Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

Wildflower’s category mix in June 2026 tilted toward Flower at 54.34% share, with Flower up 676.81% year over year and 80.61% month over month, while Topical held 29.47% share with 354.86% YoY and 8.18% MoM. Edible slipped to 16.13% share with -4.64% YoY and -7.51% MoM, and Capsules contracted to 0.06% share with -73.90% YoY and no reported MoM. Across the portfolio, brand sales rose 216.99% YoY alongside a 44.03% YoY rise in average price to $22.78, indicating mix-led and pricing-driven expansion concentrated in Flower and Topical; the pattern implies Wildflower is reallocating demand from Edible and Capsules into higher-growth inhalable and wellness formats.

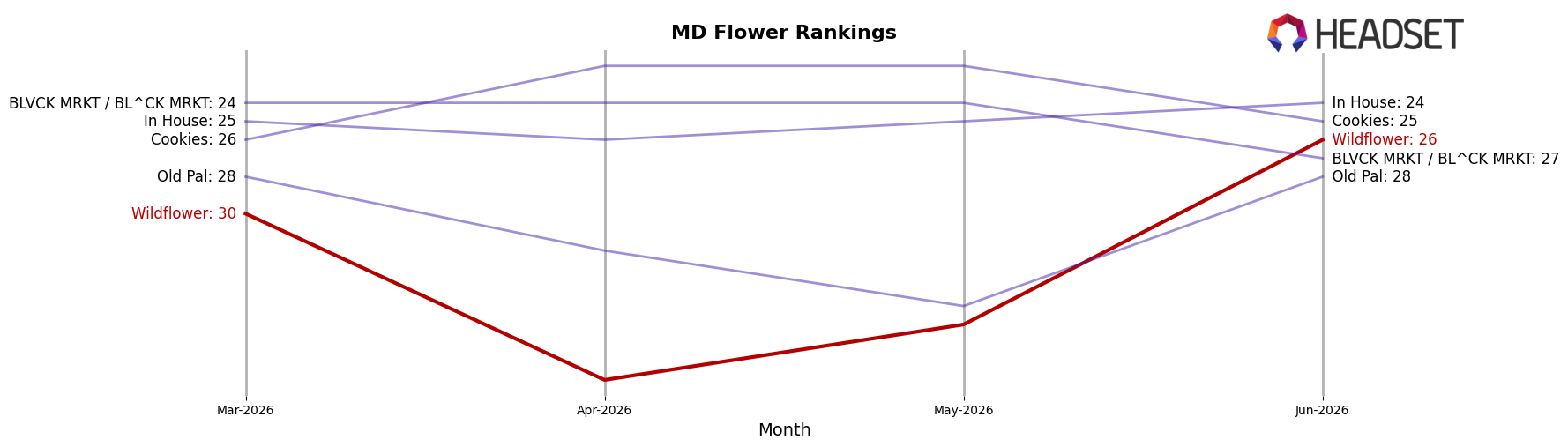

This shift positions Wildflower to compete more directly in inhalables where its rank in Flower sits at 26 in Maryland, aided by an 80.61% MoM surge that expands share while Topical’s 8.18% MoM adds breadth. With Edible declining -7.51% MoM and -4.64% YoY even as Flower’s share reached 54.34%, the brand is concentrating on categories that scale faster at current price points, implying a strategy to trade up consumers from lower-priced Edible (average $8.95) toward higher-value Flower and Topical (average $26.65 and $53.93) to sustain growth and improve positioning within Flower in Maryland.

Competitive Landscape

Wildflower sits at rank #26 in June 2026, improving 25 positions from #51 year over year and gaining 4 spots from #30 in March 2026; this new peak rank of #26 in June 2026 contrasts with SunMed holding #1 both year over year and currently while posting +13.4% YoY sales, and RYTHM advancing from #3 to #2 with +42.7% YoY sales, indicating Wildflower’s rank climb is occurring alongside faster-moving leaders and implies share gains are likely concentrated in the mid-tier rather than displacing the top five.

Notable Products

Starburst (3.5g) posted the largest month-over-month surge at +601% to reach rank 5, while Lemondary (3.5g) also jumped +106% to rank 6, indicating a rapid pivot toward specific Flower SKUs. In contrast, Black Maple (3.5g) fell -82% to rank 9 and Dogwalker (3.5g) dropped -63% to rank 8, even as Sweet Dreams - CBD/CBN/THC 1:1:2 Goji Berry Chews 5-Pack (5mg CBD,5mg CBN,10mg THC) held rank 1 with a -7.5% dip. With six of the top ten coming from Flower, the category mix is consolidating around a few breakout strains rather than broad-based Flower strength, signaling a shift in Wildflower’s commercial direction toward betting on momentum winners while managing volatility in the long tail.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.