Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

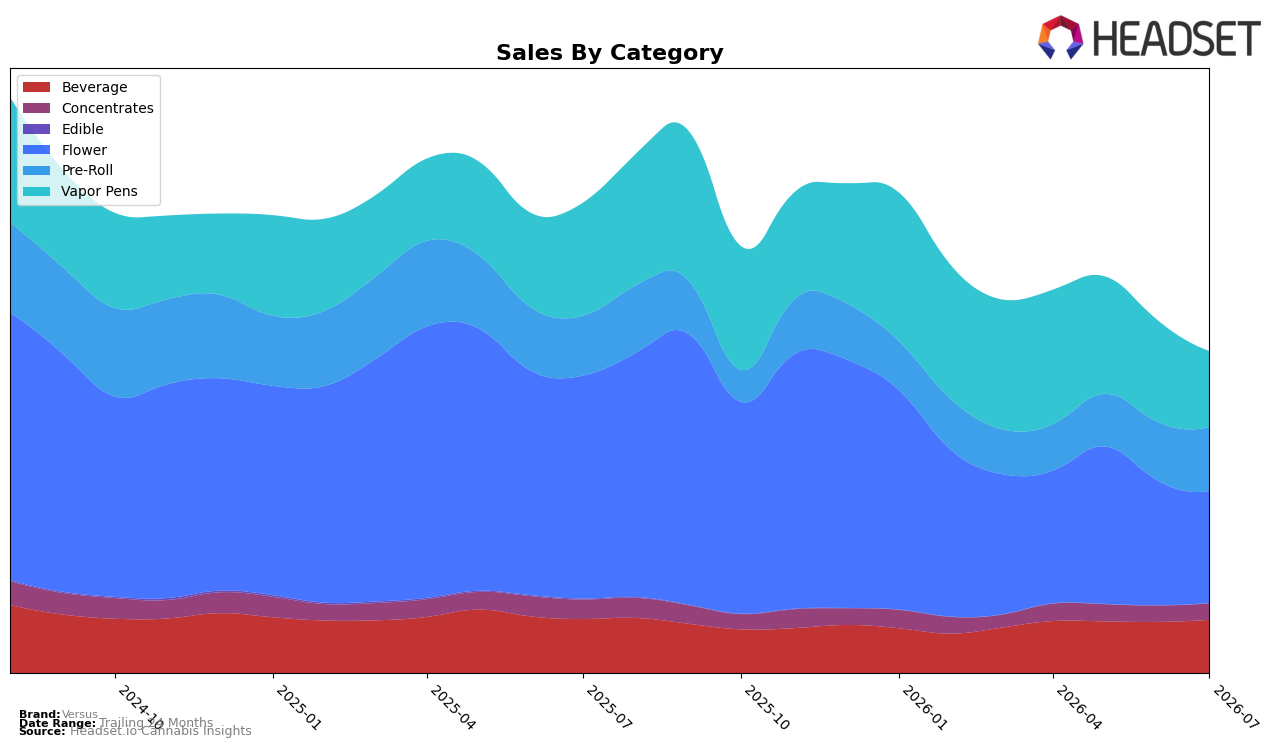

Market Insights Snapshot

In July 2026, Versus’s mix tilted toward Flower at 34.84% share with year-over-year change of -49.78% and month-over-month change of -10.04%, while Vapor Pens held 23.58% share with -32.99% YoY and -25.23% MoM, indicating contraction in its two largest categories. Offsetting this, Pre-Roll rose 6.85% YoY and 8.94% MoM to 19.89% share, and Beverage posted -1.62% YoY with a 3.91% MoM lift to 16.60% share, suggesting incremental stabilization from ready-to-consume formats. Concentrates were comparatively flat with -15.64% YoY and 0.90% MoM at 5.07% share, while Edible remains minimal at 0.02% share despite a 190.75% MoM rebound against a -93.10% YoY base. The pattern implies Versus is overexposed to declining inhalables while gains in Pre-Roll and Beverage are not yet large enough to counter a -31.64% brand-level YoY decline and a -19.74% YoY drop in average price.

