Apr-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

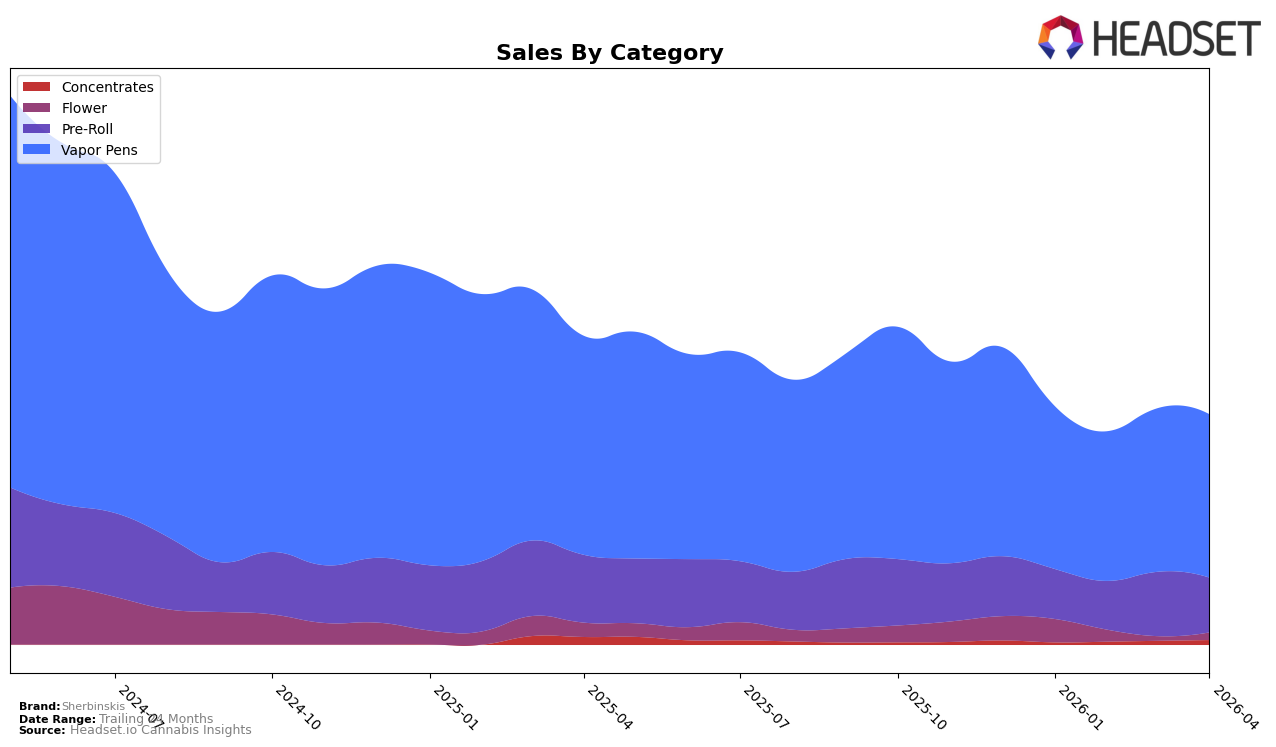

Sherbinskis has shown a varied performance across different states and categories in early 2026. In Ontario, the brand has consistently maintained a position within the top 40 for Vapor Pens, with a slight fluctuation observed in March 2026 when it dropped to 36th place before returning to 33rd in April. This consistency is indicative of stable consumer interest in Sherbinskis' Vapor Pens in this region. Meanwhile, in British Columbia, Sherbinskis did not make it into the top 30 for Vapor Pens, suggesting a more challenging market environment or stronger competition in this category.

In California, Sherbinskis' performance in the Pre-Roll category has been somewhat volatile. The brand improved its ranking from 82nd in February to 69th in March, but then slipped back to 80th in April 2026, hinting at fluctuating consumer preferences or market dynamics. Conversely, their Vapor Pens maintained a relatively stable ranking around the 60th position throughout the first four months of 2026, reflecting a steady demand. The brand's ability to maintain its ranking in California's competitive market for Vapor Pens is noteworthy, although they have yet to break into the top 30 in either category, which could be a strategic focus for Sherbinskis moving forward.

