Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

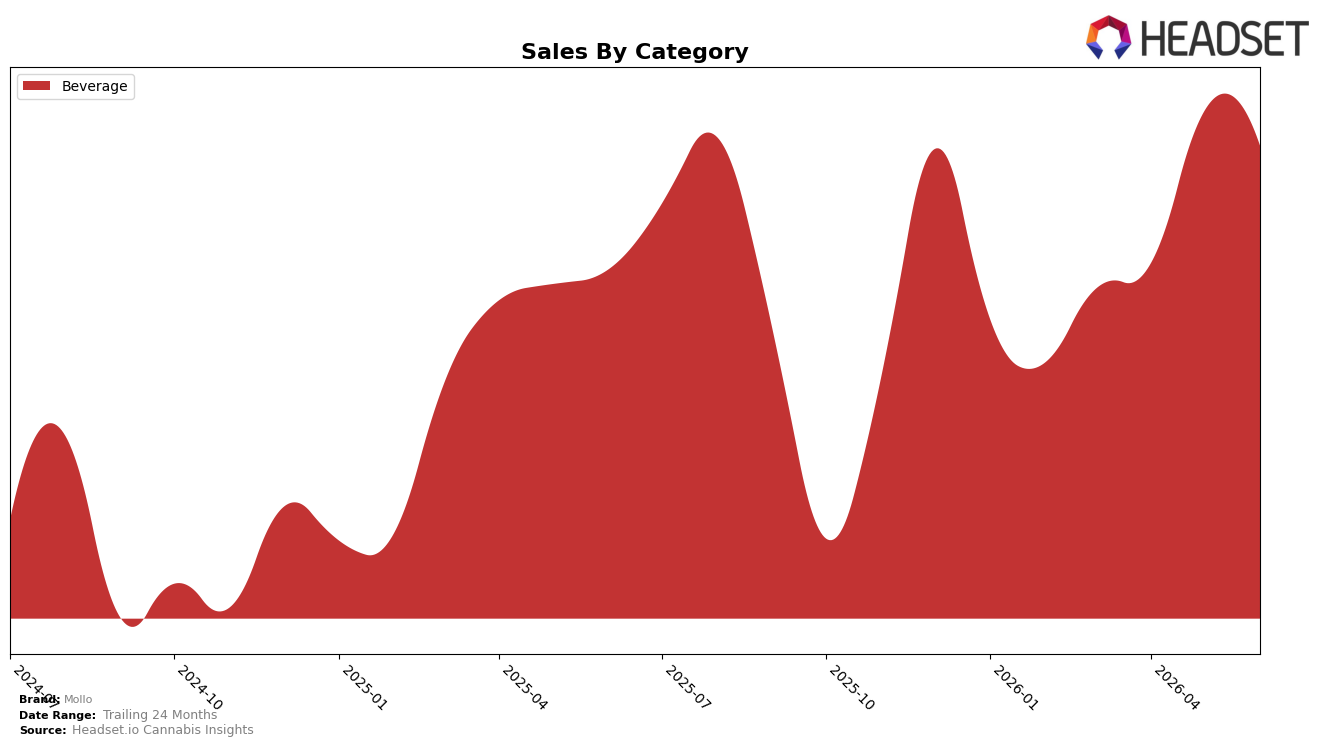

In June 2026, Mollo concentrated 100.0% of sales in Beverage, with year-over-year sales up 8.6% while month-over-month slipped 2.2%, and the average price rose 19.5% YoY alongside a category share that remained at 100.0%. Despite a 2.2% MoM dip in Beverage sales, the 8.6% YoY gain paired with a 19.5% YoY price increase suggests unit volumes were roughly flat to modestly down, indicating price rather than volume drove the annual uplift; the pattern implies Mollo is leaning into pricing power within a single-category footprint rather than expanding mix breadth.

The tighter single-category focus aligns with a #2 rank in Beverage in British Columbia while average price climbed 19.5% YoY and total brand sales advanced 8.6% YoY, implying Mollo is trading up within its lane rather than broadening into adjacent formats. Holding a #2 position amid a 2.2% MoM sales contraction and a 19.5% YoY price lift points to elasticity headwinds at the margin but sustained premium capture over the year, which implies Mollo’s near-term positioning depends on balancing price with velocity to defend rank rather than diversifying away from Beverage.

