Market Insights Snapshot

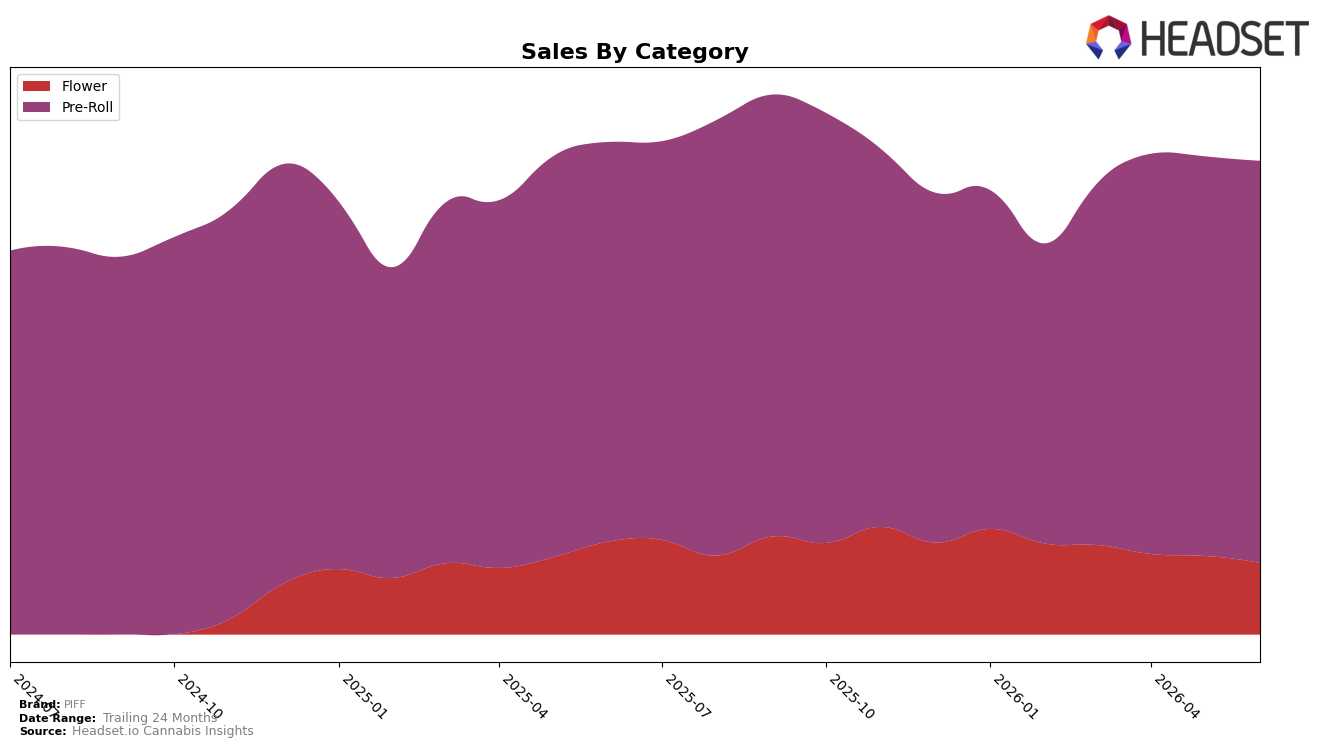

PIFF concentrated 84.95% of June 2026 sales in Pre-Roll while Flower accounted for 15.05%, with Pre-Roll up 0.65% year over year and 0.64% month over month, versus Flower down 23.12% year over year and down 9.04% month over month. Average price rose 3.61% year over year to $12.93 as Pre-Roll average price sat at $11.95 and Flower at $24.02, indicating mix-driven stabilization even as total brand sales declined 3.83% year over year; the pattern implies PIFF leaned into Pre-Roll to offset Flower contraction and sustain overall velocity.

In Ontario Pre-Roll, PIFF held rank 9 while brand sales advanced 57.42% over 24 months and dipped 3.83% year over year, a posture consistent with share defense in a mature lane rather than expansion via Flower where double-digit declines persisted. With Pre-Roll growing month over month by 0.64% as Flower fell 9.04% in the same period, the category tilt implies PIFF is prioritizing depth in its leading segment to maintain top-10 relevance in Ontario rather than diversifying into higher-priced but shrinking Flower, trading broader portfolio reach for ranked stability.

