Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Crystal Clear is stocked at 329 licensed dispensaries across Washington, California, and 2 other states, 173 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Bellingham, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

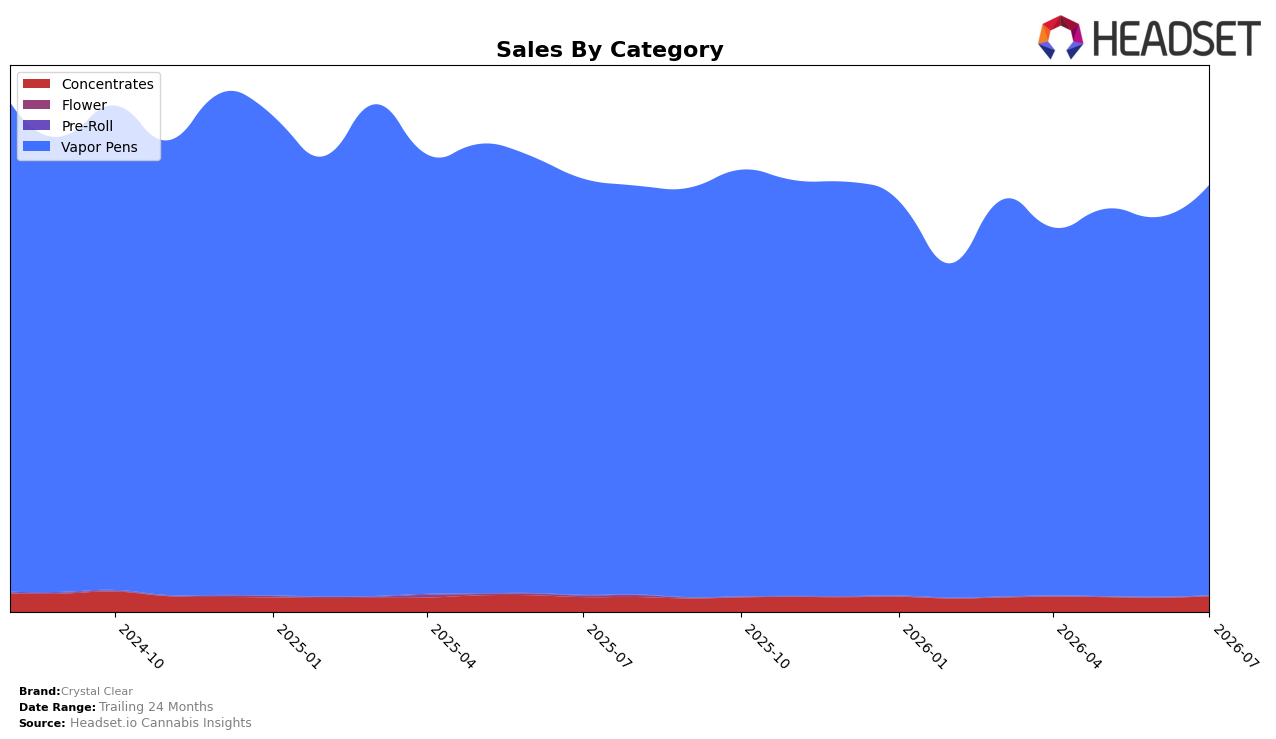

Crystal Clear’s mix in July 2026 is dominated by Vapor Pens at 96.36% share, with Concentrates at 3.64%; within that, Vapor Pens declined 1.35% year over year while Concentrates grew 6.25% year over year. Month over month, both categories expanded — Vapor Pens up 8.12% and Concentrates up 11.21% — alongside a 6.47% decline in average price and a 1.37% brand-level year-over-year sales dip, implying unit gains concentrated in lower-priced SKUs. The pattern points to a reliance on Vapor Pens for volume while a small but faster-growing Concentrates slice provides incremental momentum, suggesting price-led MoM lift without reversing the slight YoY contraction.