With Flower ranked 13 in British Columbia and accounting for 34.84% of sales, the -10.04% MoM pullback alongside Vapor Pens’ -25.23% MoM suggests short-term share vulnerability in core inhalables, even as Pre-Roll’s 8.94% MoM and Beverage’s 3.91% MoM point to pockets of momentum. The juxtaposition of Pre-Roll’s 6.85% YoY growth against Flower’s -49.78% YoY and Vapor Pens’ -32.99% YoY indicates a consumer shift within the portfolio toward lower-price-per-unit, convenience-led formats. This mix, combined with a -19.74% YoY average price change and only 5.07% of sales in Concentrates with -15.64% YoY, implies Versus’s current positioning is trending toward value-oriented, ready-to-consume options, requiring either deeper penetration in Pre-Roll/Beverage or a reset in inhalables to stabilize rank and share.

Competitive Landscape

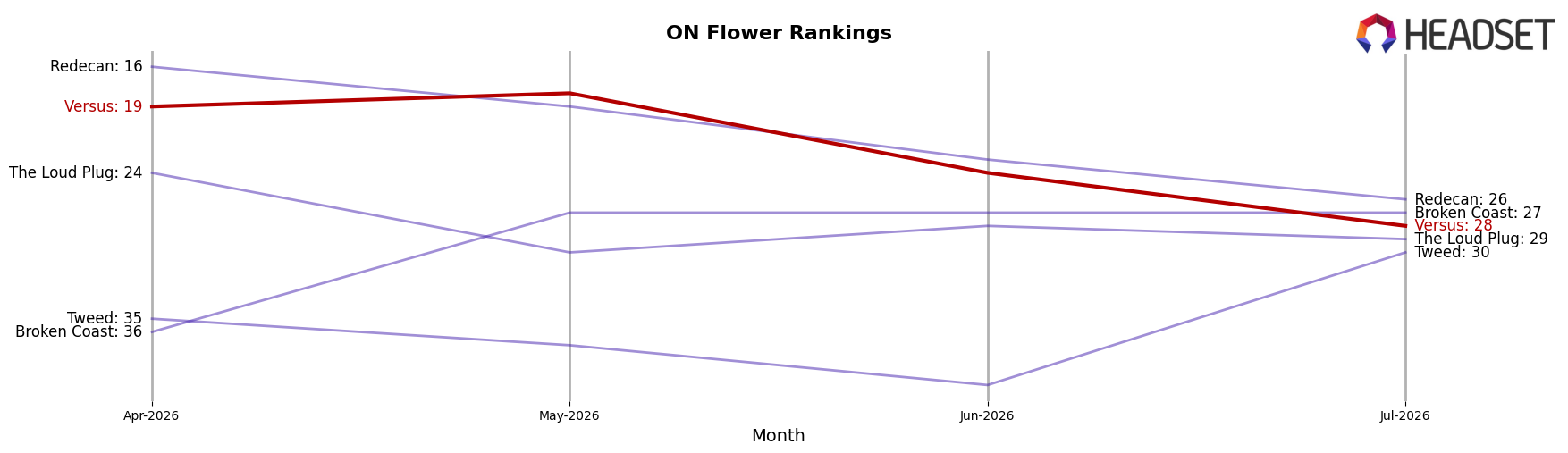

Versus sits at rank #28 in ON Flower in July 2026, down 15 positions year over year from #13, and 9 places below its April 2026 rank of #19; versus its peak at #8 in December 2025, the brand has fallen 20 spots, indicating sustained share erosion rather than seasonal noise. In contrast, Shred climbed to #1 from #2 with 17.23% YoY sales growth, while Spinach advanced to #2 from #4 alongside 31.07% YoY growth, and Back Forty / Back 40 Cannabis slipped to #4 from #1 with a -5.44% YoY decline—placing Versus’s -15 rank swing against competitors gaining rank and double‑digit growth amplifies the gap. The pattern implies Versus’s downward rank trajectory is tied to underparticipation in the high-growth tier, and absent a reversal in relative velocity versus leaders adding 2–4 rank positions, the brand is likely to keep ceding distribution and share.

Notable Products

Blueberry Pomegranate Rapid Seltzer (10mg THC, 350ml) posted the steepest movement in July 2026 with a -18.3% month-over-month drop and slid to rank 9, while CBD/THC 1:1 Neon Rush Carbonated Soda (10mg CBD, 10mg THC, 355ml) in rank 1 grew 3.9% MoM and Key Lime Rapid Seltzer (10mg THC, 355ml) in rank 3 rose 3.1% MoM. With six of the top ten coming from Beverage, the category concentration suggests Versus is tilting toward breadth within drinks even as one flavor underperforms, implying the portfolio is leaning on lineup depth rather than single-SKU momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.