Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

HY-R is stocked at 216 licensed dispensaries across Michigan, with the deepest coverage in Detroit, New Buffalo, Monroe, Grand Rapids, and Ann Arbor. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

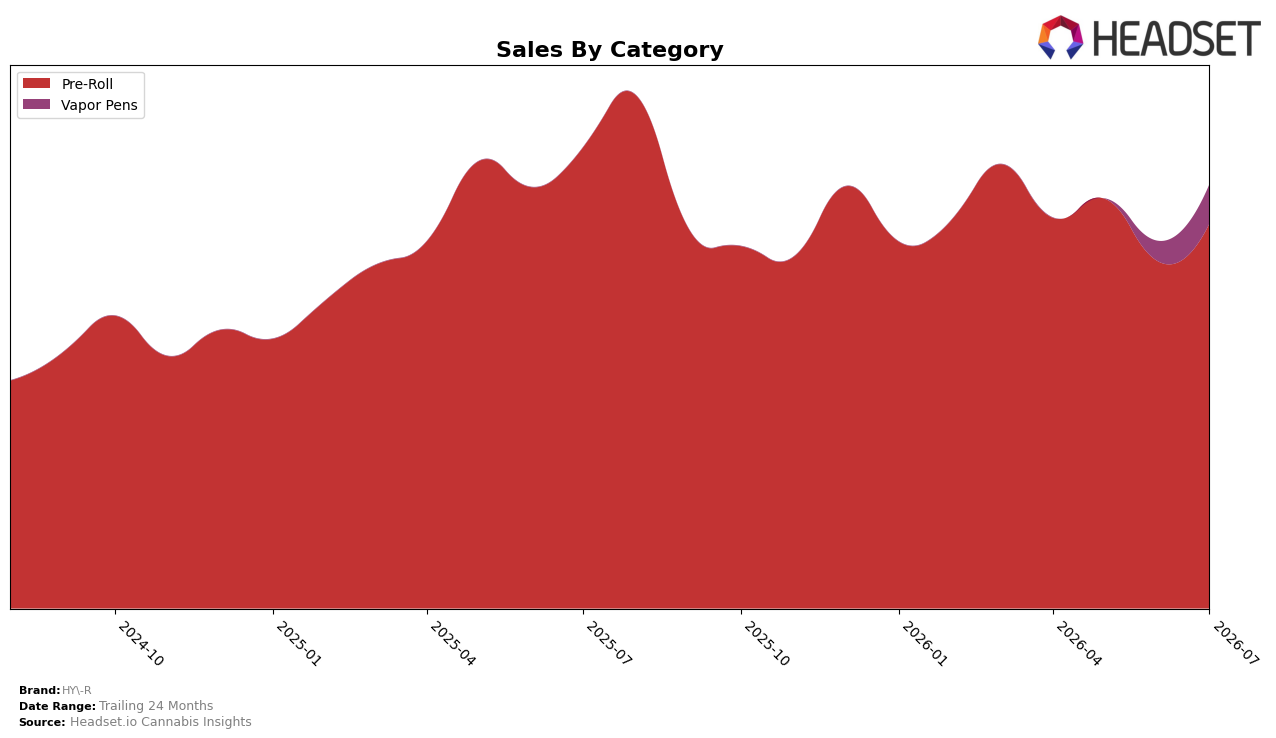

In July 2026, HY-R concentrated 90.79% of sales in Pre-Roll with a 10.88% month-over-month lift even as that category was down 16.57% year over year, while Vapor Pens expanded to 9.21% share on a 94.39% month-over-month jump from a small base and no year-over-year comp available. The brand’s average price rose 24.92% year over year to one disclosed price point, coinciding with a brand-level sales decline of 8.11% year over year, and HY-R held rank 8 in Pre-Roll within Michigan. The pattern implies HY-R is leaning back into Pre-Roll for near-term volume while testing Vapor Pens for incremental reach, with pricing gains partially offsetting the Pre-Roll year-over-year contraction.

