Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

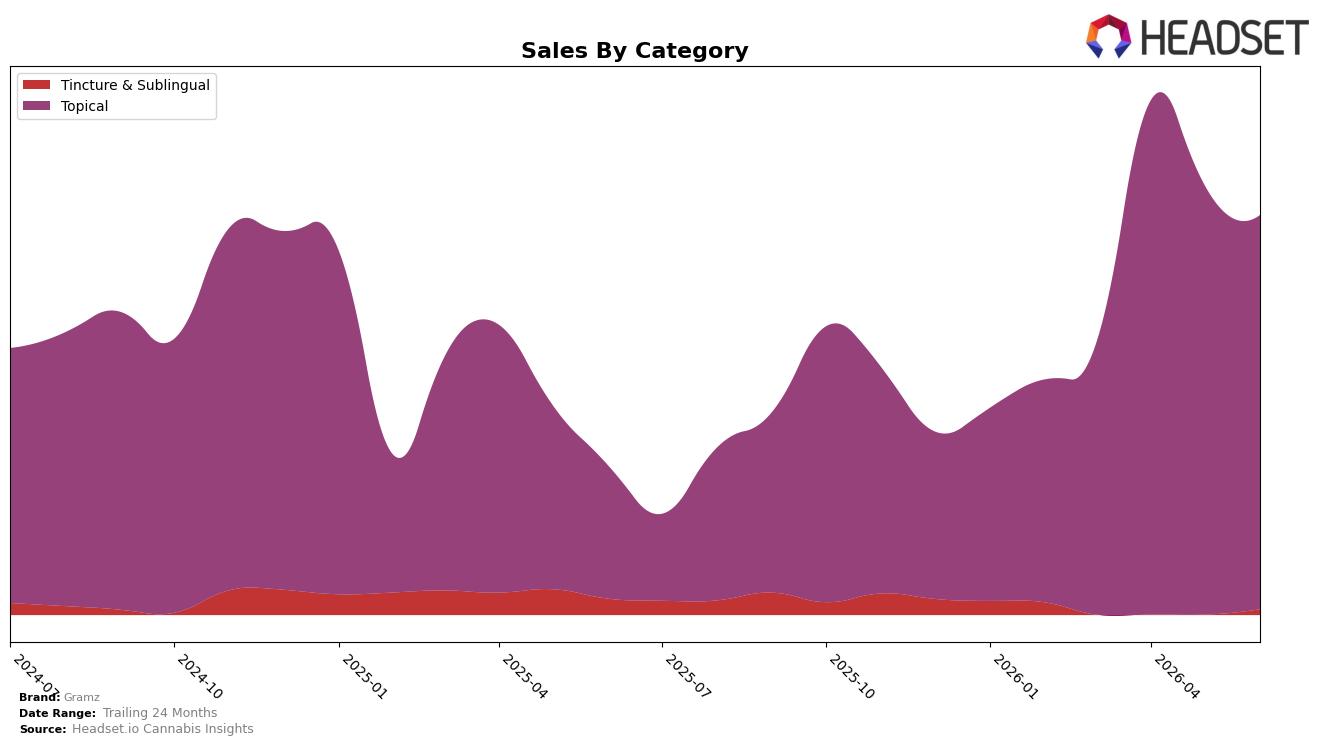

Gramz concentrated 98.65% category share in Topical during June 2026, with Topical sales up 196.84% year over year but down 8.22% month over month, while Tincture & Sublingual held 1.35% share with a 66.14% year-over-year decline and no measurable month-over-month trend. Average price rose 3.73% year over year to $38.52, and within Topical the average price sat at $38.98, indicating a slight premium over the brand average. These shifts imply Gramz is doubling down on a single-category footprint while absorbing short-term monthly volatility, and the mix suggests prioritization of higher-priced Topical over lower-priced Tincture & Sublingual as a deliberate margin and rank play.

Within Arizona Topical, Gramz held rank 3, aligning with a 196.84% year-over-year surge in its core category even as the 8.22% month-over-month contraction signals sensitivity to near-term demand or promo cadence. The 1.35% share in Tincture & Sublingual alongside a 66.14% year-over-year decline indicates de-emphasis of peripheral formats, while the price delta between $38.98 in Topical and the $20.76 average in Tincture & Sublingual narrows the brand’s positioning toward premiumized therapeutic formats. The pattern implies a strategy anchored in maintaining a top-3 Topical position through mix concentration and modest price elevation, accepting subscale presence in adjacent formats to protect category authority.

