Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Papa & Barkley is stocked at 820 licensed dispensaries across California and New York, 684 of them in California, with the deepest coverage in Los Angeles, San Francisco, Sacramento, San Diego, and Long Beach. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

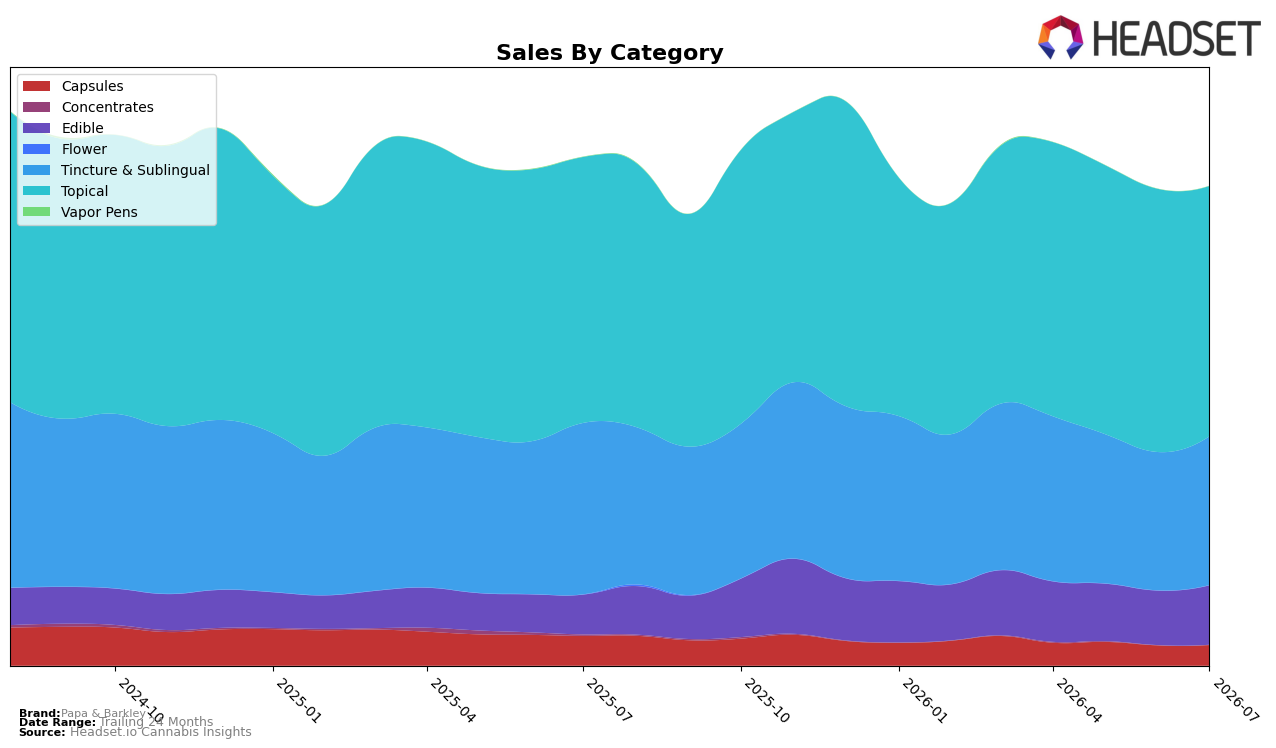

In July 2026, Papa & Barkley’s mix was anchored by Topical at 52.30% share (yoy -5.90%, mom -4.89%) and Tincture & Sublingual at 31.06% share (yoy -13.19%, mom +7.61%), while Edible expanded to 12.37% share (yoy +49.64%, mom +9.11%) and Capsules contracted to 4.27% share (yoy -31.02%, mom +1.78%). Despite a brand-level sales decline of 5.73% year over year and a 3.72% drop in average price, Papa & Barkley held rank 1 in Topical within California, indicating that the category headwind in Topical and the double‑digit year-over-year pullback in Tincture & Sublingual are being partially offset by rapid Edible growth; the pattern implies a pivot from reliance on Topical toward a more diversified mix where Edible momentum cushions Topical softness.

The combination of a -5.90% year-over-year decline in Topical and a -13.19% year-over-year decline in Tincture & Sublingual, alongside a +49.64% year-over-year surge in Edible and a +7.61% month-over-month lift in Tincture & Sublingual, implies Papa & Barkley is rebalancing toward faster-turn formats as price trims (-3.72% yoy) seek elasticity. With month-over-month contraction in Topical (-4.89%) but expansion in Edible (+9.11%), the brand’s position as rank 1 in Topical within California now functions more as a credibility anchor than a growth engine; the pattern suggests that sustaining leadership will require defending Topical share while leaning into Edible and stabilizing Tincture & Sublingual to mitigate the 17.69% two-year sales erosion.

Competitive Landscape

Papa & Barkley holds rank #1 in California Topical for July 2026 with no year-over-year rank change from #1 to #1, and no three-month change from #1 to #1, while peak rank remained #1 in July 2026; in contrast, Mary's Medicinals stayed at #2 year over year as sales fell 98.35%, and Liquid Flower advanced from #6 to #4 with sales up 60.45%. Meanwhile, Buddies held #3 with sales up 50.27%, and Sweet ReLeaf (CA) remained at #5 with sales down 0.07%; this mix of flat rank at the top alongside sharp gains and declines below implies Papa & Barkley’s unshifted #1 position masks intensifying pressure from faster-rising mid-pack competitors and a widening performance gap versus declining incumbents.

Notable Products

The steepest decline came from CBD/THC 3:1 CBD Rich Releaf Balm (90mg CBD, 30mg THC, 15ml, 0.5oz), which fell 12.4% month over month to rank 10, while the flagship Sleep Releaf- CBD/CBN/THC 1:1:1 Berry Pomegranate Solventless Gummies 20-Pack (100mg CBN, 100mg CBD, 100mg THC) rose 9.5% to hold rank 1. Three of the top five are Topical SKUs with mixed movements — CBD/THC 1:3 THC Rich Releaf Balm (100mg CBD, 300mg THC, 50ml, 1.7oz) slid 2.3% at rank 2 and CBD/THC 3:1 CBD Rich Releaf Balm (450mg CBD, 150mg THC, 50ml 1.7oz) dipped 5.1% at rank 4 — implying some price or occasion sensitivity even as the category remains concentrated. Tinctures moved up quietly, with THC Releaf Oil Tincture (1000mg THC, 15ml) gaining 11.2% at rank 7 and the CBD/THC 30:1 CBD Rich Releaf Tincture (435mg CBD, 15mg THC, 15ml) up 3.6% at rank 9, while a second gummy, Sleep Releaf- CBD/CBG/THC 1:1:1 Pear Apple Recover Gummies 20-Pack (100mg CBD, 100mg CBG, 100mg THC), advanced 18.0% at rank 8. The pattern implies Papa & Barkley is tilting toward ingestibles for incremental growth while maintaining a Topical-led base, suggesting portfolio balance will hinge on nurturing gummy velocity alongside stabilizing mid-ranked balms.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.