Competitive Landscape

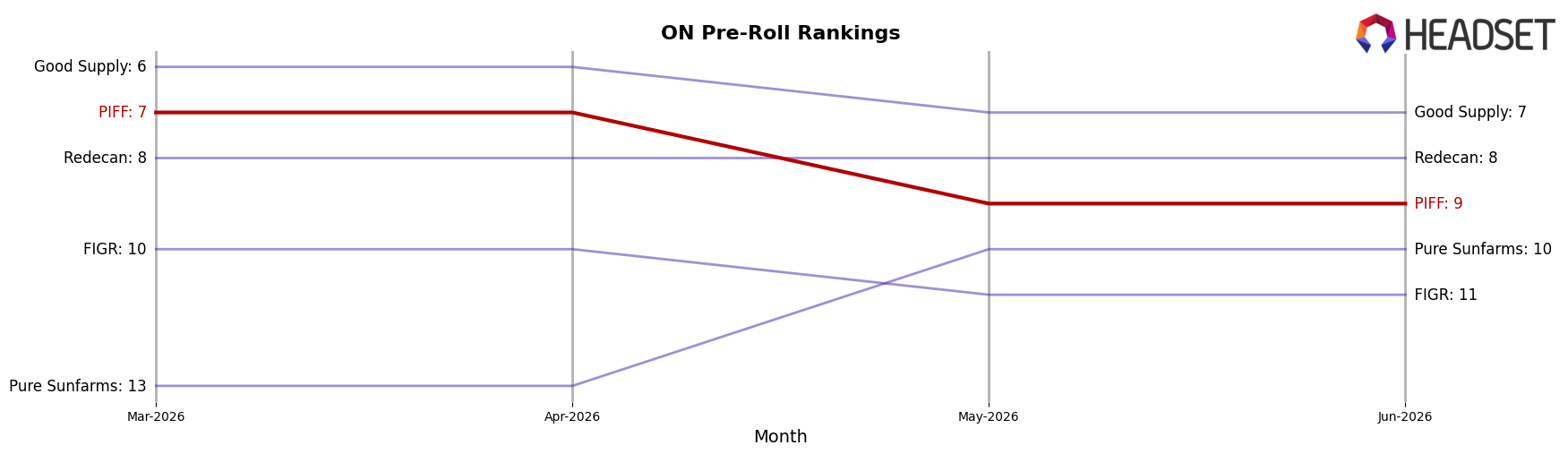

PIFF sits at rank #9 in ON Pre-Roll in June 2026, improving 2 positions from #11 year over year, but sliding 2 spots from #7 in March 2026 and sitting three off its peak at #6 in September 2025; meanwhile, Back Forty / Back 40 Cannabis advanced from #3 to #1 alongside a 74.6% year-over-year sales increase while Jeeter fell from #2 to #4 with a 48.5% year-over-year decline, indicating PIFF’s modest rank climb year over year is being outpaced by faster movers at the top and its recent quarter-over-quarter slippage signals share consolidation above it.

Notable Products

Cali Kush Milled (7g) posted the steepest movement in June 2026 with a -15.7% month-over-month decline and fell to rank 10, while Maui Wowie Pre-Roll 2-Pack (2g) held rank 1 despite a -4.7% dip. Eight of the top ten are Pre-Roll SKUs, and within that concentration the Maui Wowie Pre-Roll 14-Pack (7g) in rank 5 inched up +1.5% as the Cali Kush Pre-Roll 2-Pack (2g) in rank 2 slipped -8.5%, implying consumers are tilting toward multi-pack Pre-Rolls even as single-pack leaders soften. Panama Gold Pre-Roll 2-Pack (2g) climbed +20.4% at rank 6, whereas Juicy Blunt (1g) was essentially flat at -0.1% in rank 3, indicating momentum is accruing to value-forward or differentiated Pre-Roll formats more than to steady singles.

With Pre-Rolls dominating share of ranks and Maui Wowie variants spanning both single and 14-pack formats around $413,314 on the 14-Pack, the pattern implies PIFF’s commercial direction is consolidating around branded Pre-Roll franchises and multi-pack configurations while Flower SKUs absorb volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.