Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

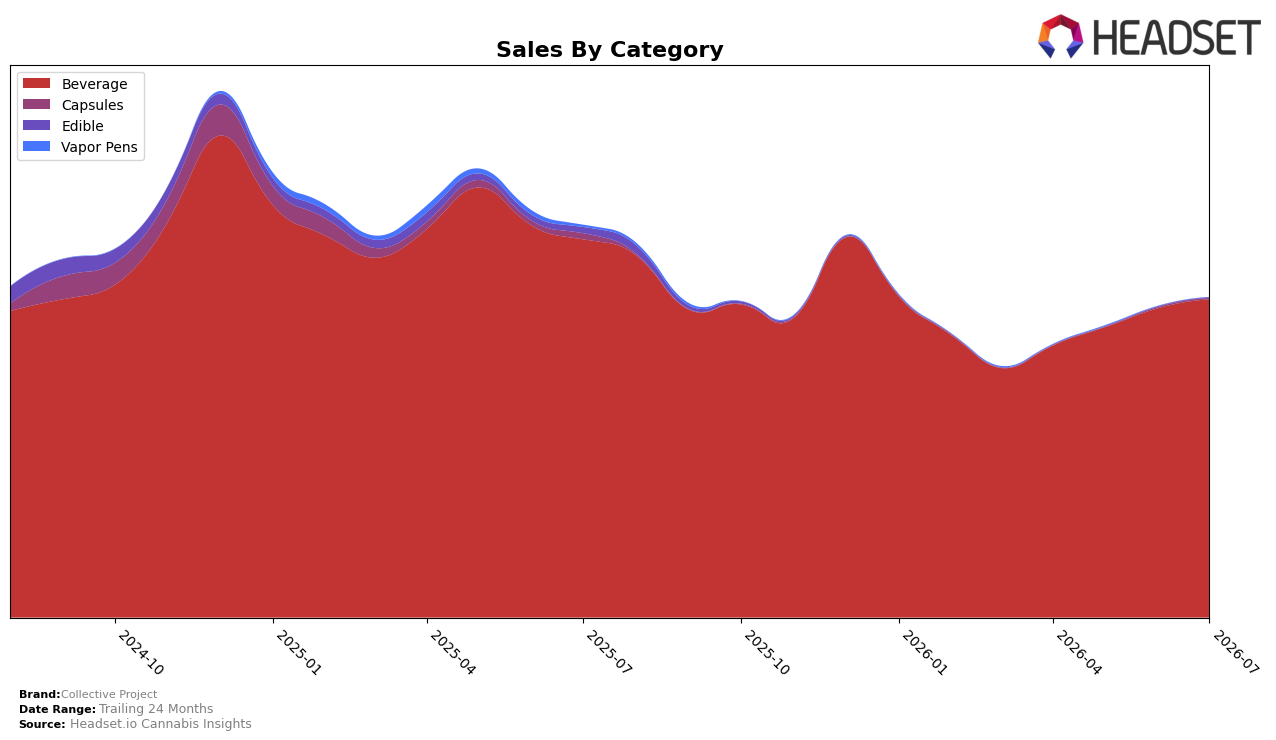

In July 2026, Collective Project remained concentrated in Beverage at 99.68% share while Capsules held 0.30% and Edible just 0.02%, with Beverage up 2.91% month over month but down 15.87% year over year; Capsules inched up 2.65% month over month yet fell 83.11% year over year, and Edible contracted 71.13% month over month and 98.75% year over year. Despite a 4.94% year-over-year increase in average price alongside a brand-level sales decline of 18.46% year over year, the rank at 8 in Beverage in Alberta signals that mix stability in Beverage contrasts with deep retrenchment in adjacent formats, implying the brand is leaning into a single-category strategy with limited cross-format cushioning.

The 2.91% month-over-month lift in Beverage against a 15.87% year-over-year decline, paired with Capsules at 0.30% share and 83.11% year-over-year erosion, indicates pricing power is concentrated where the brand is strongest while experimentation in adjacent forms has been deprioritized. With Beverage anchoring 99.68% of sales and the Beverage rank at 8 in Alberta, the July 2026 mix suggests a defensive focus on core ready-to-drink velocity rather than portfolio breadth, which likely limits exposure to trial in higher-priced Capsules and suppresses recovery potential from the 18.46% brand sales decline year over year.

