Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

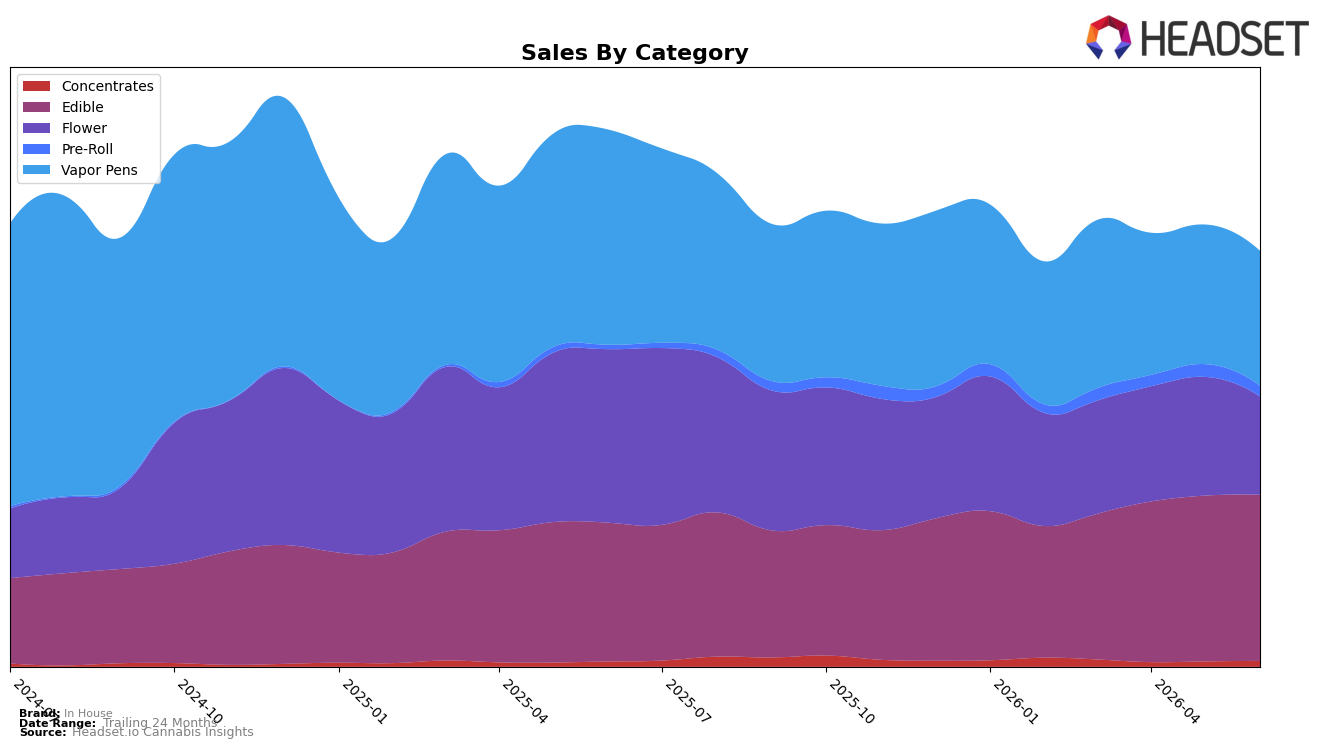

In House tilted toward Edible at 39.8% share in June 2026, with Edible sales up 19.7% year over year and edging 0.2% month over month, while Vapor Pens contracted to 32.4% share on a 37.2% YoY decline and a 3.3% MoM dip. Flower retreated to 23.6% share with a 43.2% YoY drop and a 17.1% MoM fall, contrasted by Pre-Roll’s 2.7% share on 125.9% YoY growth but a 15.6% MoM pullback, and Concentrates at 1.5% share gained 9.7% YoY and 8.6% MoM. Despite brand-wide sales falling 22.5% YoY and average price down 16.1%, Edible momentum plus a #4 rank in Edible in Maryland indicates a pivot toward value-driven edible volume while inhalables lose traction.

The mix shift implies In House is trading into lower-ticket formats as average price sits at $20.95 and Edible average price is $14.87, while Vapor Pens at $31.59 and Flower at $30.96 face elasticity that aligns with their 37.2% and 43.2% YoY declines. The concurrent 8.6% MoM lift in Concentrates alongside a 17.1% MoM drop in Flower points to substitution toward smaller, potency-forward baskets, and the 0.2% MoM uptick in Edible against a 3.3% MoM dip in Vapor Pens suggests basket stabilization around non-inhalable convenience; together these shifts position the brand closer to value-led, edible-centric share defense rather than premium inhalable leadership.

