Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

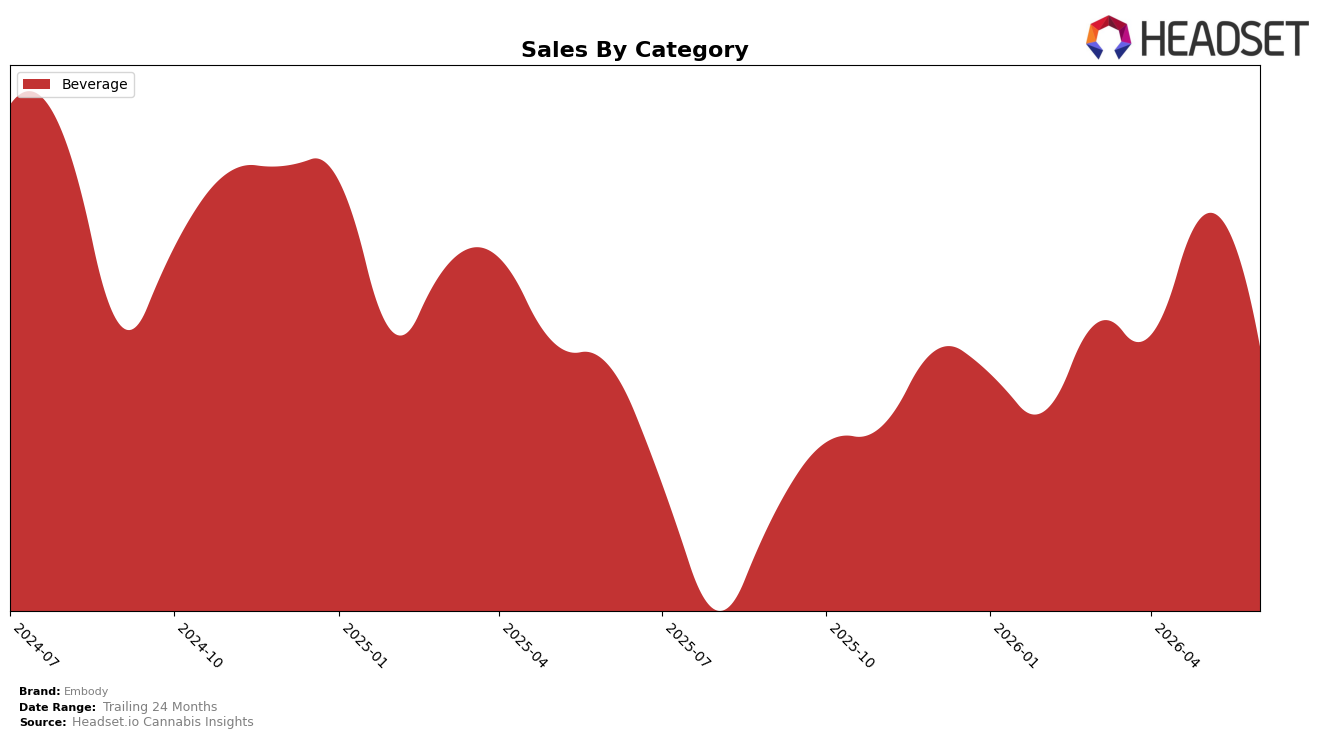

Embody operated as a single-category brand in Beverage with a 100.0% mix in June 2026, posting 3.06% year-over-year sales growth alongside a -17.68% month-over-month decline and a -0.95% average price change YoY; this combination implies a volume-led YoY uptick but a recent pullback in monthly velocity. Within Ontario Beverage, the brand sat at rank 23 in June 2026 while average price held at $8.05 and the 24-month sales trajectory registered -19.70%, indicating accumulated share pressure despite the current-year YoY gain.

