Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

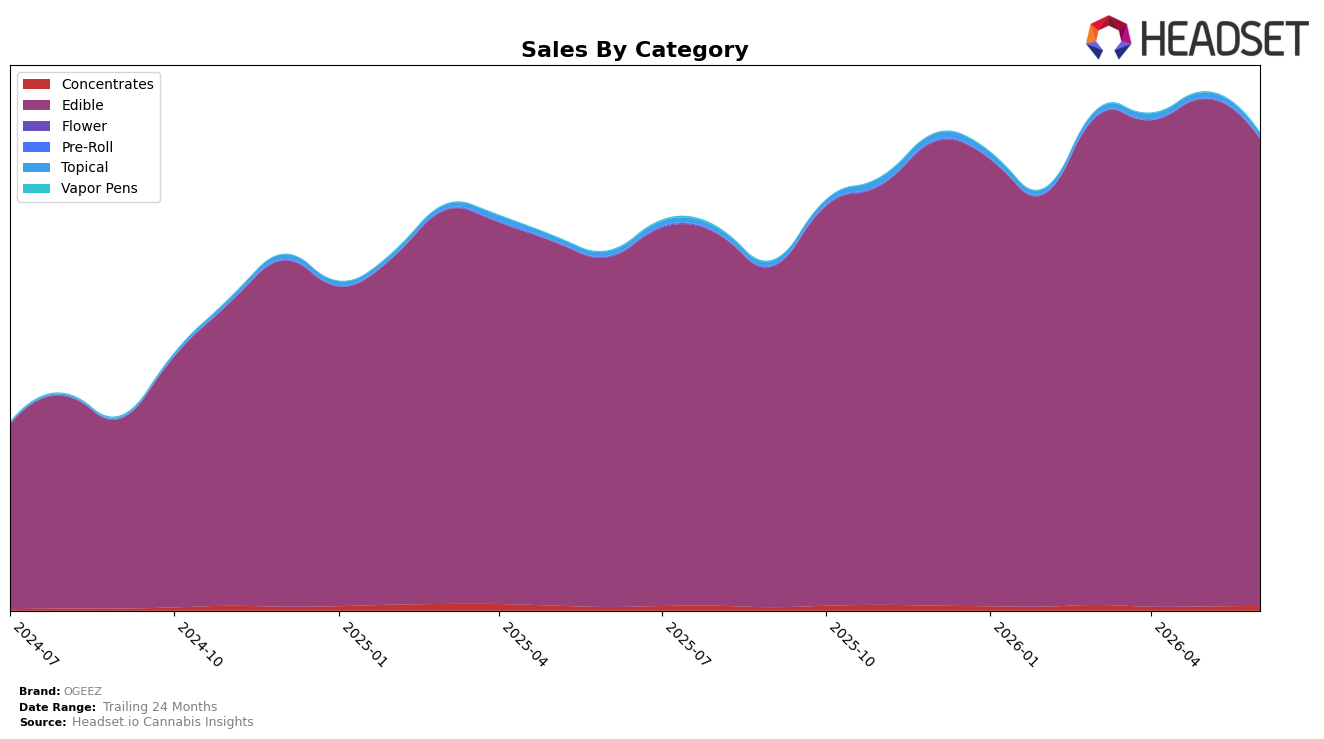

OGEEZ concentrated 97.95% of June 2026 sales in Edible, where year-over-year growth was 33.50% but month-over-month declined 8.01%, while the brand’s overall sales grew 33.06% YoY alongside a 12.95% YoY drop in average price; this mix indicates volume-led gains despite pricing pressure. Secondary categories were small but volatile: Concentrates held 0.93% share with +31.46% YoY and +12.95% MoM, Topical accounted for 0.88% with +4.01% YoY but −13.05% MoM, and Vapor Pens, at 0.15% share, jumped +16.55% YoY and +31.79% MoM; the thesis is that OGEEZ remains an Edible-led brand with tactical experimentation in fringe categories that add incremental growth without reshaping the core.

