Market Insights Snapshot

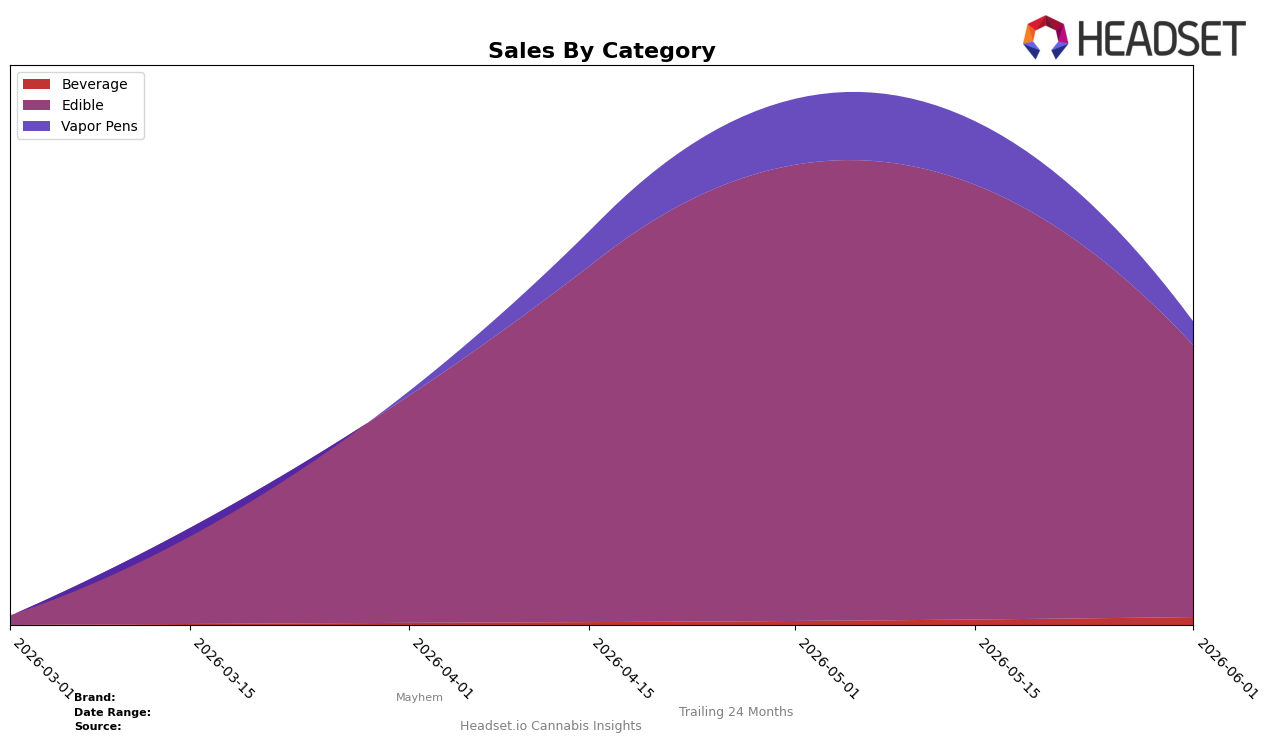

Mayhem’s mix in June 2026 is concentrated in Edible at 89.68% share while Vapor Pens holds 7.70% and Beverage 2.63%; within the month, Edible sales declined 40.49% MoM and Vapor Pens fell 64.46% MoM, contrasted by Beverage growing 97.20% MoM. In New York Edible, the brand sits at rank 58, indicating a lower-tier foothold even as category concentration stays high; this combination implies overexposure to a shrinking monthly Edible base and under-scaled participation in Vapor Pens despite premium pricing at $70.45.

The sharp 40.49% MoM drop in Edible alongside a 64.46% MoM contraction in Vapor Pens, against a 97.20% MoM surge in Beverage from a 2.63% share, suggests Mayhem’s resilience hinges on expanding the smallest line while managing volatility in its core; with an 89.68% Edible dependency and a rank of 58 in New York, the mix points to a need to rebalance toward categories with momentum rather than doubling down on the current center of gravity. The net pattern implies that incremental gains in Beverage can diversify risk and improve rank trajectory only if share lifts beyond low-single digits while Edible contraction is stabilized through price-pack architecture around the $13.78 average.

