Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

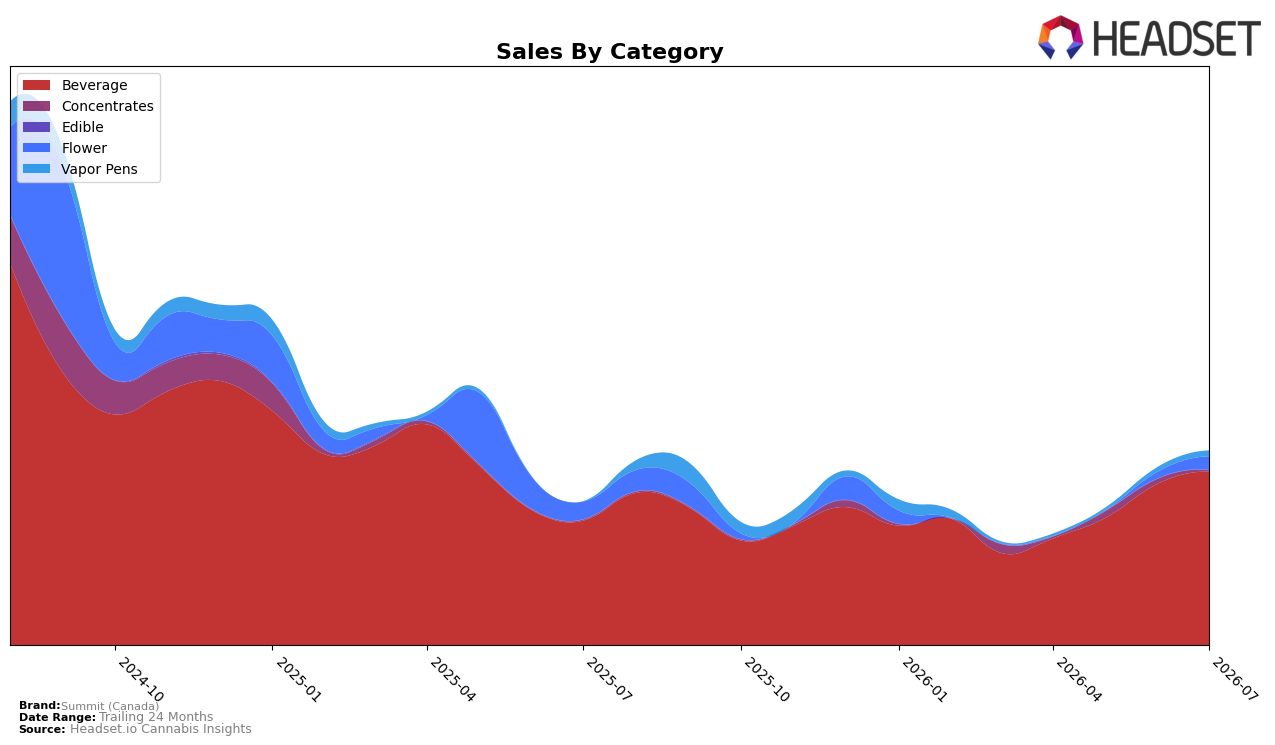

In July 2026, Summit (Canada) concentrated 89.73% of sales in Beverage, where year-over-year growth ran 39.48% and month-over-month rose 7.53%, while Flower held 6.82% share with a -24.07% year-over-year change but a 109.65% month-over-month surge. Vapor Pens accounted for 2.89% share with a 24.24% month-over-month lift and no comparable year-over-year baseline, and Concentrates sat at 0.57% share with 63.22% year-over-year growth but a -76.68% month-over-month drop. With Beverage ranked 10th in Alberta and the brand’s overall average price up 6.79% year-over-year to $7.51, the pattern implies Beverage remains the scale engine while Flower’s sharp month-over-month rebound and Vapor Pens’ sequential gains suggest cautious diversification from a Beverage-dominant base.

