Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

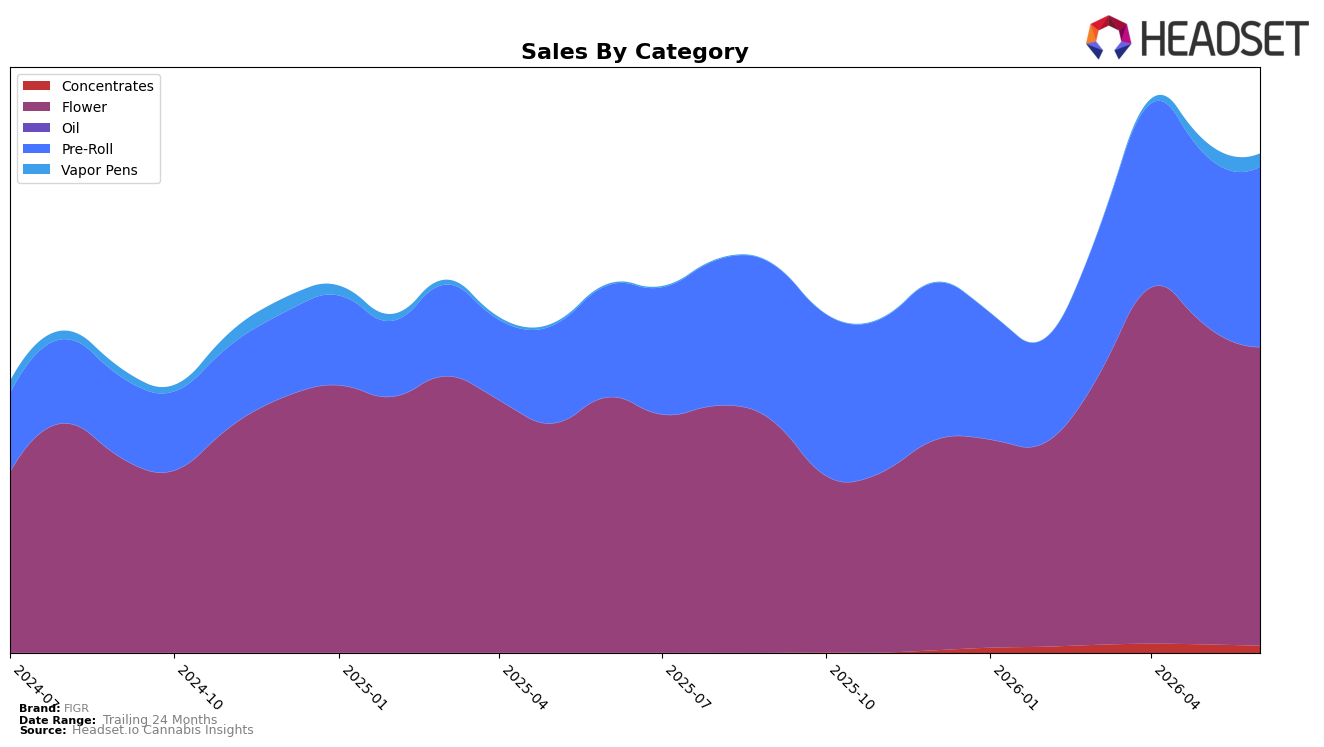

FIGR’s category mix in June 2026 tilted toward Flower at 59.85% share, but with a month-over-month decline of 6.58% even as year-over-year rose 16.92%; in contrast, Pre-Roll expanded to 36.09% share with a 5.71% MoM gain and a 61.04% YoY increase. Vapor Pens remained a small slice at 2.63% share, pairing a 0.10% MoM dip with a 1,039.26% YoY jump, while Concentrates slipped to 1.42% share on a 16.01% MoM decline and no reported YoY baseline. This mix implies FIGR is broadening beyond Flower toward Pre-Roll without abandoning its core, while testing Vapor Pens as an incremental growth vector rather than a scale bet.

With overall brand sales up 35.44% year over year against a 2.28% YoY decrease in average price, unit-led growth is outpacing any price pressure, and the 5.71% MoM lift in Pre-Roll alongside a 6.58% MoM pullback in Flower signals share rotation rather than category contraction. Holding the top provincial momentum in ON and an eighth-place Flower rank in Alberta positions FIGR to leverage Pre-Roll gains while defending Flower, implying a portfolio strategy that trades some Flower velocity for expanding baskets via value-priced Pre-Rolls and niche experimentation in Vapor Pens.