Competitive Landscape

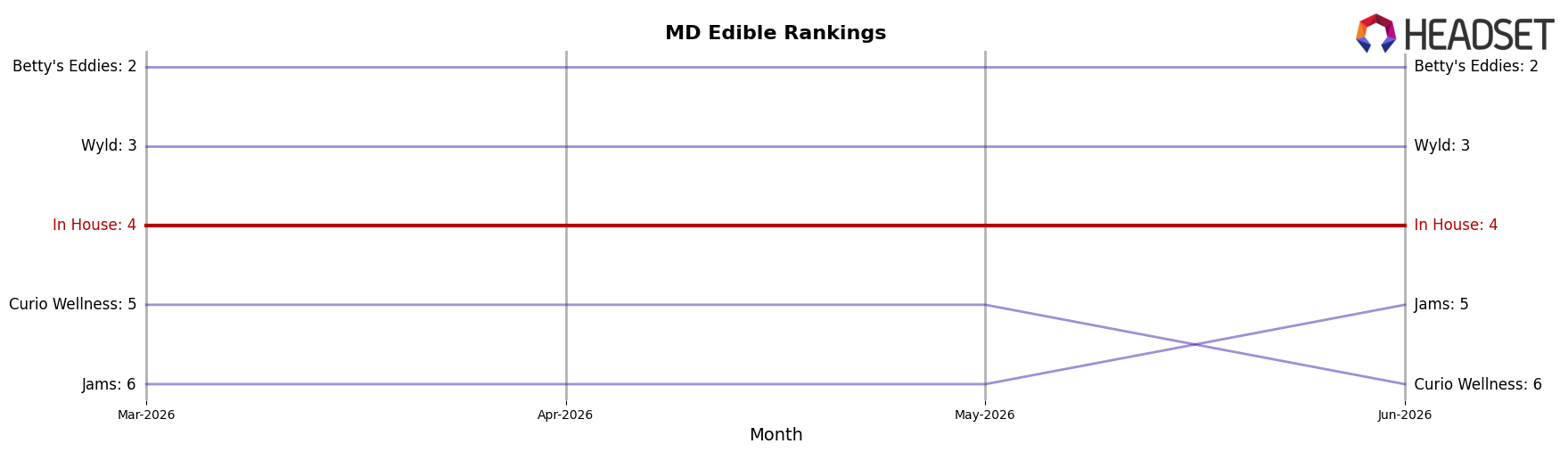

In House is currently ranked #4 in MD Edible, improving 2 positions from #6 year over year, and matching its peak at #4 in June 2026 while holding steady from March 2026 at #4; meanwhile, Incredibles climbed from #3 to #1 with a 49.4% YoY sales increase, and Betty's Eddies slipped from #1 to #2 as sales fell 10.8% YoY, with Wyld easing from #2 to #3 on a 6.0% YoY decline; against this backdrop, In House’s unchanged rank from March 2026 to June 2026 and 2-rank YoY gain imply the brand is consolidating a top-5 position as leadership churns above it.

Notable Products

The steepest move in June 2026 was the decline for Cherry Lemonade Fast Acting Gummies 20-Pack (100mg), down 15.6% MoM at rank 7, while Watermelon Fast Acting Gummies 10-Pack (100mg) slipped 10.1% MoM at rank 6, signaling pressure on larger-count and certain fruit SKUs. At the top, CBD/THC 5:1 Blood Orange Gummies 10-Pack (500mg CBD, 100mg THC) grew 8.3% MoM to hold rank 1, and CBD/THC/CBN 3:2:1 Blueberry Dreams Nano Gummies 10-Pack (150mg CBD, 100mg THC, 50mg CBN) rose 9.7% MoM at rank 5, suggesting cannabinoid-balanced and sleep-adjacent formats are gaining share. Eight of the top ten are Edible gummies, and the 10-Pack format dominates the top five, implying unit-size convenience is concentrating demand. The mix points to In House leaning into functional formulations and 10-Pack accessibility to stabilize share while phasing back from slower 20-Pack variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.