sonics - CBD/THC 1:1 Kiwi Berry Burst Gummies 2-Pack (10mg CBD, 10mg THC) up 3.8% at rank 1 and Sonics - CBD/THC 1:1 Red Razz Chiller Gummies 2-Pack (10mg CBD, 10mg THC) up 13.7% at rank 2, while single-unit Jolts - Sativa Electric Lemon Lozenge (10mg) dropped -54.9% at rank 8. The contrasting +31.5% gain for the 10-pack vs. a -54.9% slide for the single suggests demand consolidating into multi-pack Edibles, and the dual Flower declines imply a strategic tilt away from Flower toward scaled Edible formats where rank momentum is concentrating.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.