Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Sip is stocked at 133 licensed dispensaries across Arizona and Massachusetts, 100 of them in Arizona, with the deepest coverage in Phoenix, Mesa, Tucson, Tempe, and Chandler. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

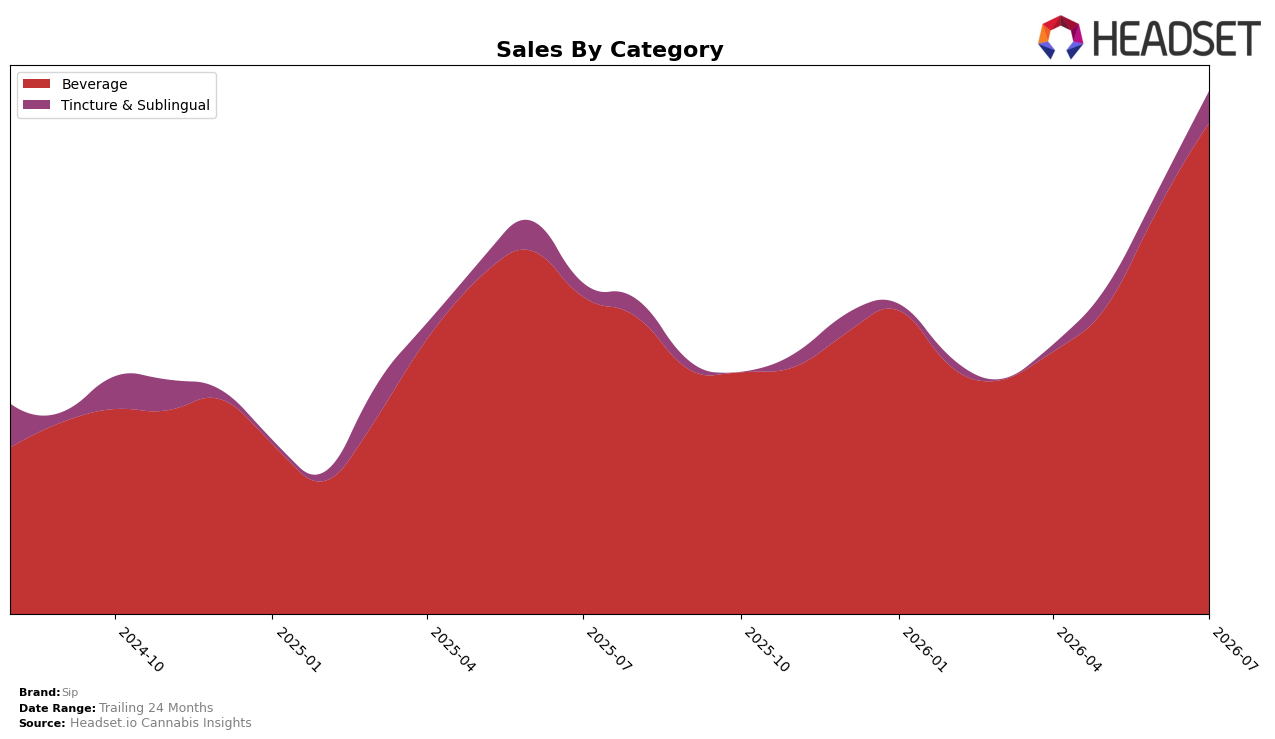

Beverage expanded to 86.45% share in July 2026, up 18.99% month over month and 46.81% year over year, while Tincture & Sublingual held 13.55% share with 17.86% MoM and 26.73% YoY growth; combined, these shifts contributed to Sip’s 43.72% YoY brand sales lift and a 7.28% YoY decline in average price to $4.11. With Beverage priced at $3.65 versus Tincture & Sublingual at $21.35, the mix is tilting toward lower-ticket velocity, and the brand’s Beverage rank at 7 in Massachusetts suggests further share gains are more sensitive to volume than premiumization; the implied pattern is that Sip is trading price for scale within Beverage while maintaining a smaller, higher-priced Tincture & Sublingual niche.

