Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

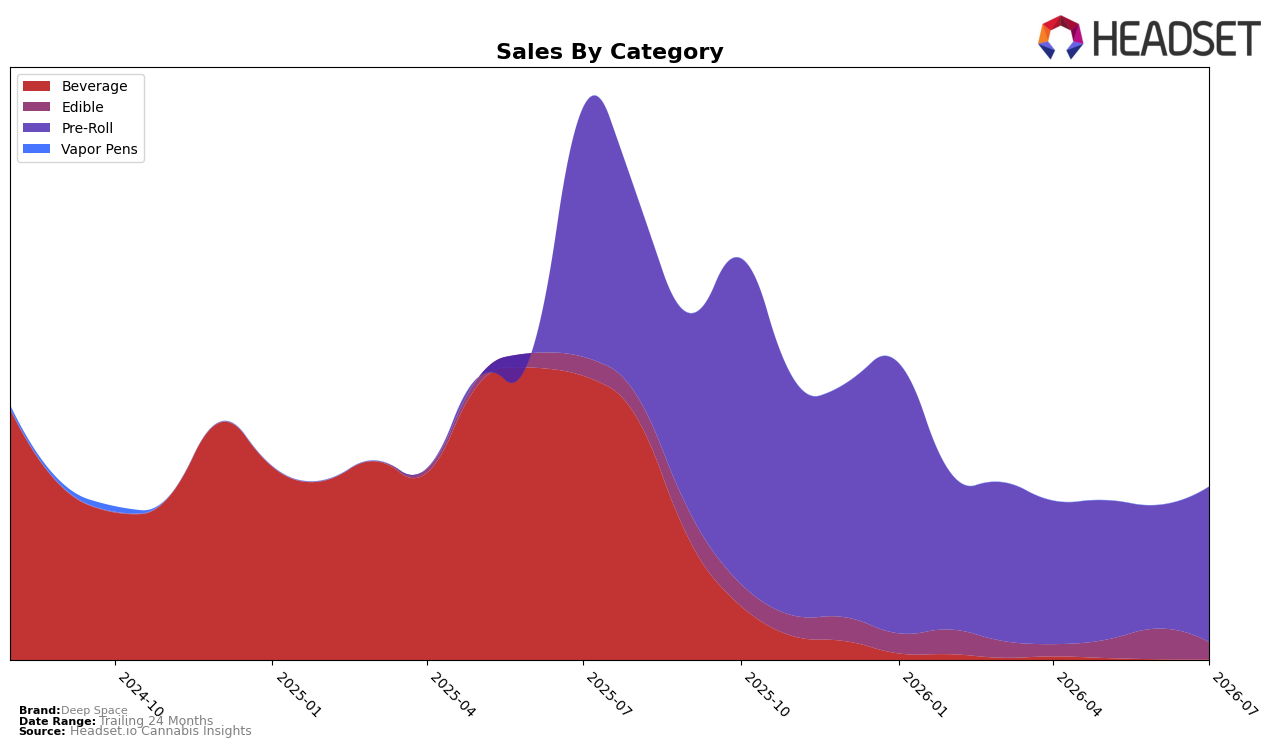

In July 2026, Deep Space concentrated 89.95% of sales in Pre-Roll, up 25.86% month over month while still down 37.62% year over year, signaling a rebound concentrated in a single format; Edible held 9.81% share with a 44.14% month-over-month decline and a 9.49% year-over-year decline, narrowing its role in the mix. Beverage shrank to 0.25% share with a 22.17% month-over-month drop and a 99.85% year-over-year decline, effectively exiting the category. With total brand sales down 68.72% year over year alongside a 29.45% increase in average price, the pattern implies a pivot toward higher-priced Pre-Roll units while de-emphasizing Edible and Beverage to stabilize near-term volume through a single-category lift.

