Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

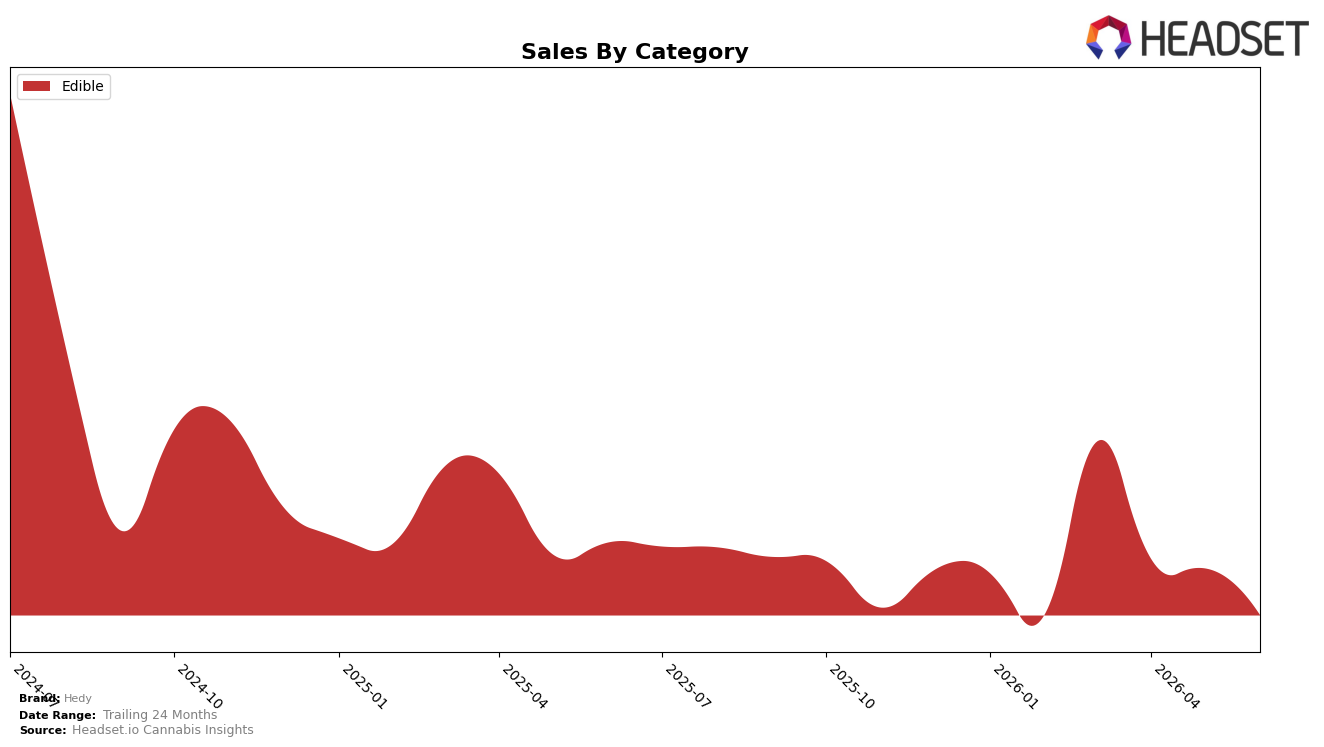

In June 2026, Hedy operated as a single-category brand with Edible accounting for 100.0% of sales, while brand sales declined 19.35% year over year and 13.38% month over month. Average price decreased 2.09% year over year alongside a category rank of 12 in Colorado Edibles, indicating that mix-driven recovery via cross-category expansion was absent and that the Edible-only concentration amplified the 24-month contraction of 62.10%.

The pattern implies a positioning constrained by price-led tactics rather than portfolio breadth: a 2.09% average price decline against a 13.38% month-over-month sales drop suggests limited elasticity in June 2026, while a 100.0% Edible mix left no buffer to offset a 19.35% year-over-year fall. With a rank of 12 in Colorado Edibles and no share from other categories, Hedy’s current stance relies on improving Edible velocity or segment targeting within Edibles rather than diversification, as price changes alone did not counter the slope implied by the double-digit month-over-month decline.