Competitive Landscape

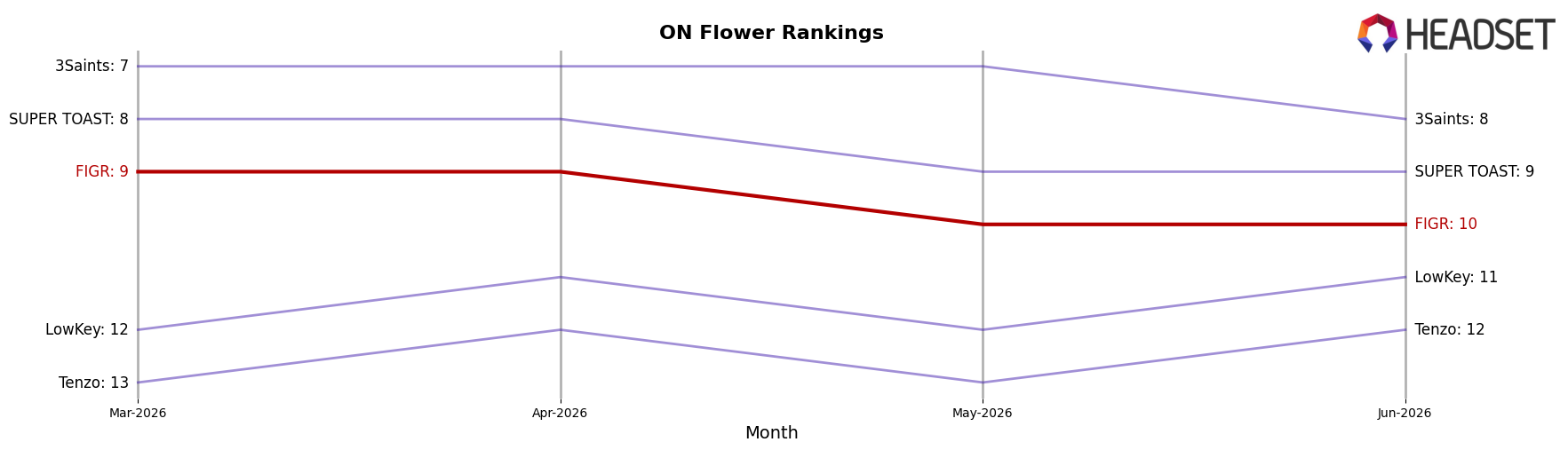

FIGR holds rank #10 in Ontario Flower in June 2026, up 6 positions year over year from #16, but down 1 spot from March 2026’s #9 and off its April 2026 peak at #9; by contrast, Spinach climbed from #4 to #1 while growing sales 38.3% YoY, and Back Forty / Back 40 Cannabis slipped from #1 to #4 as sales fell 11.3% YoY, indicating FIGR’s mid-pack rise comes amid both accelerating leaders and retreating incumbents, implying its rank trajectory points to opportunistic share capture if it converts April 2026’s peak positioning into sustained top-10 stability.

Notable Products

Mellow Man Pre-Roll 10-Pack (3.5g) posted the steepest decline at -8.6% month over month while sliding to rank 3 in June 2026, whereas Jungle Fumes Pre-Roll 10-Pack (3.5g) held rank 1 with a -3.2% dip and Chatty Kathy Pre-Roll 10-Pack (3.5g) rose 8.3% at rank 2. Kandy Cake Pre-Roll 10-Pack (3.5g) surged 41.8% to rank 4, and four of the top ten are Pre-Roll SKUs concentrated in multi-pack formats, indicating promotional or repeat-purchase pull within this format rather than broad category expansion. In Flower, Jungle Fumes (14g) grew 5.5% at rank 6 while Mellow Man (7g) fell -8.7% at rank 8 and Mellow Man (14g) was flat at +0.6% at rank 10, implying that value ounces are steady but mid-size formats face pressure. The pattern implies FIGR is consolidating around a Pre-Roll-led basket with flagship stability at the top and selective format elasticity in large-format Flower guiding near-term assortment and pricing moves.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.