Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

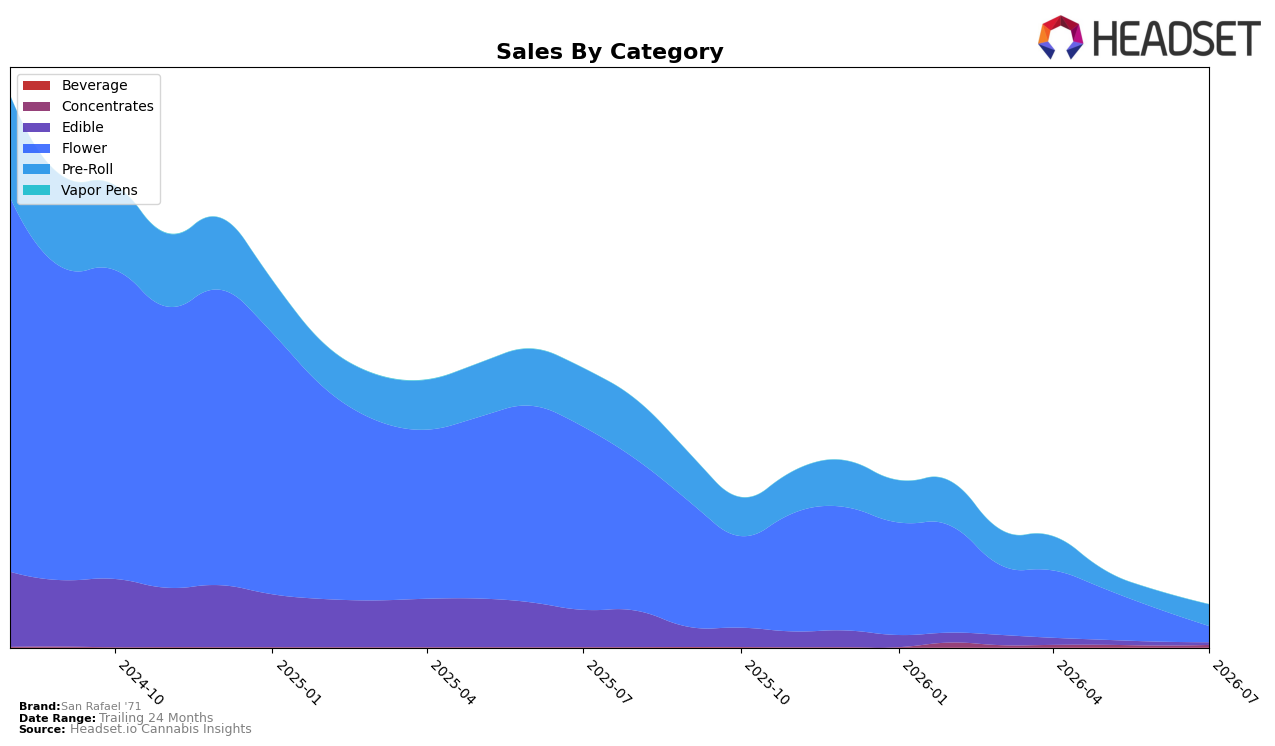

In July 2026, San Rafael 71 concentrated over half of brand sales in Pre-Roll at 50.99% share, while Flower held 37.83% and Edible 5.61%, indicating a shifted mix as Flower declined. Pre-Roll sales were down 63.42% year over year but up 20.56% month over month, whereas Flower fell 91.35% year over year and 51.35% month over month, and Concentrates—now 5.53% share—grew 32.08% month over month despite lacking a year-over-year baseline. This mix realignment, paired with a 14.67% year-over-year rise in average price and an 87 rank in Pre-Roll within Alberta, implies the brand is consolidating around a narrower Pre-Roll core while de-emphasizing underperforming Flower and Edible lines.

The directional spread—Pre-Roll up 20.56% month over month versus Flower down 51.35% month over month—signals short-term momentum concentrated in a single category even as total brand sales are down 84.97% year over year. With Concentrates adding 32.08% month-over-month growth and Beverage only 0.04% share despite a 5.35% month-over-month lift, the portfolio tilt suggests a positioning pivot toward format-led value where price points near $20.34 coexist with premium pockets (Flower average price $32.03), implying near-term gains will depend on sustaining Pre-Roll velocity while using Concentrates as a secondary growth lane rather than broad multi-category expansion.

