Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

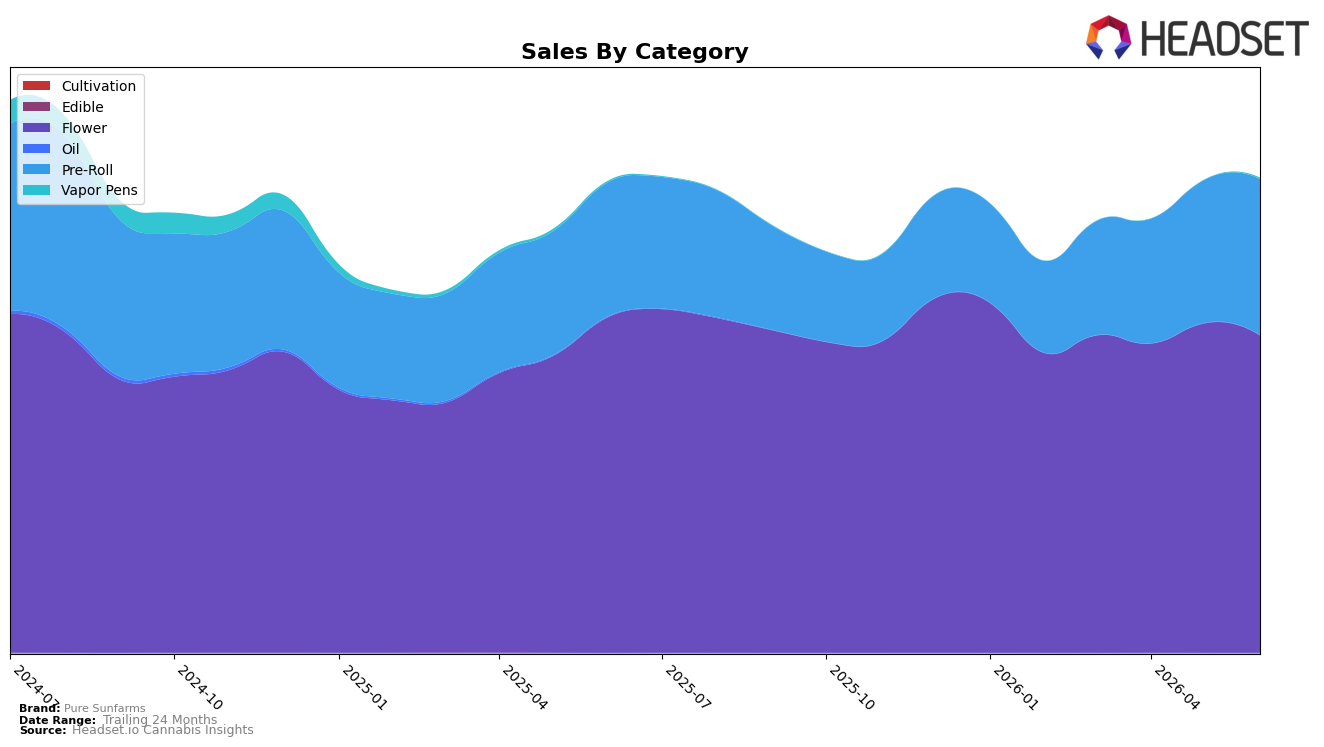

In June 2026, Pure Sunfarms leaned further into a two-category barbell: Flower held 66.89% share despite a 5.48% year-over-year decline and a 3.70% month-over-month dip, while Pre-Roll rose to 32.87% share on 16.35% year-over-year growth and 9.04% month-over-month growth. Vapor Pens remained a rounding error at 0.23% share, but the month-over-month spike of 3,378.21% off a small base contrasts with an 11.68% year-over-year decline, indicating testing rather than scale. With average price up 17.22% year over year to $33.51 and the brand ranked 1 in Flower in Alberta, the pattern implies Pure Sunfarms is trading price for mix: defending Flower leadership while using faster Pre-Roll growth to offset softening Flower velocities.

The mix shift implies positioning anchored in value Flower leadership complemented by momentum in Pre-Roll, not diversification into new form factors: Flower’s rank of 1 in Alberta coexists with a 5.48% year-over-year contraction and 3.70% month-over-month dip, while Pre-Roll’s 16.35% year-over-year and 9.04% month-over-month gains lift overall growth without displacing Flower’s 66.89% share. The 17.22% year-over-year average price increase alongside a 0.23% Vapor Pens share and an 11.68% year-over-year decline in that segment suggests pricing power is being exercised where the brand has equity (Flower and Pre-Roll) rather than stretched into Vapor Pens, so the brand’s competitive posture is to consolidate top-of-funnel Flower buyers and convert them into Pre-Roll loyalists to sustain June 2026 brand sales growth of 62.41% year over year despite a 24‑month decline of 7.38%.

