Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

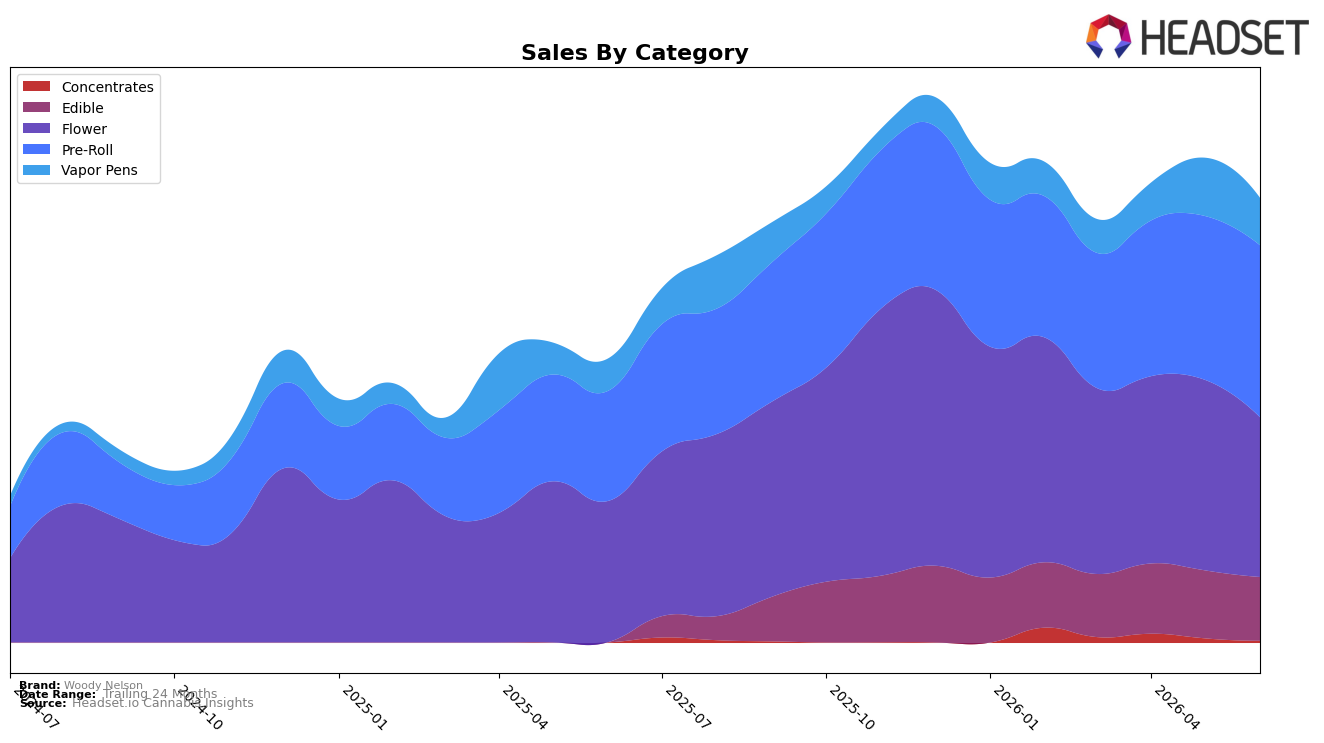

In June 2026, Woody Nelson’s mix tilted toward Pre-Roll at 38.68% share with year-over-year growth of 56.28% and month-over-month growth of 4.97%, while Flower held 35.94% share but fell 16.16% month-over-month despite a 13.16% year-over-year increase. Edible accounted for 14.31% share with a 6.25% month-over-month decline, and Vapor Pens at 10.64% share dropped 18.57% month-over-month even as they grew 46.86% year-over-year; Concentrates remained small at 0.44% share with 524.28% year-over-year growth but a 55.75% month-over-month pullback. With average price down 17.98% year-over-year to $28.02 and Pre-Roll ranked 34th in Ontario, the pattern implies a deliberate pivot toward volume-led categories where price elasticity is favorable, using Pre-Roll momentum to offset Flower and Vapor Pens volatility.

The combination of rising Pre-Roll share (+4.97% month-over-month growth alongside 56.28% year-over-year) and contracting Flower and Vapor Pens month-over-month (-16.16% and -18.57%, respectively) implies that Woody Nelson is prioritizing accessible formats and price points to expand reach, even if that tempers premium mix in the short term. The outsized year-over-year surge in Concentrates (524.28%) paired with a steep 55.75% month-over-month decline suggests opportunistic experimentation rather than sustained scale, while Edible’s 6.25% month-over-month dip indicates limited near-term lift from ingestibles. Together with a 17.98% year-over-year price decrease and a 34th-place Pre-Roll ranking in Ontario, the shifts imply a value-forward positioning anchored in Pre-Rolls to drive traffic, with selective bets in higher-ticket segments that will need stabilization to upgrade the brand’s overall rank.

Competitive Landscape

Woody Nelson ranks #34 in ON Pre-Roll in June 2026, improving 12 positions from #46 year over year, while remaining flat versus March 2026 at #34; despite a peak of #31 in February 2026, the brand has not converted that brief rise into a sustained climb. In the same window, Back Forty / Back 40 Cannabis advanced from #3 to #1 with 74.6% year-over-year sales growth, and Jeeter slid from #2 to #4 alongside a 48.5% sales decline, indicating share is rotating toward value and away from premium-positioned entrants; this split, combined with Woody Nelson’s 12-rank YoY gain but 3-rank gap from its February 2026 peak, implies the brand’s trajectory is incremental rather than breakout unless it captures momentum from incumbents shifting down the leaderboard.

Notable Products

Flight 525 Pre-Roll 5-Pack (2.5g) posted the single largest movement in June 2026 with a +56.0% month-over-month surge, jumping into rank 5 while Rainbow Driver Pre-Roll 5-Pack (2.5g) slid -14.6% to rank 3. Rocketeer Infused Pre-Roll (1g) inched up +6.2% while holding rank 1, and Country Club Infused Pre-Roll (1g) fell -11.4% at rank 10. With seven of the top ten SKUs in Pre-Roll formats, the mix signals a pivot toward multi-pack and infused Pre-Rolls as the commercial engine, concentrating share in formats that can scale velocity even when legacy Pre-Roll SKUs contract.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.