May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

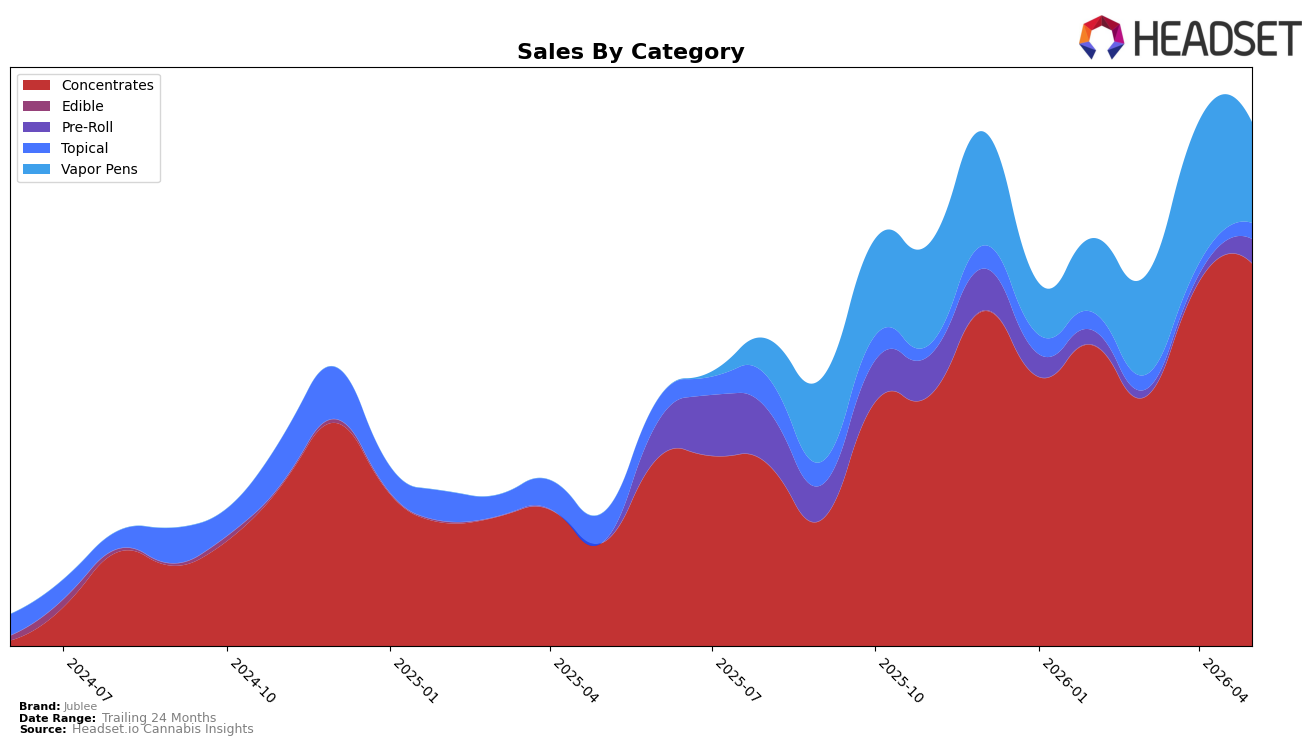

In May 2026, Jublee concentrated its mix even further into Concentrates at 73.19% share, with that category up 269.84% year over year and 5.23% month over month, while Vapor Pens fell to 19.23% share with a 29.31% month-over-month decline. Pre-Roll, though only 4.57% share, spiked 250.42% month over month, and Topical held 3.00% share despite a 45.99% year-over-year drop alongside a 44.89% month-over-month rebound; combined with a 294.49% brand-level year-over-year sales increase and a 9.83% higher average price, the current mix implies price-tolerant growth anchored in Concentrates expansion. The thesis is that Concentrates-driven scale is offsetting volatility in smaller lines, creating headroom to selectively nurture Pre-Roll while managing the Vapor Pens drawdown.

The shift toward a 73.19% Concentrates footprint, alongside a May 2026 rank of 29 in Concentrates in Ontario, positions Jublee as a category specialist rather than a broad-portfolio player, with MoM softness in Vapor Pens (-29.31%) signaling a need to prioritize depth over breadth. The 250.42% MoM surge in Pre-Roll and the 44.89% MoM recovery in Topical suggest tactical upside niches that can lift velocity without diluting the core, while the 5.23% MoM gain in Concentrates underpins stability despite a higher average price and a 294.49% YoY brand sales rise; the implication is a defensible rank based on Concentrates leadership with controlled bets in two adjacent formats.

