Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

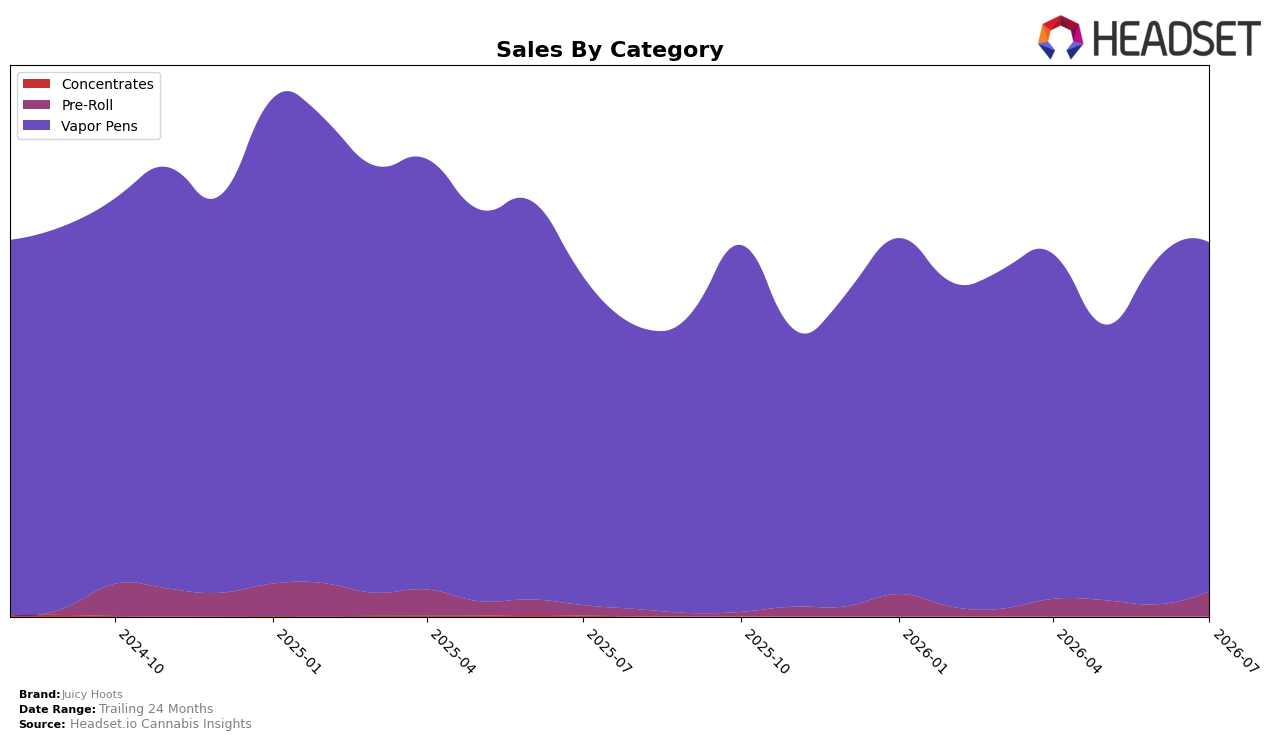

In July 2026, Vapor Pens held 93.38% share for Juicy Hoots while Pre-Roll accounted for 6.62%, with Vapor Pens up 0.74% month over month and 6.11% year over year and Pre-Roll up 111.57% month over month and 146.67% year over year. Overall brand sales grew 10.01% year over year alongside a 12.31% decline in average price to $30.07, indicating mix-led unit expansion as Pre-Roll scaled from a small base; the pattern implies Juicy Hoots is leaning into a two-tier portfolio where rapid Pre-Roll gains begin to diversify a Vapor Pens-centric model without yet displacing the core.

Juicy Hoots ranked 10 in Vapor Pens in Saskatchewan, a position that, combined with 93.38% category concentration and only 6.62% in Pre-Roll, suggests the brand’s market identity is still anchored to Vapor Pens even as Pre-Roll momentum accelerates by 111.57% month over month and 146.67% year over year. With Vapor Pens price at $32.05 versus Pre-Roll at $16.05, the widening low-price segment mix helps defend volume but can dilute revenue per unit, implying the brand’s positioning is shifting toward value-access entry points while preserving rank relevance in Vapor Pens through steady 0.74% month-over-month growth.

