Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Baked Bros is stocked at 107 licensed dispensaries across Arizona, with the deepest coverage in Phoenix, Tucson, Mesa, Chandler, and Tempe. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

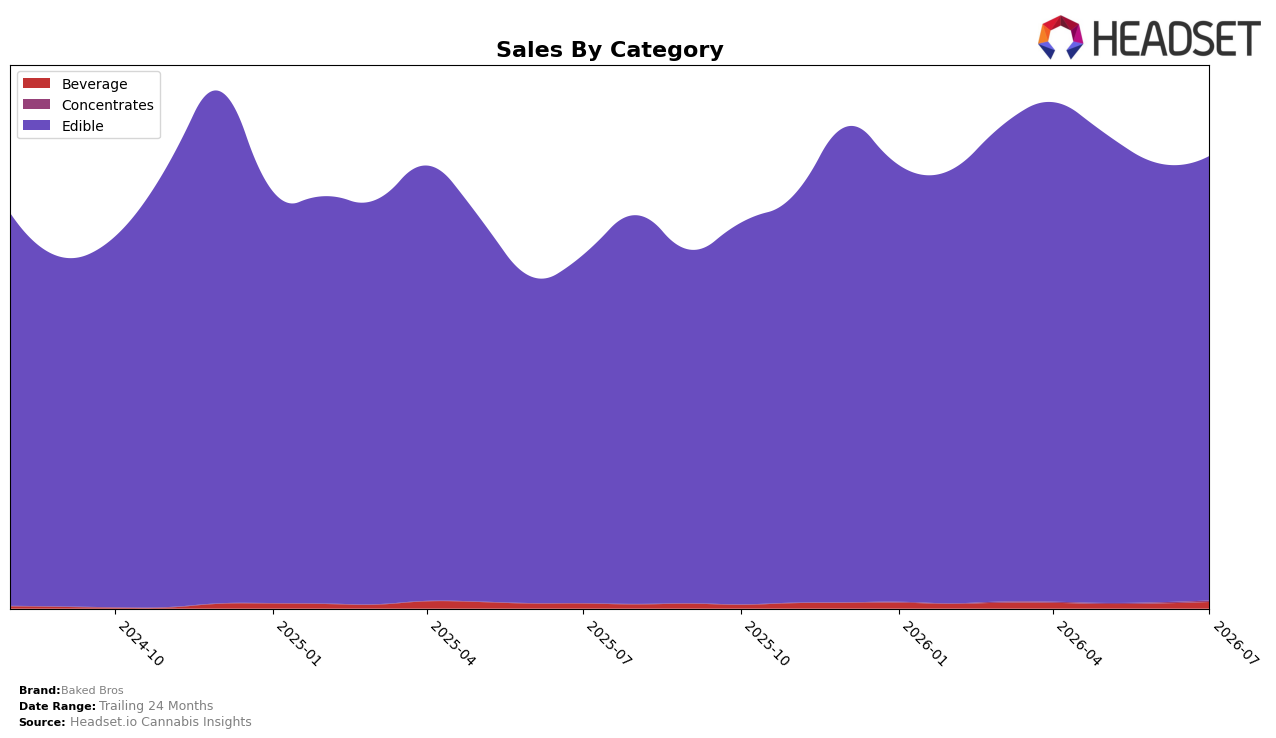

In July 2026, Baked Bros concentrated 98.40% of sales in Edible, up 1.24% month over month and 27.68% year over year, while overall brand sales grew 28.05% year over year and average price fell 1.62%. Beverage expanded to 1.38% share with a 31.02% month-over-month jump and 34.21% year-over-year growth, and Concentrates, though just 0.22% share, accelerated 46.61% month over month from a small base. With Edible anchoring volume and Beverage outpacing on both month-over-month and year-over-year rates, the pattern implies Baked Bros is using price stability around $12.10 in Edible to defend scale while testing adjacency-led growth that can diversify mix without diluting the Edible core.

Positioning-wise, the 3rd-place Edible rank in Arizona pairs with a 1.24% month-over-month Edible lift and a 31.02% month-over-month Beverage surge to suggest headroom to convert loyalty in Edible into trial across smaller formats. The 27.68% Edible year-over-year growth against a 34.21% Beverage year-over-year pace, alongside a 1.62% brand-wide price decline, implies a deliberate trade-up on volume rather than price, signaling a strategy to preserve rank in Edible while seeding Beverage and Concentrates as incremental basket drivers.

