Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

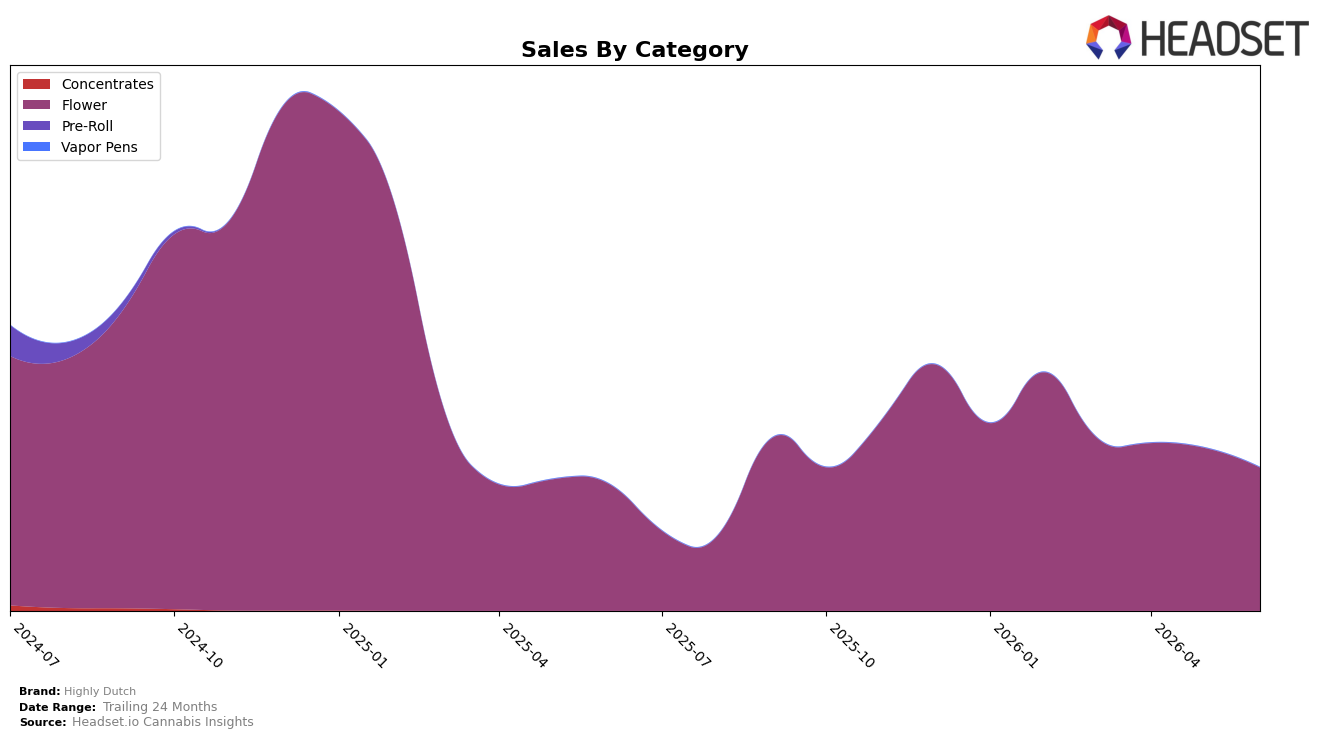

In June 2026, Highly Dutch operated as a single-category brand with Flower at 100.0% of sales share, posting year-over-year growth of 12.6% but a month-over-month decline of 12.1%. Average price rose 1.7% YoY to $119.25 while the category’s sole-focus mix left no offset from other formats, amplifying the MoM pullback despite positive annual momentum. The concentration, paired with a rank of 24 in Flower within British Columbia and a 12.6% YoY lift, implies reliance on a narrow demand base that can swing monthly and limits cross-category insulation.