The shift from +3.06% YoY to -17.68% MoM within a 100.0% Beverage concentration suggests sensitivity to short-cycle demand and limited diversification levers, positioning Embody as a value-anchored Beverage player rather than a cross-category hedge. Holding rank 23 in Ontario while average price declined -0.95% YoY and sales contracted -19.70% over 24 months implies a trade-off: pricing discipline may preserve entry-level demand, but without mix expansion beyond Beverage or improved monthly sell-through, the brand’s position risks drifting toward lower-tier share rather than climbing the category ranks.

Competitive Landscape

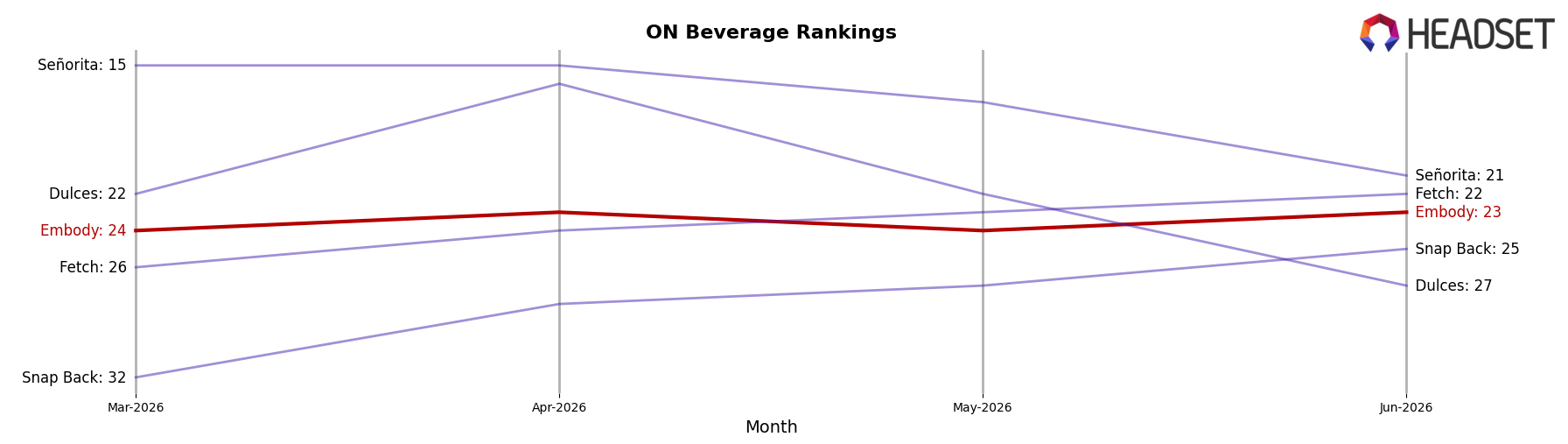

Embody sits at rank #23 in ON Beverage for June 2026, improving 4 places year over year from #27, yet edging down 1 spot versus March 2026 when it ranked #24; the brand’s best position was #21 in December 2025, placing its current level 2 ranks below that peak. Competitive movement is polarized: XMG held at #1 year over year while its sales fell 37%, and TeaPot climbed from #10 to #5 with 130% YoY growth, indicating Embody’s modest rank gain is occurring amid both contraction at the top and acceleration mid‑tier. The pattern implies Embody’s upward YoY trajectory is stability-driven rather than breakout, and maintaining or extending share likely depends on capturing spillover from top-tier declines faster than rising mid-pack brands.

Notable Products

Embody's CBD/THC Blood Orange + Rosemary Tea (40mg CBD, 2mg THC, 355ml) posted the steepest June 2026 movement with a -59.6% month-over-month decline and fell to rank 2, indicating a sharp pullback in a previously higher-velocity SKU. In contrast, CBD/THC Peach + Ginger White Sparkling White Tea (40mg CBD, 2mg THC, 355ml) held rank 1 with a -6.0% month-over-month dip and approximately $18,241 in sales, pointing to resilience at the top despite softness. With both top-2 positions occupied by Beverage SKUs, the category concentration remains high even as volatility widens between the leader and the follower, implying Embody’s mix is anchored in beverages but requires SKU-level pacing adjustments rather than category shifts.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.