Competitive Landscape

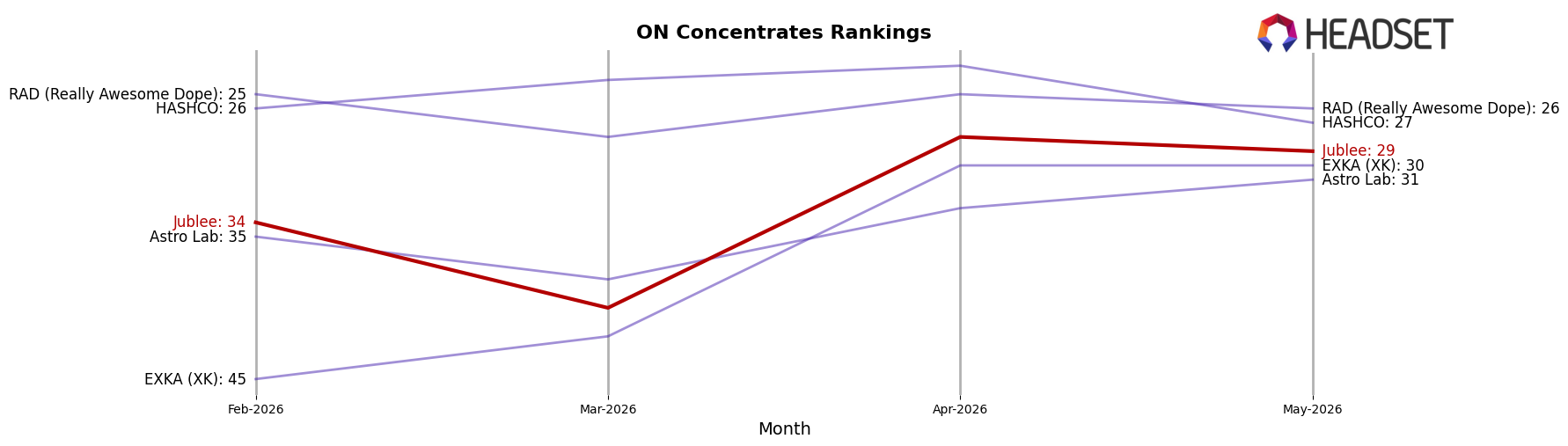

Jublee sits at rank #29 in ON Concentrates for May 2026, improving 21 spots year over year from #50 and edging 5 ranks ahead of its February 2026 position at #34; however, it slipped 1 place from its peak rank of #28 reached in April 2026. In contrast, Vortex Cannabis Inc. held #1 with a 7.9% year-over-year sales increase while Pura Vida advanced from #4 to #2 on 30.8% growth, and Endgame fell from #2 to #5 as sales declined 49.7%, indicating competitors are both consolidating at the top and cycling downward. The pattern—steady climb from #50 to #29 year over year but a month-over-month dip from #28 to #29—implies Jublee is gaining structural ground but still contends with volatile short-term rank pressure from faster-rising and sharply-correcting rivals.

Notable Products

CBG Bright Mind Full Spectrum Kief Infused Pre-Roll 4-Pack (2g) posted the largest movement in May 2026 with a +250.4% month-over-month surge and jumped into rank 5, while Gilded Live Rosin (1g) collapsed by -80.4% to rank 8 and CBG Sweet Citrus Bright Mind Distillate Broad Spectrum Disposable (1.2g) fell -29.3% to rank 3. Concentrates still concentrate the leaderboard with four of the top ten SKUs, led by Montreal Style Aged Hash (2g) at rank 1 with +22.5% MoM and Hybrid Full Spectrum (1g) at rank 2 with +16.1% MoM, even as East Coast Aged Hash (2g) declined -23.5% to rank 4. Topicals provided incremental breadth as CBD Sweet Citrus Extra Strength Body Butter (1000mg CBD) climbed +70.8% to rank 7 and the CBD Flowers & Fir Bath Salts (400mg CBD, 250g) rose +13.8% to rank 9, contributing $1,744 in added stability amid category volatility. The mix implies Jublee is leaning into hash-led Concentrates for volume while testing wellness-oriented Topicals and an opportunistic Pre-Roll hit to diversify exposure away from a weakening premium rosin and a cooling CBG vapor pen.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.