Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Howl's is stocked at 31 licensed dispensaries across Massachusetts and Rhode Island, 28 of them in Massachusetts, with the deepest coverage in Ayer, Easthampton, Fairhaven, Fall River, and Middleborough. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

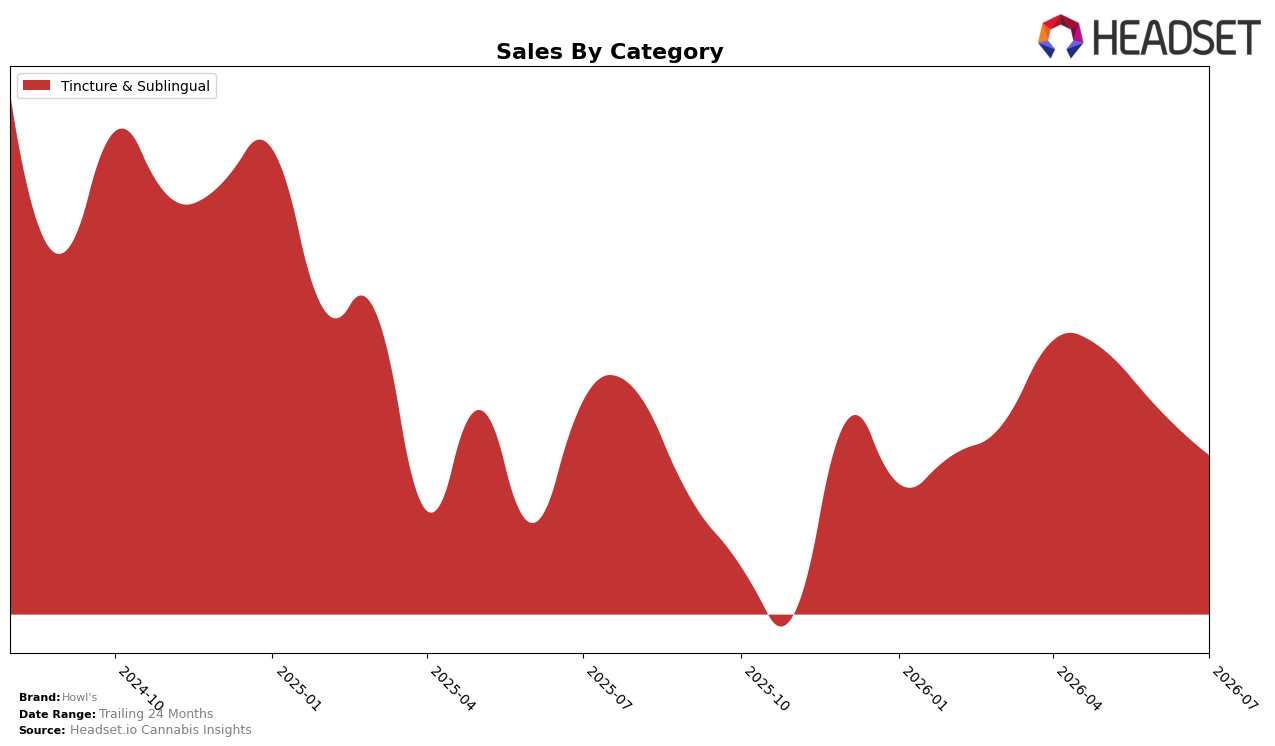

In July 2026, Howl's operated as a single-category brand with Tincture & Sublingual at 100.0% category share, posting a -11.67% year-over-year sales change and a -10.39% month-over-month decline, while average price rose 4.21% year over year to $72.22. Within Massachusetts Tincture & Sublingual, Howl's sat at rank 5, and the combination of a 100.0% mix concentration with a double-digit MoM contraction implies a footprint that is fully exposed to category cyclicality rather than buffered by cross-category offsets.

The -11.67% year-over-year contraction alongside a 4.21% price lift, together with a -10.39% month-over-month pullback, suggests elasticity pressure outweighing any unit mix upgrades, and rank 5 in Massachusetts signals middle-tier visibility rather than category leadership in Tincture & Sublingual. With 100.0% of sales tied to Tincture & Sublingual and a 24‑month decline of -60.69%, the positioning skews toward a narrow, premium-leaning lane where sustaining share will require either deeper differentiation within tinctures or diversification to reduce sensitivity to further single-category volume swings.