The shift toward a modestly broader mix — Pre-Roll at 90.79% and Vapor Pens at 9.21% — combined with a 10.88% Pre-Roll month-over-month increase and a 94.39% Vapor Pens month-over-month surge suggests a positioning pivot from single-category reliance toward a two-lane strategy. With rank 8 in Michigan Pre-Roll and a 16.57% year-over-year decline in that category against a 24.92% higher average price, the brand is trading some Pre-Roll velocity for higher unit economics while using Vapor Pens to recapture lost baskets. The implication is a defensive posture in Pre-Roll paired with opportunistic expansion in Vapor Pens to stabilize revenue after an 8.11% brand-level year-over-year dip.

Competitive Landscape

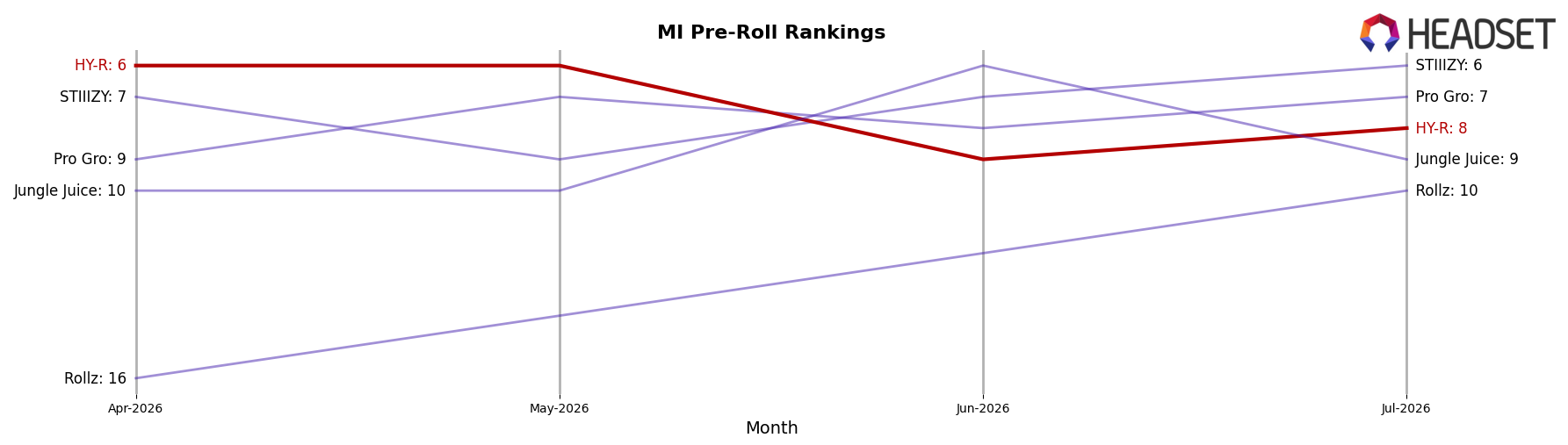

HY-R ranks #8 in MI Pre-Roll in July 2026, down 2 spots year over year from #6, after peaking at #6 in May 2026 and slipping from #6 three months ago to #8 now; this contrasts with Mitten Extracts moving up from #7 to #4 alongside a 68.5% YoY sales gain and Goodlyfe Farms sliding from #4 to #5 with a 36.4% YoY sales decline, while category leader Jeeter held #1 year over year with a 4.0% YoY sales increase; the pattern—HY-R’s 2-rank YoY drop amid upward mobility from a key mid-tier rival—implies a need to defend share as momentum concentrates above and below its current position.

Notable Products

Blueberry Crumble Liquid Diamonds Infused Pre-Roll (1g) posted the standout move in July 2026 with +84.7% MoM at rank 1 and approximately $149,308 in sales, while Strawberry Shortcake Infused Pre-Roll (1g) fell -13.1% at rank 6. Kiwi Pie Infused Pre-Roll (1g) surged +632.5% MoM into rank 2, and Peach Infused Pre-Roll (1g) declined -24.4% at rank 10. With all top 10 entries in Pre-Roll, the mix indicates HY-R is consolidating around infused pre-rolls, tilting the portfolio toward higher-velocity SKUs that can absorb volatility at the lower ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.