Competitive Landscape

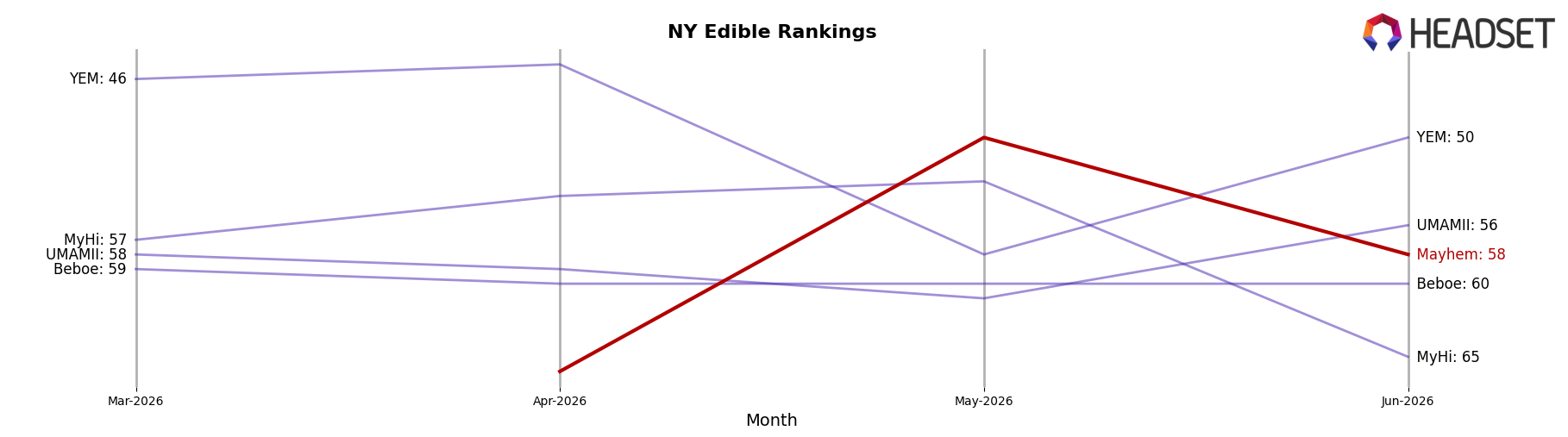

Mayhem sits at rank #58 in New York Edible for June 2026, improving 73 positions from #131 in March 2026 and sitting 8 spots below its peak of #50 reached in May 2026; with no year-over-year rank available, the recent three-month climb is the clearest signal. In the same June 2026 snapshot, Camino held #1 while rising 1 place year over year as sales grew 10.5%, and Wyld stayed at #3 with 26.0% YoY sales growth, indicating that top-tier velocity is outpacing mid-pack movement; compared directionally, Mayhem’s 73-rank three-month ascent exceeds Camino’s 1-rank YoY gain but still leaves a 57-rank gap to the lead. With leaders adding between 10.5% and 26.0% in YoY sales and Mayhem consolidating at #58 after a peak at #50 in May 2026, the trajectory implies a rebound phase where recent rank gains need sustained share capture to avoid reversion as incumbents press advantages.

Notable Products

Blue Raspberry Lemonade Gummy (100mg) posted the steepest decline at -60.03% MoM and slid to rank 5, while Dark Chocolate (100mg) fell -50.00% MoM at rank 4, signaling a sharp pullback in single-serve edibles. The top rank still belongs to Sour Blue Raspberry Lemonade Gummies 10-Pack (100mg) despite a -23.81% MoM drop at rank 1, and Strawberry Kiwi Gummy (100mg) contracted -40.97% MoM at rank 2. With eight of the top ten as Edible SKUs, the mix implies reliance on confections that are compressing month over month, pointing to a need for format diversification to stabilize rank and share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.