Competitive Landscape

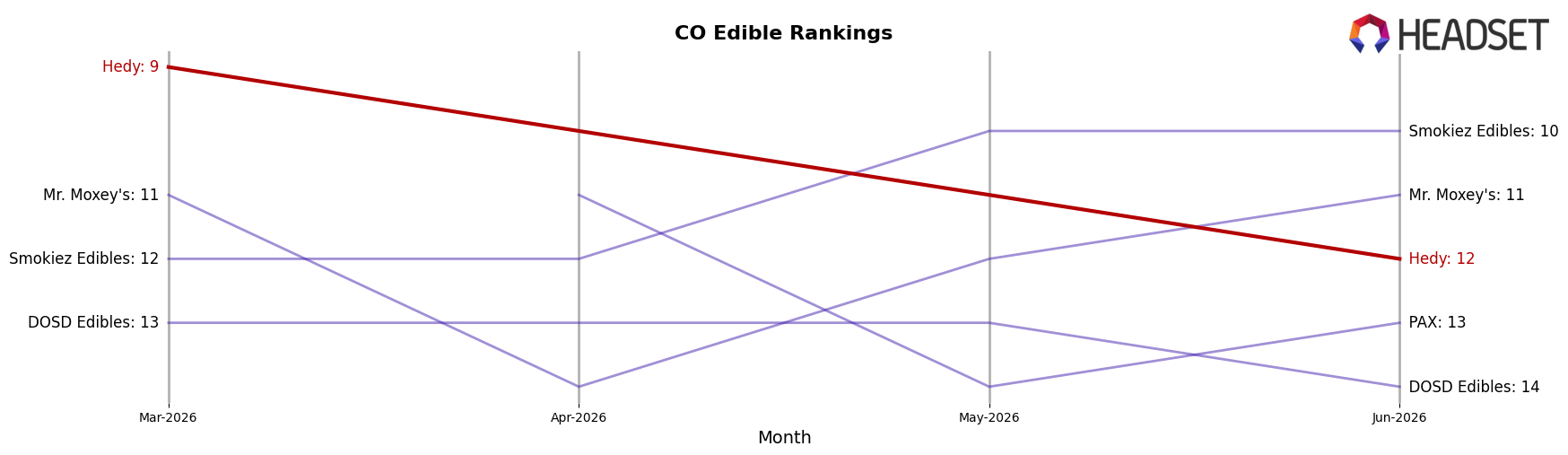

Hedy sits at rank #12 in Colorado Edible in June 2026, down 2 positions from #10 a year ago, and 3 spots below its March 2026 peak at #9; meanwhile, category leader Wyld held #1 year over year but saw sales decline 16.6%, and Good Tide stayed at #5 while contracting 25.5%, signaling that Hedy’s rank slippage contrasts with top-tier softness it could have exploited. Compared with Wana steady at #2 with a 0.5% sales dip and Dialed In Gummies stable at #3 with 3.7% growth, Hedy’s move from #9 in March 2026 to #12 in June 2026 indicates momentum loss during a period when incumbents were either flat or contracting, implying the brand’s trajectory points to missed share-capture opportunities rather than category-driven pressure.

Notable Products

Inspired Root Beer Float Soft Lozenges 10-Pack (100mg) posted the steepest decline in June 2026 at -11.1% while dropping to rank 8, contrasting with Sour Watermelon Gummies 10-Pack (100mg) up 25.2% at rank 1. Cherry Limeade Gummies 10-Pack (100mg) grew 14.7% at rank 2, whereas Fruity Crunch Cereal Treat (100mg) slipped -6.2% at rank 4, indicating share is consolidating toward fruit gummy formats. With four of the top ten as gummies clustered at ranks 1–3 and 6, plus a new Neapolitan Cereal Treat (100mg) debuting at rank 7, Hedy’s mix is tilting toward higher-velocity gummies over lozenges, with cereal treats holding mid-pack. This pattern implies Hedy is concentrating commercial energy on mainstream fruit gummies as the primary growth engine, using cereal treats as secondary support while de-prioritizing novelty lozenges despite $12,333 in June 2026 sales for the declining SKU.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.