The tilt toward Pre-Roll expansion at 25.86% month over month amid a 44.14% month-over-month contraction in Edible and a 99.85% year-over-year collapse in Beverage suggests a deliberate narrowing to defend relevance where velocity is recoverable. Given Saskatchewan positioning in Edible lacks a rank and Edible now represents just 9.81% of sales, Deep Space reduces exposure to a category where it carries limited placement while leaning into a Pre-Roll price architecture at an average of 28.07 that can sustain share at 89.95%. The implication is a focused-brand stance: consolidate presence in one lead format to arrest overall declines despite a 37.62% year-over-year drop in that format, accepting reduced breadth (0.25% Beverage share) to trade off for mix-driven price realization.

Competitive Landscape

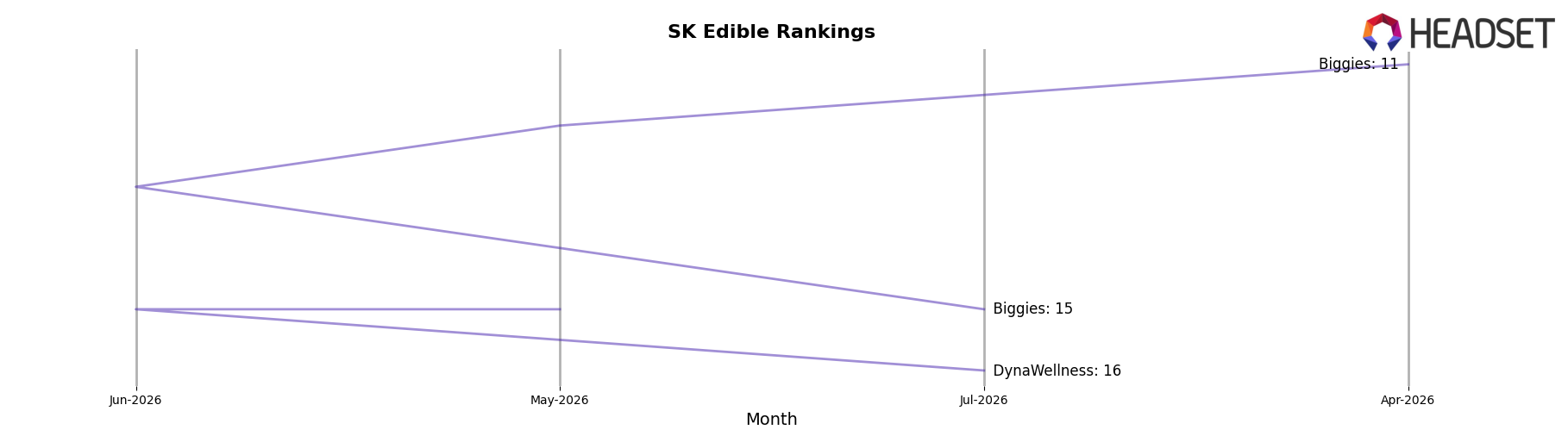

Deep Space is ranked #17 in SK Edible in July 2026, down 5 positions year over year from #12, and flat versus April 2026 at #17; the brand’s peak of #12 in September 2025 underscores a five-rank slide since that high. Meanwhile, Wyld held #1 year over year at #1 despite a -9.1% YoY sales change, Spinach inched up from #3 to #2 on +6.0% YoY sales, and Shred slipped from #2 to #3 with -18.1% YoY sales, while Wana jumped from #10 to #4 on +546.9% YoY sales; these moves indicate Deep Space is losing relative rank to both stable leaders and fast risers despite mixed category momentum, implying that without a catalyst the brand is likely to remain mid-pack or drift lower.

Notable Products

Space Propulsion - Sour Strawberry Void Gummy (10mg) posted the steepest decline at -91.14% MoM and fell to rank 4, while Space Propulsion - Sour Pulsar Peach Gummy (10mg) dropped even further at -98.06% MoM at rank 6, together signaling a sharp retreat for Edibles. In contrast, Milky Way Melon Infused Pre-Roll 3-Pack (1.5g) surged +45.11% MoM to rank 2, narrowing the gap to the rank 1 Xpress - Limon Splashdown Gummy (10mg) despite that leader sliding -33.04% MoM on just $8,646 in July 2026. With two of the top three positions held by Pre-Roll SKUs, the mix is tilting toward inhalables and away from Edibles, implying resource allocation should shift to formats with momentum and de-risk exposure to fast-eroding gummy lines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.