Competitive Landscape

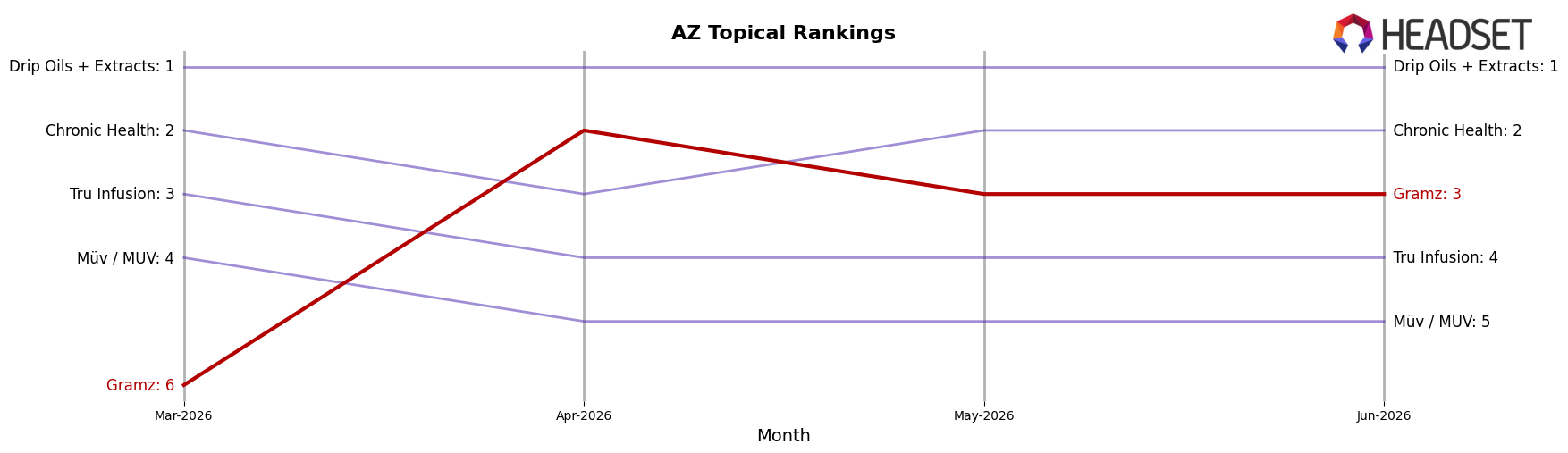

Gramz ranks #3 in AZ Topical in June 2026, improving 4 positions year over year from #7 and rising 3 spots since March 2026 from #6, while peaking at #2 in April 2026; by contrast, Drip Oils + Extracts held at #1 year over year with +18.9% sales YoY and Chronic Health stayed at #2 despite a -9.3% sales YoY change, and Tru Infusion remained #4 with +8.9% sales YoY, indicating that Gramz’s rank gains are coming from positional shifts above and below rather than broad category churn; the pattern—up 4 ranks YoY but off the April 2026 peak by 1 position—implies momentum toward the top tier with headroom constrained by a stable #1 and a flat #2 neighbor.

Notable Products

CBD/THC 1:1 Herbal Lotion (300mg CBD, 300mg THC) led June 2026 by rank 1 but contracted by 9.2% month over month while the category runner-up fell 5.2% at rank 2, indicating the flagship’s pullback outpaced the tier below and tightened the top spread. CBG/THC 1:2 G9 Herbal Aphrodisiac Libido Booster (50mg CBG, 100mg THC) rose 16.5% and held rank 3, yet that gain did not offset the leader’s decline given $28,420 concentrated in the top SKU and only 1,148 units of revenue in the rising item. Four of the top ten are Topical SKUs and they occupy ranks 1–3 with one Tincture & Sublingual at rank 4, so mix remains weighted to Topicals despite a 9.2% downtick at the top and a 5.2% slip in the second slot.

The pattern implies Gramz is reliant on a single Topical leader with softening momentum, and near-term commercial direction will hinge on sustaining the 16.5% growth in the third-ranked Topical while reducing exposure to a rank-1 product that is trending down 9.2% month over month.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.