Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

In June 2026, Verano’s mix skewed to Pre-Roll at 43.90% share despite a year-over-year decline of 65.85% and a month-over-month drop of 10.16%, while Flower held 33.30% share with a steeper 69.96% YoY contraction and a 31.32% MoM decline. Vapor Pens compressed to 13.47% share with an 85.69% YoY fall and a 37.25% MoM slide, and Concentrates at 6.33% share fell 74.45% YoY and 16.85% MoM; Edible remained small at 2.99% share but was the only category with positive MoM at 5.44% despite a 77.18% YoY decline. The pattern implies reliance on value-forward inhalables where price elasticity is evident, as seen in the brand’s average price easing 2.70% YoY to $29.13 alongside mix migration toward lower-priced Pre-Roll and away from higher-ticket Flower and Vapor Pens.

The sharper MoM declines in Flower (down 31.32%) and Vapor Pens (down 37.25%) versus Pre-Roll (down 10.16%) indicate a retreat from premium and hardware-dependent formats, concentrating Verano’s demand in faster-turn, mid-price items; this shift aligns with a 73.08% brand-level YoY sales contraction and a 29th rank in Flower in New Jersey. With Edible growing 5.44% MoM off a 2.99% share base while Vapor Pens and Concentrates continue double-digit MoM erosion, the implication is that short-term stabilization may come from leaning into Pre-Roll scale and testing Edible expansion, while Flower’s declining rank position within New Jersey suggests diminished shelf power that necessitates re-segmentation rather than discount-only tactics.

Competitive Landscape

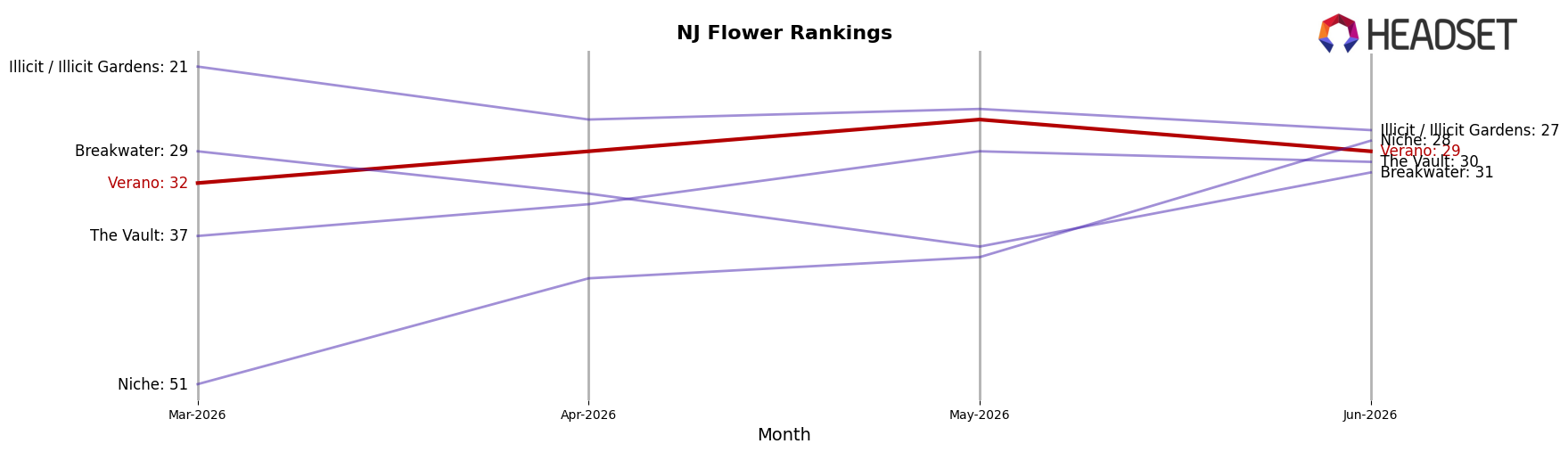

Verano ranks #29 in New Jersey Flower in June 2026, down 16 positions year over year from #13, and only slightly up versus March 2026 when it sat at #32; against its historical peak of #8 in April 2025, the current #29 marks a 21-place slide, while the three-month shift from #32 to #29 is a 3-rank improvement. In contrast, Find. climbed from #12 to #1 year over year and Ozone moved from #2 to #2 with a flat rank but negative 10.6% sales change, indicating the competitive set is advancing or consolidating at the top while Verano ceded share; this trajectory implies Verano is stabilizing quarter-over-quarter but remains on a multi-quarter downtrend that requires either mix or pricing resets to re-enter the top 20.

Notable Products

Blue Magic Gummies (100mg) plunged 89.2% month over month to rank 1, while Fresh Powder #9 (7g) fell 31.1% at rank 9, signaling a sudden contraction at both the top and within Flower. Guava Casquitos Pre-Roll (1g) declined 34.5% at rank 6, and Pre-Rolls occupy four of the top ten ranks, concentrating mix away from Edibles and Vapor Pens even as Essence Travelers - Strawberry Cough BDT Distillate Oil Disposable (0.3g) slid 2.9% at rank 3. With only one major raw dollar anchor at $41,850 for Fresh Powder #9 (7g) and multiple negative MoM shifts exceeding 30%, the portfolio is tilting toward multi-pack Pre-Rolls for volume while legacy Edible and select Flower SKUs retrench, implying a pivot toward repeatable, value-forward formats over novelty-led offerings.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.