Competitive Landscape

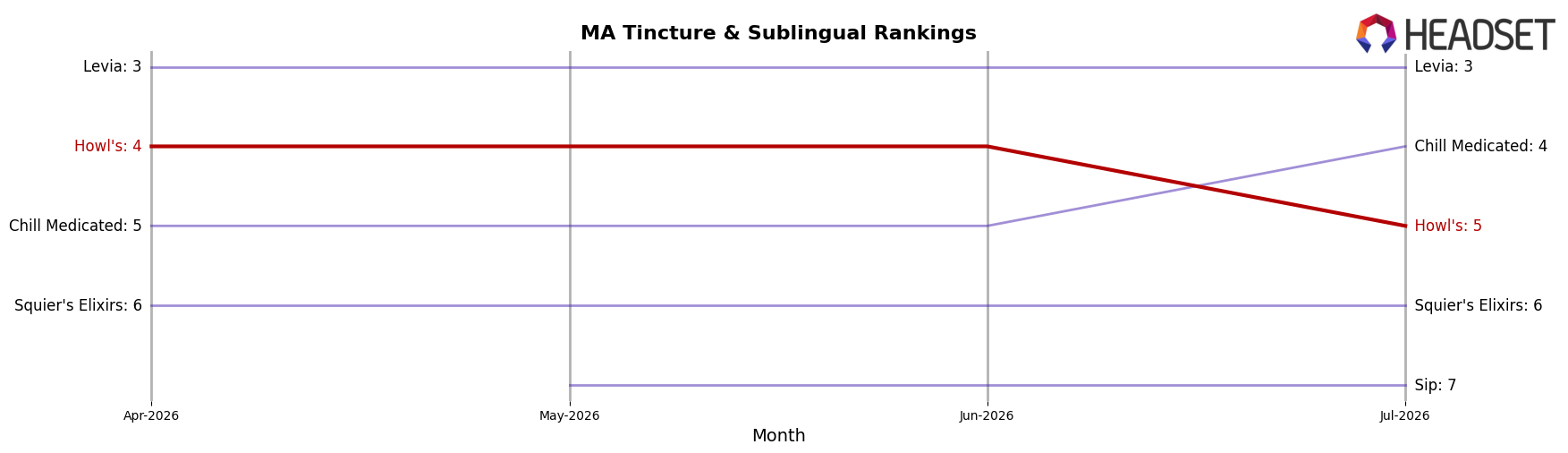

Howl's sits at rank #5 in Massachusetts Tincture & Sublingual for July 2026, slipping 1 position year over year from #4, and down 1 rank from its peak at #4 in June 2026, while category leader Good Feels Inc held #1 with a -5.1% year-over-year sales change and Levia stayed #3 alongside a 130.6% year-over-year increase; additionally, Chill Medicated climbed from #8 to #4 with a 368.3% year-over-year surge, and Treeworks maintained #2 with a 23.0% year-over-year gain. The juxtaposition of Howl's 1-rank YoY decline against competitors’ double- and triple-digit growth implies share is consolidating upward and that holding or regaining #4 will require countering faster comp momentum.

Notable Products

CBD/THC 10:1 High CBD Max Tincture (500mg CBD, 50mg THC,10ml) delivered the largest month-over-month surge at +343.5% and entered July 2026 at rank 3, while Nighttime 2x Double Strength Tincture (500mg THC, 10ml) climbed +151.9% to rank 1 with $8,346 in sales. In contrast, Daytime Max Tincture (500mg) fell -60.4% to rank 4 and Anytime Max Temple Kush Tincture (500mg) dropped -51.1% to rank 2, indicating a rotation away from standard daytime formats toward high-CBD and higher-potency nighttime offerings. With six of the top ten coming from the Tincture & Sublingual category, the mix points to Howl's consolidating around tinctures that address distinct use-cases, signaling a pivot toward polarized demand at the extremes of potency and CBD ratio.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.