Competitive Landscape

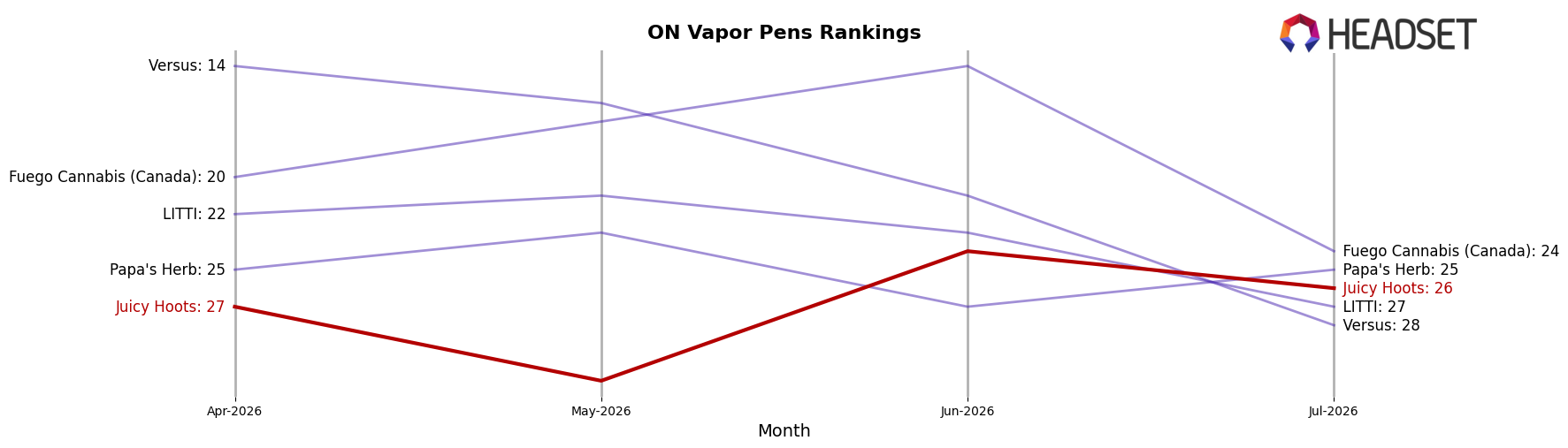

Juicy Hoots is ranked #26 in ON Vapor Pens in July 2026, down 1 position year over year from #25, but 1 position higher than April 2026 when it sat at #27; the brand’s historical ceiling of #16 in November 2024 frames a 10-rank gap to reclaim. Meanwhile, Spinach climbed from #4 to #1 with 144.72% year-over-year sales growth, and General Admission slipped from #3 to #4 alongside a -18.96% sales decline, indicating that upward mobility is available even as peers lose ground; against this backdrop, a 1-rank dip year over year combined with a 1-rank lift versus three months ago implies Juicy Hoots is stabilizing off its November 2024 peak and must convert minor quarter-on-quarter gains into sustained share capture to re-enter the top 20.

Notable Products

Double Berry Flavour Infused Pre-Roll 3-Pack (1.5g) posted the largest month-over-month surge at 188.9% while jumping into rank 6, outpacing the next-fastest riser Double Blue Cherry Distillate Disosable (1g) at 16.1% in rank 1 and eclipsing the 26.0% gain for Double Berry Punch Distillate Disposable (1g) in rank 5. In contrast, Double Blue Cherry Distillate Cartridge (1g) fell 26.2% to rank 3 as Double Grape Giggles Distillate Cartridge (1g) slid 32.4% to rank 8, creating a split where legacy cartridges contracted as infused and disposable formats expanded. With three Pre-Roll SKUs now in the top ten and two of them up triple- and double-digits, versus two cartridge SKUs declining more than 25%, the product mix implies Juicy Hoots is rotating demand from traditional cartridges into higher-impact infused Pre-Rolls and select Disposables in July 2026.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.