Competitive Landscape

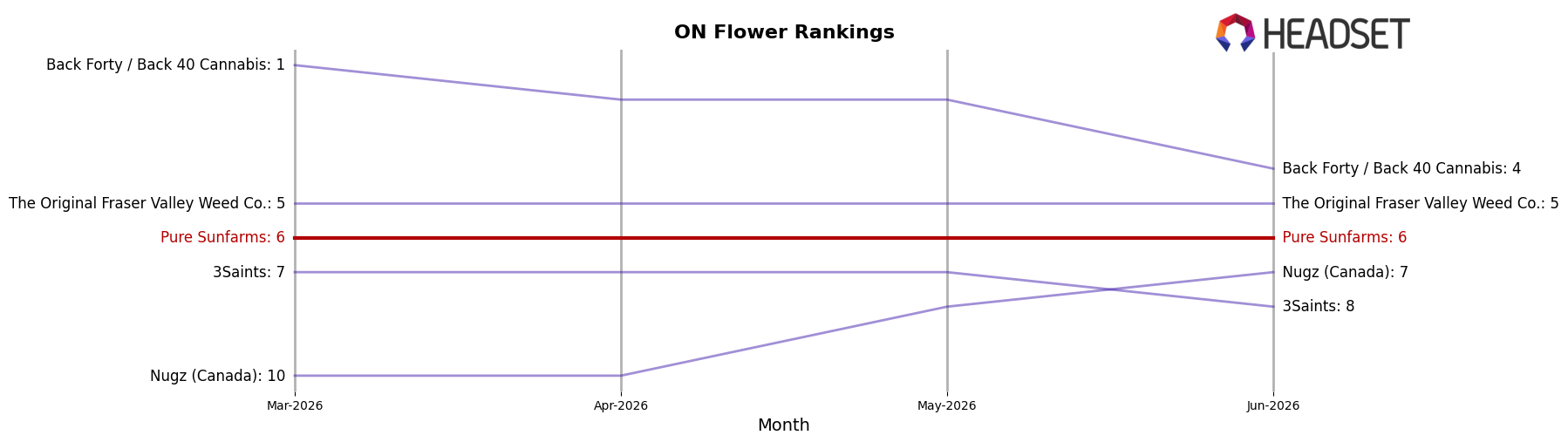

Pure Sunfarms is currently ranked #6 in ON Flower in June 2026, slipping 1 position year over year from #5, and holding flat versus March 2026 at #6, which contrasts with a prior peak at #4 in April 2025. Competitive pressure intensified as Spinach climbed from #4 to #1 with +38.3% YoY sales growth, while Back Forty / Back 40 Cannabis fell from #1 to #4 with an -11.3% YoY sales decline, and The Original Fraser Valley Weed Co. rose from #8 to #5 with +26.5% YoY growth. The combination of a 1-rank YoY slide and a 2-rank gap to Pure Sunfarms’ April 2025 peak implies the brand is being out-accelerated by faster-moving peers at the top, making near-term share gains contingent on recapturing momentum against incumbents that are gaining ranks and those that are retrenching.

Notable Products

Blue Dream#16 Pre-Roll 10-Pack (3.5g) posted the steepest decline at -10.2% month over month while slipping to rank 9, whereas West Coast Classics - Blue Dream and Pink Kush Pre-Roll 10-Pack (5g) surged +42.5% to rank 5, signaling a rotation within the pre-roll lineup rather than category weakness. Pink Kush Pre-Roll 10-Pack (3g) held rank 1 with a +3.5% lift as Pink Kush (3.5g) dipped -1.5% at rank 2, and Pink Kush (7g) fell -4.6% at rank 4, indicating the brand is consolidating demand toward pre-roll formats even as core flower sizes soften. Four of the top ten are Pink Kush SKUs and five of the top ten are Pre-Roll SKUs, and the combination of a -10.2% drag on Blue Dream#16 with a +42.5% gain on the West Coast Classics variant implies portfolio cannibalization that favors multi-strain and value-driven packs over single-strain iterations. The pattern suggests Pure Sunfarms is tilting commercial focus toward pre-roll-led Pink Kush franchises and curated blends to capture repeat buyers, while de-emphasizing mid-size flower where momentum is negative.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.