Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

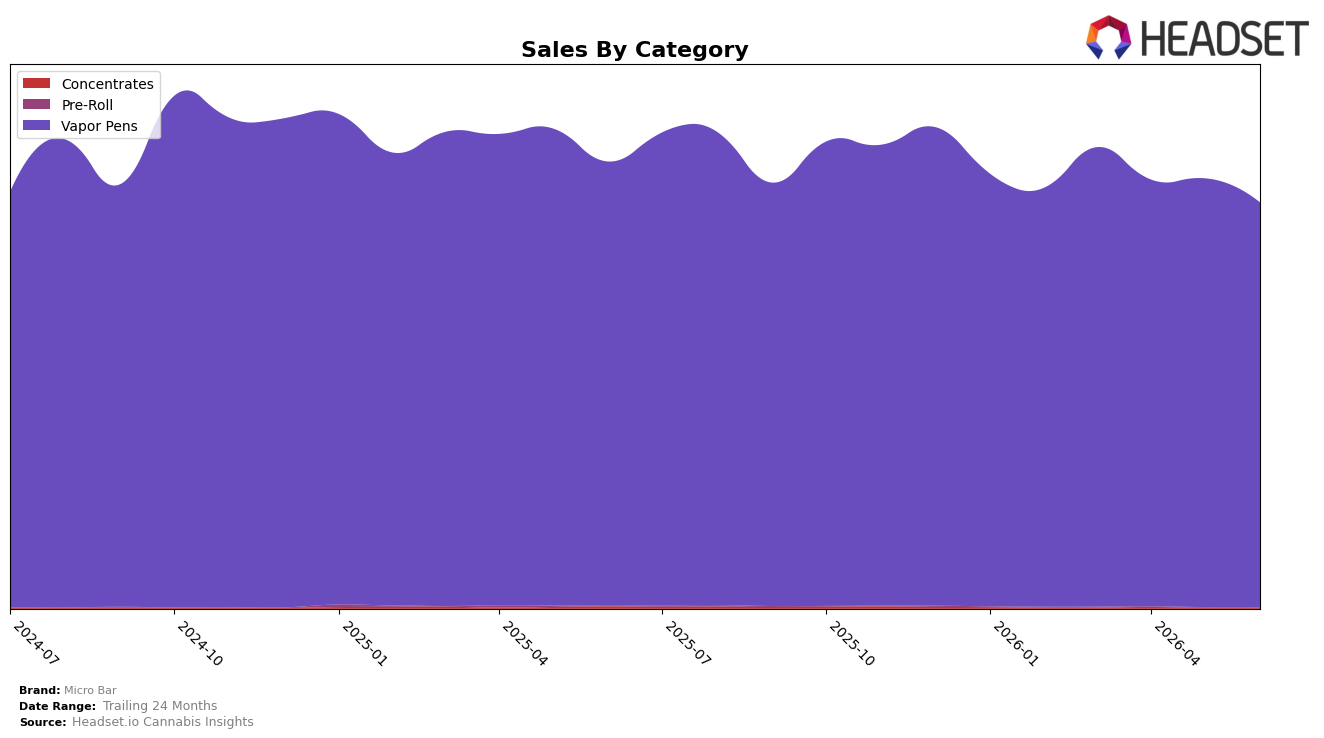

Micro Bar concentrated 99.83% of June 2026 sales in Vapor Pens while holding a rank of 6 in Washington Vapor Pens, with Vapor Pens down 8.78% year over year and 5.61% month over month. The residual mix shrank further as Concentrates slipped 72.49% YoY and 4.32% MoM to 0.13% share, and Pre-Roll fell 76.58% YoY and 2.17% MoM to 0.04% share; average price declined 2.73% YoY to $25.32. The pattern implies a deliberate single-category concentration where incremental declines in minor categories are not offsetting core-category softness, indicating that Micro Bar’s June 2026 performance is governed almost entirely by Vapor Pens dynamics rather than portfolio balance.