Competitive Landscape

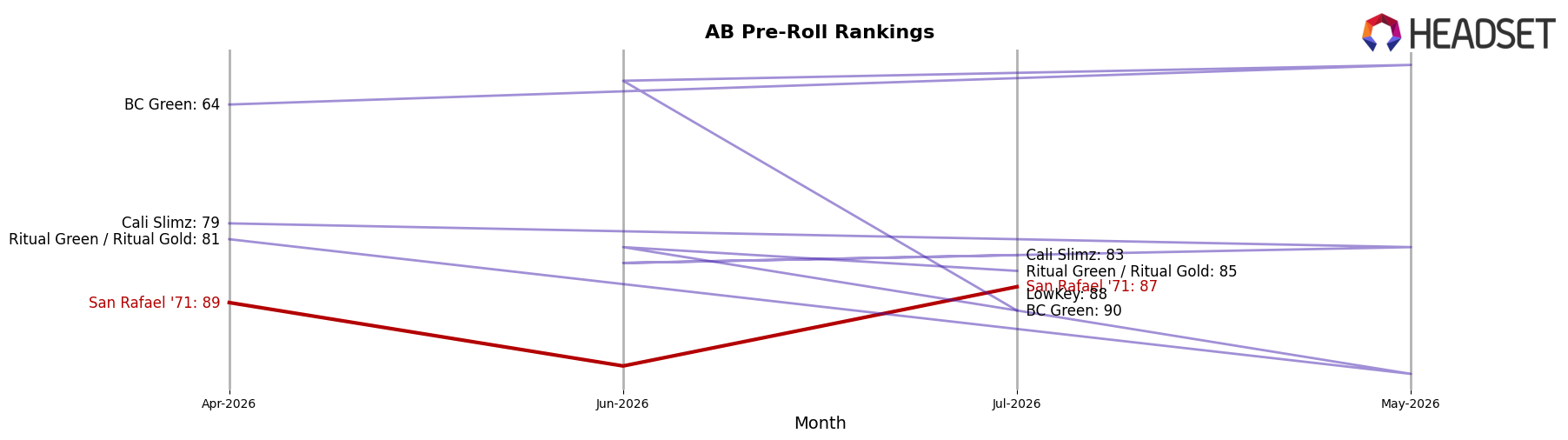

San Rafael '71 is ranked #87 in AB Pre-Roll in July 2026, down 8 positions year over year from #79, while improving 2 ranks versus April 2026 when it stood at #89, and far off its peak of #41 from July 2024; meanwhile, category leaders are diverging, as General Admission held #1 but with a -14.5% YoY sales change, and Back Forty / Back 40 Cannabis moved from #6 to #2 with +34.3% YoY growth. With Space Race Cannabis slipping from #2 to #3 alongside a -37.9% YoY sales trend while Thumbs Up Brand jumped from #19 to #5 on +138.3% YoY, the mix at the top is fluid, and San Rafael '71’s drift from its July 2024 peak to #87—despite a modest quarter-over-quarter rank lift—implies that without a differentiated play against faster risers, its share will continue to compress as momentum concentrates among a few accelerating competitors.

Notable Products

Pink Diesel '71 (3.5g) posted the steepest move in July 2026 with a -52.9% month-over-month drop and slid to rank 2, while Sour Blueberry Live Resin Gummies 4-Pack (10mg) also declined -12.8% and sat at rank 3. Ponderosa Pine Pre-Roll 5-Pack (2.5g) rose +35.9% month over month to hold rank 1, and Black Jelly (3.5g) fell -26.2% at rank 9, signaling uneven traction across Flower versus Pre-Roll. Three of the top ten are Pre-Roll SKUs, and Edibles occupy ranks 3 and 4 with -12.8% and -34.0% declines respectively, concentrating weakness in ingestibles even as the leading Pre-Roll accounted for $44,111. The pattern implies San Rafael '71 is tilting toward inhalables-led velocity, with Pre-Rolls consolidating share while Flower and Edibles require repositioning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.