Competitive Landscape

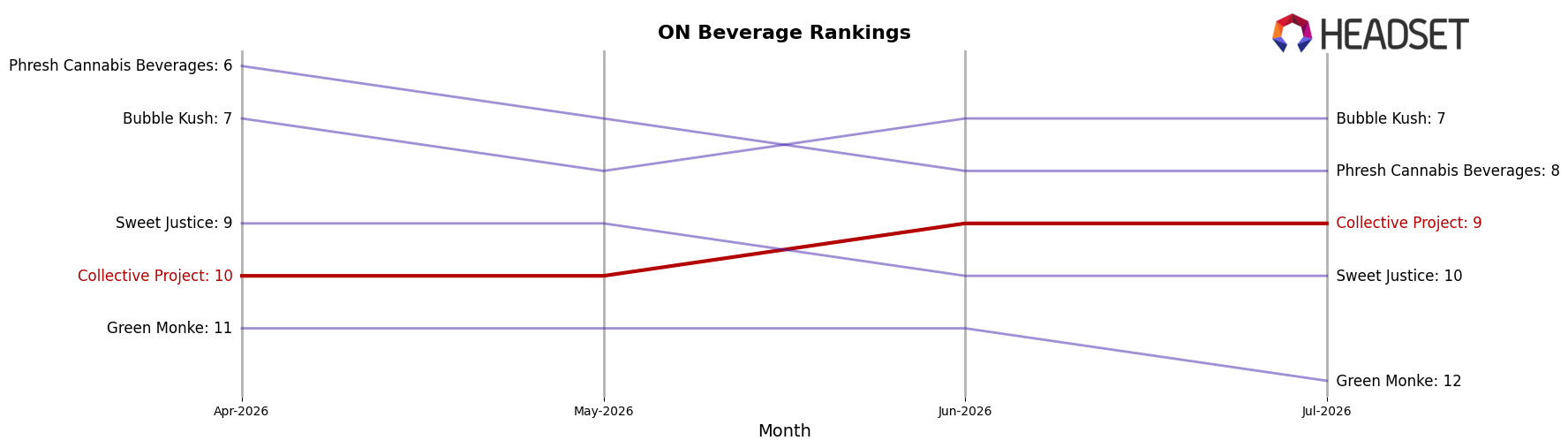

Collective Project sits at #9 in ON Beverage in July 2026, down 5 ranks from #4 year over year, while improving 1 position from #10 over the last three months; that contrasts with Versus holding #1 with a +2 rank lift from #3 and +18.1% year-over-year sales growth, and XMG sliding to #2 from #1 alongside a -37.2% sales contraction. Against Mollo at #3 (down 1 rank with -1.1% sales) and Ray's Lemonade at #4 (up 1 rank with +28.7% sales), Collective Project’s retreat from its #3 peak in June 2025 and current #9 position imply the brand is ceding relative momentum to faster-rising peers and will need mix or velocity gains to reverse the rank decline.

Notable Products

Botany - CBD/THC 1:1 White Peach & Cardamom Sparkling Botanical Water (10mg CBD, 10mg THC, 355ml) posted the steepest decline at -15.0% MoM, falling to rank 6 while the CBD/THC 1:1 Original Blood Orange, Yuzu & Vanilla Sparkling Juice (10mg CBD, 10mg THC, 355ml) rose 23.0% to hold rank 1. Happy Place - CBG/THC 2:1 Mango Peach & Yuzu Juice Sparkling Beverage (20mg CBG, 10mg THC, 355ml) surged 25.2% to rank 2, whereas the CBD/THC 1:1 Original Blood Orange, Yuzu & Vanilla Sparkling Juice 4-Pack (40mg CBD, 40mg THC, 12oz, 355ml) slid -21.2% at rank 9; eight of the top ten are Beverage SKUs centered on fruit-forward sparkling formats. With single-serve units up 23.0% at rank 1 while the equivalent 4-Pack is down -21.2% at rank 9 and total July 2026 sales for the leader at $142,199, the mix signals a shift toward trial-size, on-the-go consumption over multi-pack pantry loading.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.