Competitive Landscape

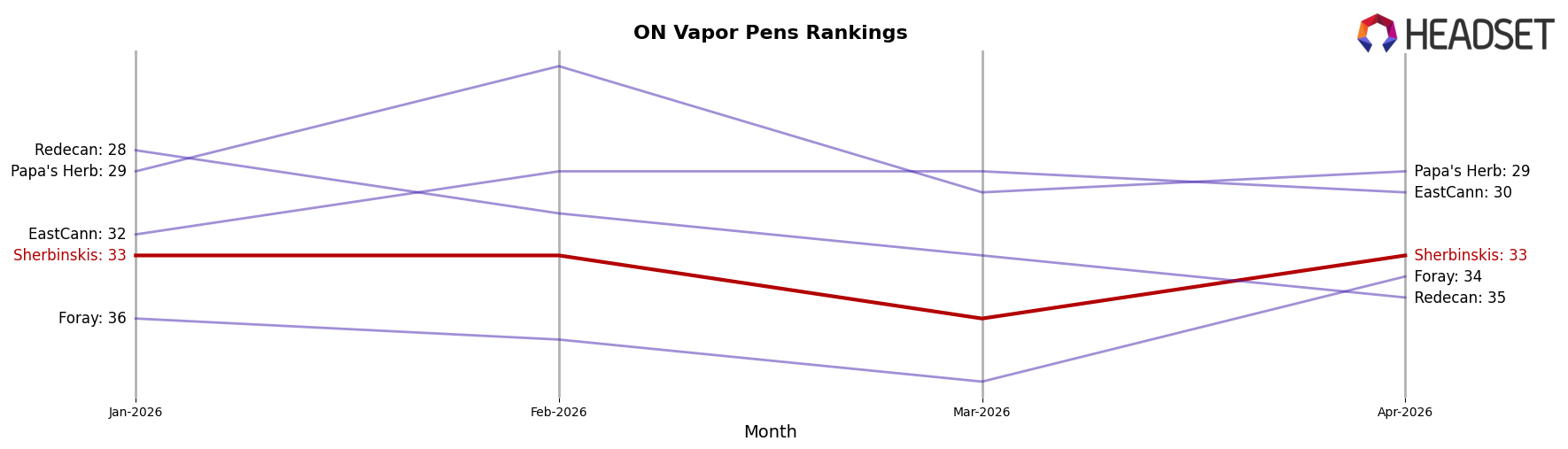

In the competitive landscape of vapor pens in Ontario, Sherbinskis has shown a consistent presence, maintaining a rank of 33 in January, February, and April 2026, with a slight dip to 36 in March. This stability in rank is noteworthy, especially when compared to competitors like Redecan, which experienced a decline from rank 28 in January to 35 in April. Similarly, Papa's Herb fluctuated but generally maintained a stronger position, ranking 29 in January and April. Meanwhile, EastCann showed a more favorable trend, improving from rank 32 in January to 30 in April. Despite these competitive pressures, Sherbinskis' sales have shown an upward trend from January to April, indicating a positive reception in the market despite not breaking into the top 20 ranks. This suggests that while Sherbinskis may not lead in rank, its sales growth could be attributed to brand loyalty or effective marketing strategies.

Notable Products

In April 2026, Sherbinskis' top-performing product was the True Gelato 33 Live Resin Disposable (0.5g) in the Vapor Pens category, maintaining its first-place rank for the fourth consecutive month with impressive sales reaching 3333 units. The True GLTO 33 Live Resin Cartridge (1g) also performed well, securing the second spot, consistent with its February and March rankings. The Pure Live Resin Disposable 2-Pack (1g) ranked third, showing a slight decline from its second position in March. Gelonade Rosin Infused Pre-Roll 5-Pack (2.5g) held steady at fourth place, mirroring its March ranking. Lastly, Mochi x Acai Infused Pre-Roll 2-Pack (1g) re-entered the rankings at fifth place, having been unranked in March.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.