The simultaneous 18.99% MoM growth in Beverage and 17.86% MoM growth in Tincture & Sublingual indicates that July 2026 momentum was broad-based, but the 86.45% Beverage weight means positioning hinges on sustaining repeat purchase at the $3.65 price point, not on upselling to $21.35 formats. Given the 46.81% YoY rise in Beverage against a lower brand-wide average price and a rank of 7 in Massachusetts Beverage, the brand is operating as a volume-led mid-pack player whose path to rank improvement likely comes from incremental Beverage distribution and pack-size tactics rather than relying on the 26.73% YoY growth in Tincture & Sublingual, which lacks enough share to shift overall positioning.

Competitive Landscape

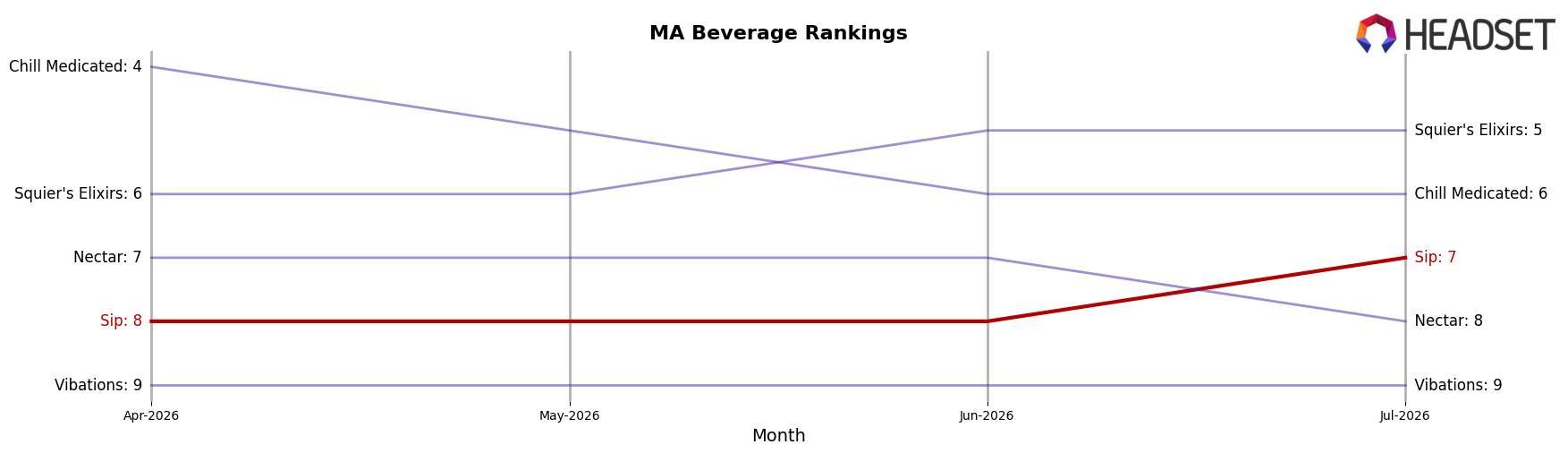

Sip ranks #7 in MA Beverage in July 2026, up 4 positions year over year from #11, and up 1 place versus three months ago when it was #8; this new #7 also marks a peak rank in July 2026, while category leaders moved less on the ladder—Levia held at #1 year over year and Hi5 Seltzer stayed #2—indicating Sip is compressing the gap to the top tier despite stable incumbents and a mid-pack shuffle where Pine + Star improved from #5 to #4 and Squier's Elixirs advanced from #6 to #5; the trajectory implies Sip’s step-up from #11 to #7 within a year positions it for near-term contention for the #5–#6 slots if momentum against static top-two rivals persists.

Notable Products

CBD/THC 1:1 Half & Half Soda (5mg CBD, 5mg THC, 12oz, 355ml) posted the sharpest month-over-month acceleration at 39.1% while rising to rank 5, and Orange Pineapple Seltzer (5mg, 12oz, 355ml) followed with a 33.0% gain at rank 4. Meanwhile, THC/CBG/THC Revive Pink Potion (5mg THC, 1mg CBG, 1mg CBC, 12oz, 355ml) slipped 1.7% at rank 9 even as Rootbeer Soda (5mg, 12oz, 355ml) jumped 29.2% into rank 8. With eight of the top ten in Beverage formats and the top three ranks growing between 6.4% and 10.8%, the mix tilts toward familiar soda and seltzer profiles capturing incremental trial while niche functional blends pause. The pattern implies Sip is consolidating share around classic, low-complexity Beverage SKUs that scale distribution, with functional variants serving as secondary, lower-volatility contributors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.