The 100.0% Flower dependence alongside a 12.1% MoM dip and a 1.7% YoY price increase indicates positioning as a mid-pack Flower specialist rather than a diversified portfolio player. With overall brand sales up 12.6% YoY but down 59.5% over 24 months, the rank at 24 and single-category exposure suggest share is earned through niche depth rather than breadth, implying stability hinges on smoothing intra-Flower volatility rather than expanding into adjacent categories.

Competitive Landscape

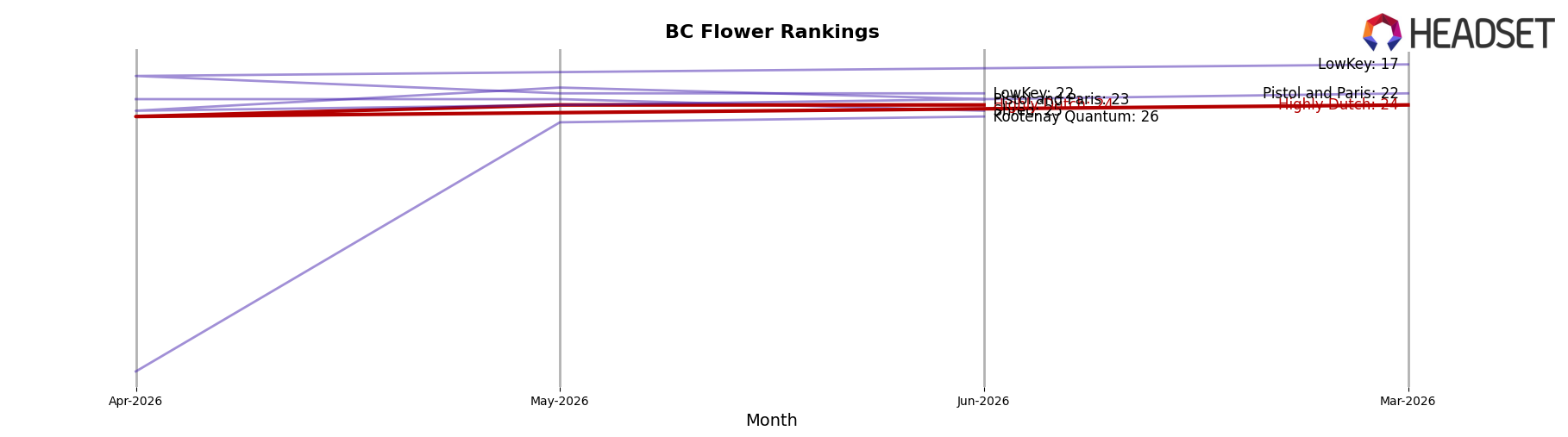

Highly Dutch sits at rank #24 in BC Flower for June 2026, slipping 1 position year over year from #23, while holding flat versus March 2026 at #24; against this, Good Supply climbed from #6 to #1 with 78.1% YoY sales growth and Spinach moved from #8 to #3 with 84.9% YoY growth, indicating that leaders are accelerating as Highly Dutch trails. The brand’s peak of #16 in December 2024 is 8 ranks above today and the top-5 remained stable with Big Bag O' Buds steady at #2 and Bake Sale easing from #3 to #5 alongside an 8.2% YoY sales decline, suggesting that Highly Dutch’s flat three-month rank and slight YoY slippage imply share erosion amid faster-moving rivals and a need to counter sustained gains at the top.

Notable Products

Amsterdam Cherry Mints (28g) posted the steepest decline at -35.9% while falling to rank 6, and Rotterdam (15g) sank -46.1% at rank 7; together with Organic Cherry Mints (28g) at -21.8% and rank 3, this concentration of double-digit drops across Flower signals demand compression within legacy lines. In contrast, Red Pop Runtz (28g) jumped +55.4% to rank 2 and generated $88,254, narrowing the gap to Amsterdam Sativa (28g) which slid -16.0% at rank 1. The mix implies Highly Dutch is rotating toward fewer, faster-moving Flower SKUs anchored by a breakout like Red Pop Runtz (28g) while deprioritizing depth in underperforming formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.