Positioning implications point to depth over breadth: holding the number 2 rank in Edible in Arizona while Edible mix sits at 97.95% suggests defensible specialization even as MoM softness of −8.01% in Edible contrasts with double-digit MoM gains in Vapor Pens (+31.79%) and Concentrates (+12.95%). With Topical contracting −13.05% MoM and Flower down −32.54% YoY at just 0.05% share, the portfolio tilt implies OGEEZ should protect Edible price architecture amid a −12.95% brand-wide YoY price decline while selectively scaling the two fastest MoM growers as hedge channels rather than near-term share drivers.

Competitive Landscape

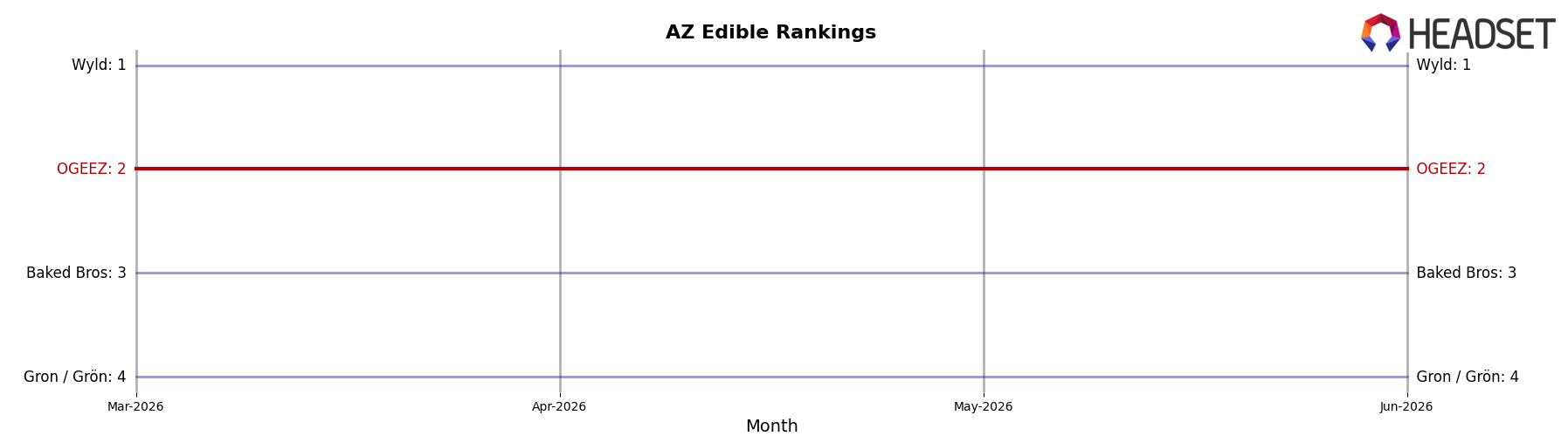

OGEEZ ranks #2 in AZ Edible in June 2026, unchanged from #2 year over year, while its 3-month position also held at #2 and its peak rank of #2 occurred in June 2026; in contrast, Wyld stayed at #1 year over year despite a -15.3% sales change, and Baked Bros improved from #4 to #3 with +30.9% YoY sales, indicating OGEEZ’s static #2 spot faces upward pressure from a rising #3 and limited headroom beneath a declining #1.

Notable Products

Sleep - THC/CBN 2:1 Indica Aqua Berry Gummy (100mg THC, 50mg CBN) led June 2026 declines at -15.2% MoM while holding rank 1, and Big Happy - CBD/THC 1:1 Strawberries & Cream Gummies 10-Pack (100mg CBD, 100mg THC) fell -17.6% at rank 4. The Fruits - Indica Mellow Gummies 10-Pack (100mg) dropped -18.7% at rank 5, whereas The Creams - Sativa Sunny Gummies 10-Pack (100mg) inched up +4.4% at rank 9. With eight of the top ten as Edible gummies and only one SKU posting a positive mid-single-digit gain, the pattern implies OGEEZ is leaning on a concentrated gummy portfolio that is cyclically sensitive and may need pricing or feature refreshes to stabilize flagship reliance.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.