Category concentration at 96.36% in Vapor Pens paired with a #1 rank in Vapor Pens in Washington indicates leadership in a single lane, but the 6.25% YoY rise in Concentrates and its 11.21% MoM acceleration create an adjacent foothold for mix diversification. With average price down 6.47% and 24‑month sales down 15.98%, the combination of price elasticity and overexposure to one category implies near-term share defense in Vapor Pens and a tested path to risk balancing via Concentrates, where incremental gains could offset pricing pressure if scaled beyond 3.64% share.

Competitive Landscape

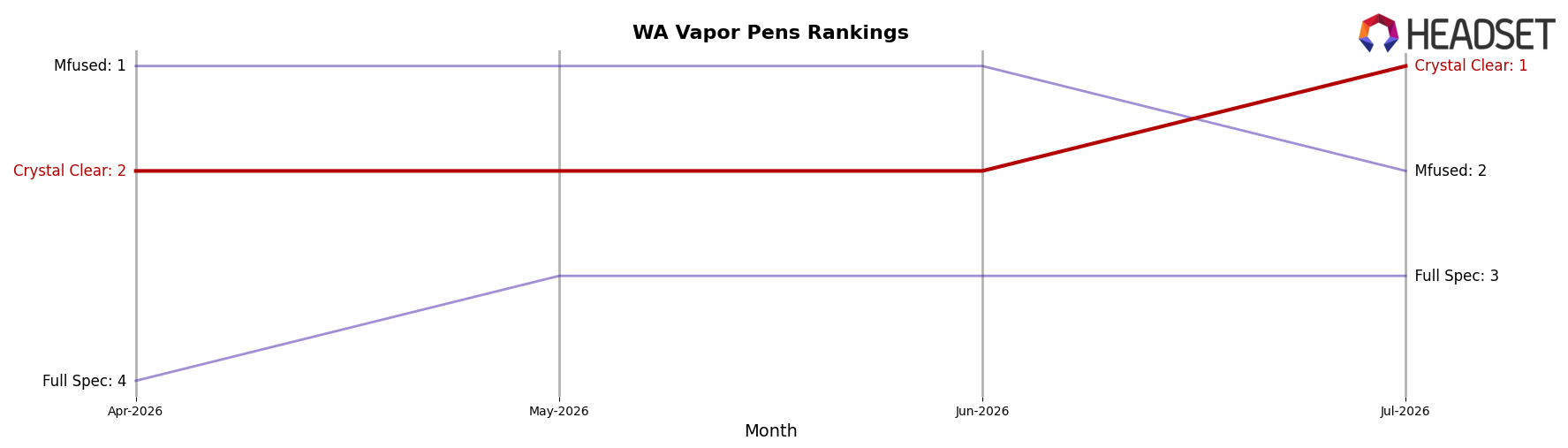

Crystal Clear ranks #1 in WA Vapor Pens in July 2026, improving 1 position YoY from #2, and rising 1 spot from April 2026 when it sat at #2; this ascent coincides with Mfused slipping from #1 to #2 while posting a -26.1% YoY sales change, and Full Spec advancing from #6 to #3 on +12.9% YoY growth, indicating Crystal Clear’s move to its peak rank (#1) in July 2026 is aided by competitor contraction at the top and faster upward mobility in the chasing pack, implying a consolidation window where holding share depends on converting the #2 displacement into sustained lead over brands gaining ranks.

Notable Products

Blue Dream Terp Sauce Cartridge (1g) posted the standout move in July 2026 with a 69.6% month-over-month gain to rank 3, while category leader Maui Wowie Distillate Cartridge (1g) slipped 2.5% but held rank 1. White Widow Blast Distillate Disposable (1g) advanced 20.0% at rank 2 and its companion White Widow Blast Distillate Cartridge (1g) rose 36.9% at rank 6, indicating cross-format pull. With all top-10 SKUs in Vapor Pens and two Maui Wowie variants sitting at ranks 1 and 4 with -2.5% and +23.9% respectively, the mix implies Crystal Clear is consolidating around a few flavor-led lines while accelerating terp-forward and disposable formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.