Given a 6th-place state-category rank alongside a 9.15% brand sales YoY decline and a 3.37% sales lift versus 24 months, the mix suggests Micro Bar is defending a mid-tier position by leaning into Vapor Pens scale rather than multi-category breadth. With Vapor Pens down 5.61% MoM while Concentrates and Pre-Roll together contribute just 0.17% share, the brand’s exposure to single-category volatility is high; the 2.73% YoY price decrease indicates a price-led tactic that did not prevent the 8.78% YoY volume drag in the core. The implication is that near-term positioning rests on sustaining rank in Washington through Vapor Pens efficiency while the negligible shares in Concentrates and Pre-Roll limit buffering against category-specific downturns.

Competitive Landscape

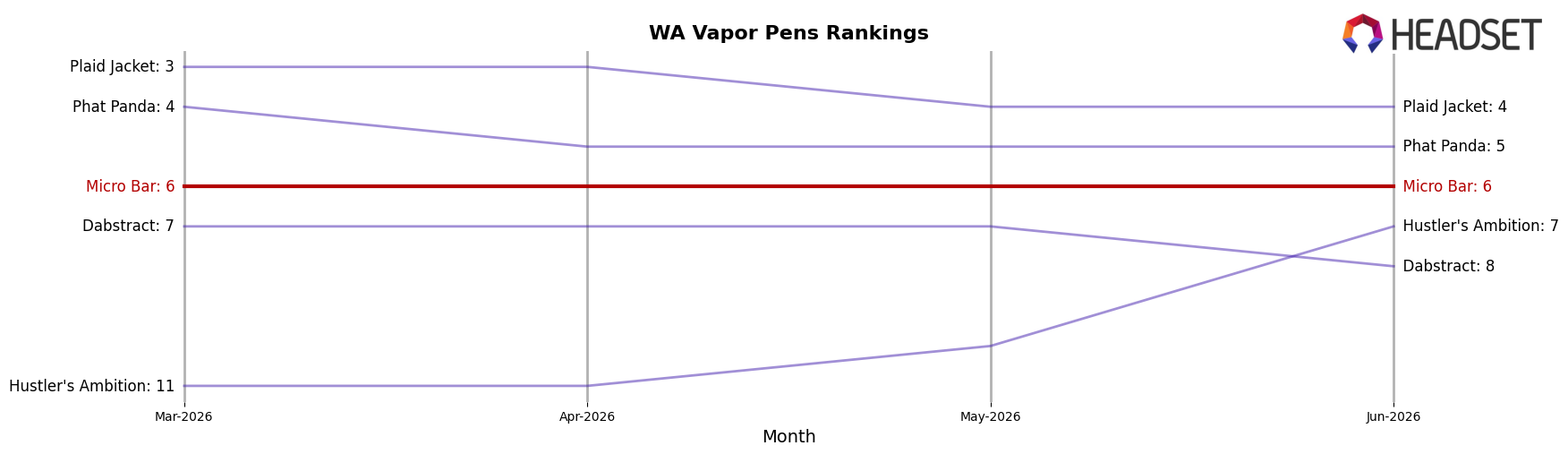

Micro Bar is ranked #6 in WA Vapor Pens in June 2026, slipping 1 position year over year from #5 while holding flat versus March 2026 at #6, and it sits two spots below its peak of #4 from October 2025; in contrast, Mfused held #1 year over year despite a -21.8% sales decline and Plaid Jacket advanced from #6 to #4 with a 17.3% sales increase, indicating that Micro Bar’s static rank amid both upward and downward competitor movements implies share is being maintained rather than expanded, and the trajectory points to stalled gains unless a catalyst pushes it back toward a top-5 position.

Notable Products

White Razz Flavored Distillate Disposable (1g) posted the steepest decline in June 2026 at -22.8% MoM while dropping to rank 8, and Watermelon Mimosa Distillate Disposable (1g) also contracted -11.2% MoM at rank 9, signaling softening traction in flavored distillates. Blackberry Slush Live Resin Liquid Diamond Disposable (1g) rose +26.4% MoM to rank 1 with $136,703 in sales, whereas Melon Bar Distillate Disposable (1g) fell -19.6% MoM to rank 3, creating a widening performance gap between live resin and distillate formats. With nine of the top ten SKUs in Vapor Pens and live resin SKUs advancing while several flavored distillates retreat, the mix points to Micro Bar leaning into higher-potency live resin offerings and pruning weaker flavor-led distillates.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.