The mix shift implies Summit (Canada) is reinforcing a value-forward Beverage position—Beverage pricing at an average $7.08 alongside 39.48% year-over-year and 7.53% month-over-month growth—while testing higher-ticket adjacency: Flower at a $13.68 average and Vapor Pens at $25.06 collectively expanded their combined share to 9.70% with triple- and double-digit month-over-month increases. The divergence—Flower’s -24.07% year-over-year versus 109.65% month-over-month and Concentrates’ 63.22% year-over-year versus -76.68% month-over-month—signals episodic rather than steady traction outside Beverage, implying the near-term positioning hinges on defending a top-10 Beverage foothold in Alberta while selectively scaling the two categories showing immediate sequential demand without diluting the 89.73% Beverage center of gravity.

Competitive Landscape

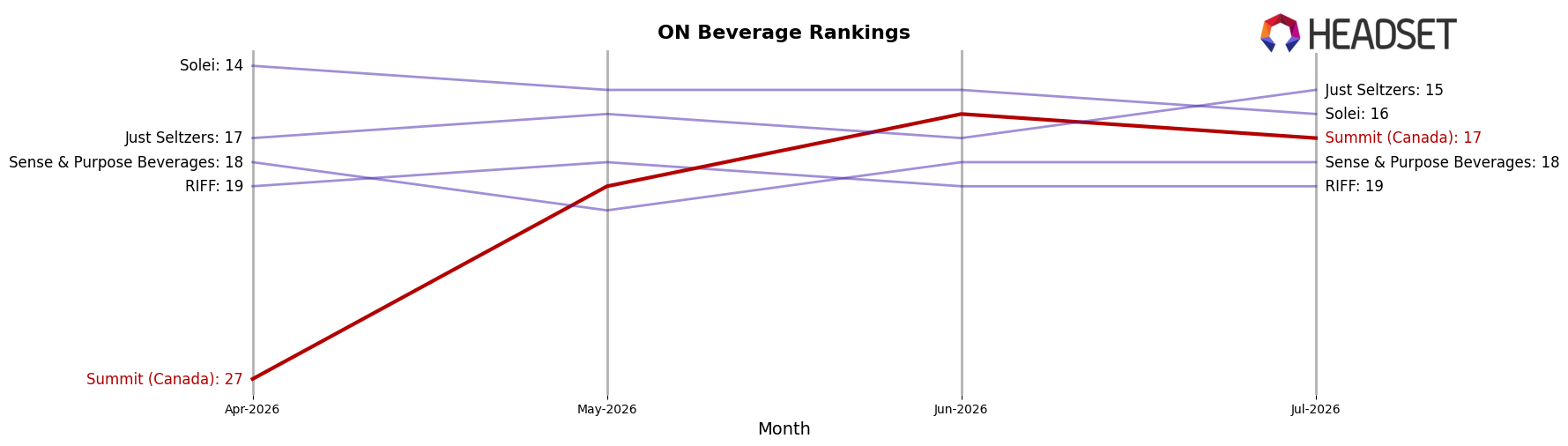

Summit (Canada) sits at #17 in ON Beverage in July 2026, improving 15 spots from #32 year over year, but slipping 1 rank from its #16 peak in June 2026; over the last three months the brand advanced 10 places from #27 to #17, while category leaders reshuffled as Versus climbed from #3 to #1 and XMG fell from #1 to #2 with a -37.2% YoY sales change. In the same window, Ray's Lemonade moved from #5 to #4 on +28.7% YoY and Mary Jones rose from #8 to #5 on +56.1% YoY, indicating that Summit (Canada)’s rapid climb from #32 to #17 is outpacing mid-tier peers but its slight dip from June 2026 signals a need to convert momentum into sustained top-15 presence.

Notable Products

Trop Cherry Live Resin Cartridge (1g) posted the largest month-over-month gain at +312.2% while sitting at rank 6, outpacing Black Inferno Popcorn (3.5g) at +109.7% in rank 4 and contrasting with Apple Pie Iced Tea (10mg THC, 355ml) at -32.4% in rank 8. Pink Lemonade (10mg THC, 12oz, 355ml) held rank 1 with +11.7% and Lemonade Iced Tea (10mg THC, 355ml) held rank 2 with +9.2%, and five of the top ten are Beverage SKUs, indicating category depth alongside emerging momentum in Vapor Pens and Flower. The pattern implies Summit (Canada) is leveraging a beverage-led base while testing higher-velocity upside in adjacent inhalables to diversify growth beyond seasonal drink demand.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.