Competitive Landscape

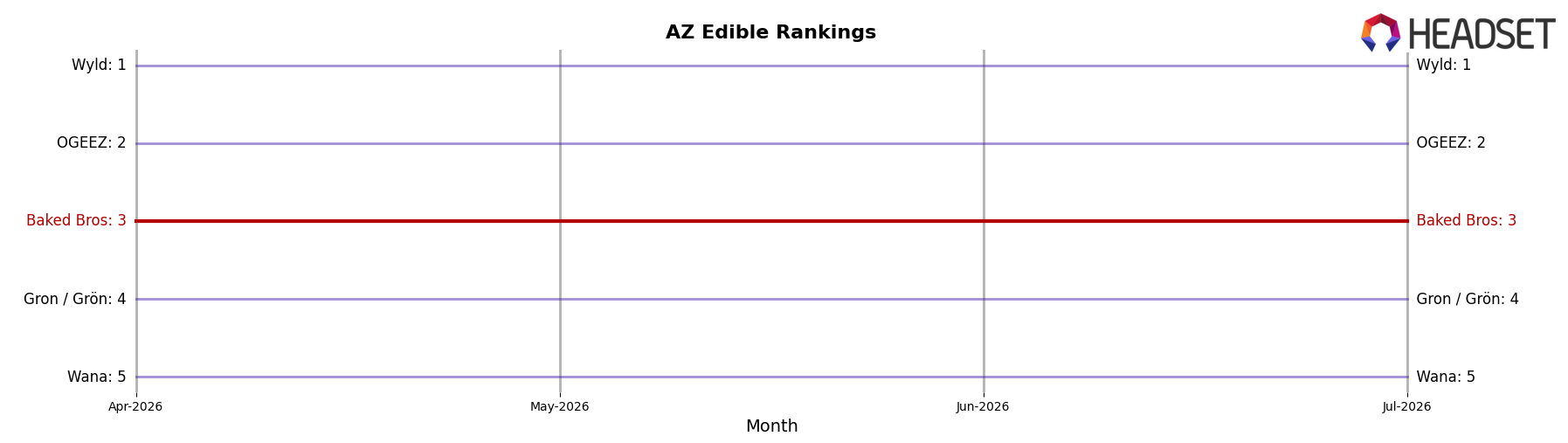

Baked Bros is ranked #3 in AZ Edible in July 2026, a 1-place improvement from #4 in July 2025, while holding flat versus April 2026 at #3; by contrast, Wyld held #1 year over year but posted a -9.98% sales change, and OGEEZ stayed at #2 with +10.74% YoY sales, marking a divergence where the top spot softened as the runner-up expanded. Baked Bros’ peak was #2 in December 2024 and it remains #3 for three consecutive months, whereas Gron / Grön slipped from #3 to #4 with -1.76% YoY sales and Wana moved from #6 to #5 with +6.97% YoY sales; this pattern implies Baked Bros’ incremental rank gain is stabilizing in upper-tier contention but requires displacing a growing #2 to reclaim its prior #2 peak.

Notable Products

Happy - CBD/CBC/THC 1:1:1 Jack Herer Pomegranate Nectarine Gummies 10-Pack (100mg CBD, 100mg CBC, 100mg THC) posted the standout surge with a 330.7% month-over-month jump to $155,392, leaping into rank 2 while Sleepy - CBD/THC 2:1 Blackberry Acai x Granddaddy Purple Gummies 10-Pack (200mg CBD, 100mg THC) climbed 52.8% to rank 1. By contrast, Dreamy - CBN/THC 5:2 Elderberry Plum Gummies 10-Pack (250mg CBN, 100mg THC) fell 12.6% and slid to rank 8, while Stoney - CBG/THC 1:1 OG Kush x Prickly Pear Lemonade Gummies 10-Pack (100mg CBG, 100mg THC) dipped 1.3% at rank 3. Eight of the top ten are Edible gummies, and Wild Strawberry Live Hash Rosin Gummies 10-Pack (100mg) advanced 9.5% at rank 6 as Very Berry Live Hash Rosin Gummies 10-Pack (100mg) rose 70.2% at rank 5, indicating flavor-driven Live Rosin variants are gaining share even as certain minor-cannabinoid sleep SKUs soften. The pattern implies Baked Bros is pivoting toward mood-forward, multi-cannabinoid and Live Rosin gummies that can scale quickly, while sleep-focused formats face selective pruning.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.