Competitive Landscape

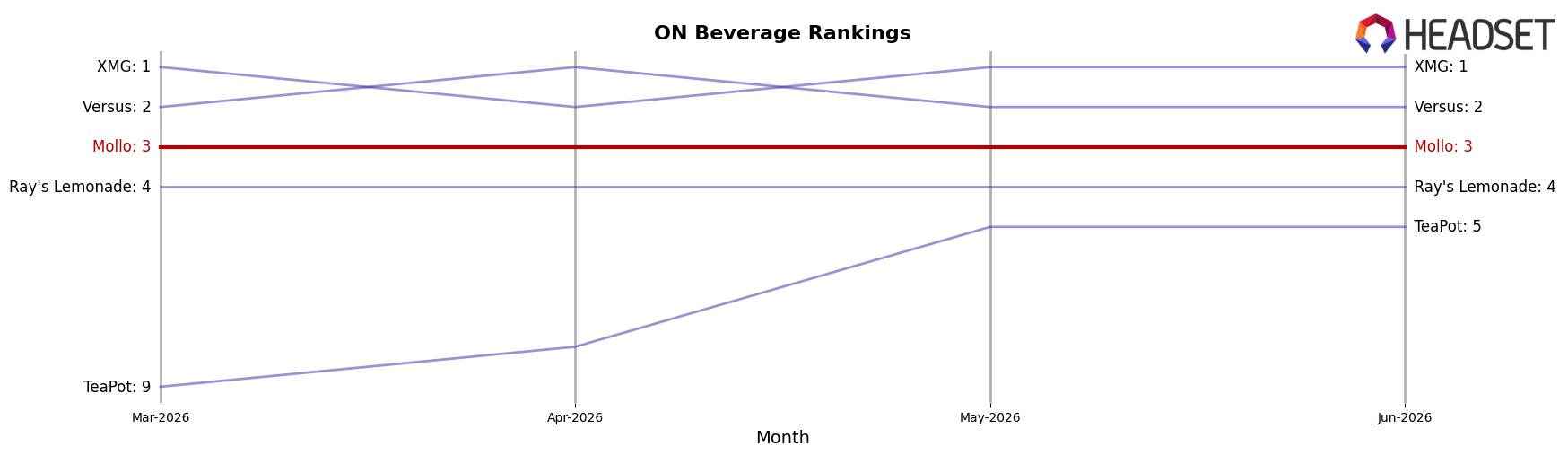

Mollo sits at #3 in ON Beverage in June 2026, improving 1 rank position year over year from #4, while holding flat versus March 2026 at #3; against this backdrop, XMG stayed at #1 year over year with a -36.99% sales change and Versus held #2 with a -5.01% sales change, whereas TeaPot jumped from #10 to #5 alongside 129.54% sales growth and Ray's Lemonade moved from #5 to #4 with 23.46% growth; given Mollo’s peak at #2 in August 2025 and its current #3 with a +1 YoY rank shift, the pattern implies Mollo is stabilizing just below the top tier and must outpace mid-pack climbers to retake #2.

Notable Products

CBG/THC 2:1 Mango Seltzer (20mg CBG, 10mg THC, 355ml) posted the steepest decline at -12.7% while holding rank 4, and CBG/THC 2:1 Blackberry Seltzer (20mg CBG, 10mg THC, 355ml) slipped -11.3% at rank 1, signaling pressure at the top even as the 4-Pack format surged. THC/CBG 1:1 Orchard Chill'r Apple Cider Sparkling Beverage (10mg CBG, 10mg THC, 355ml) rose 9.5% at rank 6 versus CBG/THC 2:1 Watermelon Lime Seltzer (20mg CBG, 10mg THC, 12oz, 355ml) at -8.8% and rank 2, and the CBG/THC 2:1 Wildberry Acai Seltzer 4-Pack (80mg CBG, 40mg THC, 1420ml) jumped 29.4% at rank 10, indicating single cans are softening while multipacks gain traction. With eight of the top ten as CBG-forward seltzers and only one 1:1 can in the top six, the mix tilts toward higher-CBG beverages, implying Mollo’s near-term growth will come from pack-size upsell and flavor rotation rather than relying on the flagship singles.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.