Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Plug Play is stocked at 718 licensed dispensaries across California, New York, and 3 other states, 607 of them in California, with the deepest coverage in Los Angeles, San Diego, Santa Ana, Long Beach, and Santa Rosa. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

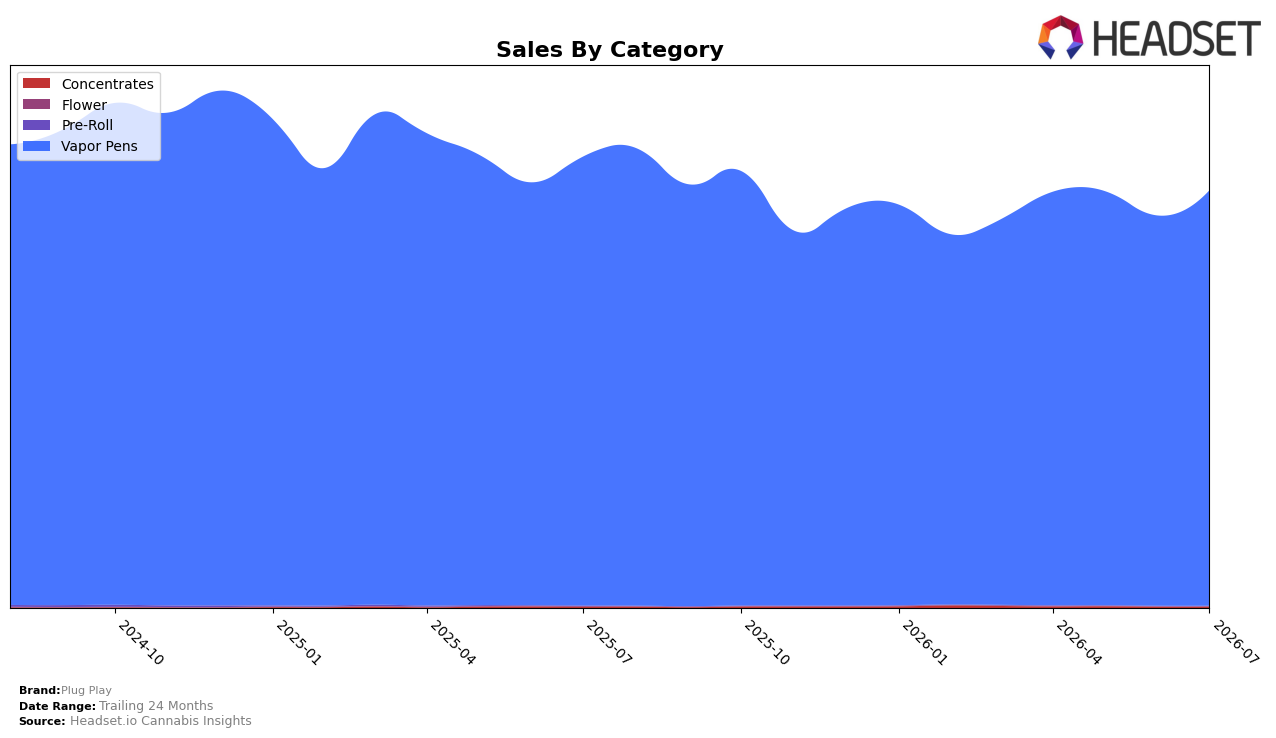

Plug Play concentrated 99.77% share in Vapor Pens during July 2026, with the residual 0.23% in Concentrates, indicating an extreme category focus. Within Vapor Pens, year-over-year sales fell 7.49% while month-over-month sales rose 6.47%, pairing a 13.39% YoY drop in average price to $27.70 with a short-term volume-led rebound; Concentrates moved the opposite direction in scale but posted 22.45% YoY growth and 4.47% MoM growth off a small base. In California Vapor Pens, Plug Play sat at rank 4, which combined with the mixed YoY/MoM pattern implies share is defended through pricing and near-term velocity, but long-run category dependence raises exposure if the Vapor Pens downtrend persists.

The July 2026 mix signals positioning as a single-category specialist in Vapor Pens (99.77% share) with price elasticity driving recent MoM gains (6.47%) despite YoY contraction (-7.49%), while the nascent Concentrates presence (0.23% share, +22.45% YoY) functions more as optionality than a hedge. Given rank 4 in California Vapor Pens and a 13.39% YoY price decline, the brand’s stance aligns with value-seeking consumers, implying that sustained competitiveness will depend on maintaining below-category price points to convert MoM momentum into stable share while selectively scaling Concentrates to mitigate category-specific risk.

Competitive Landscape

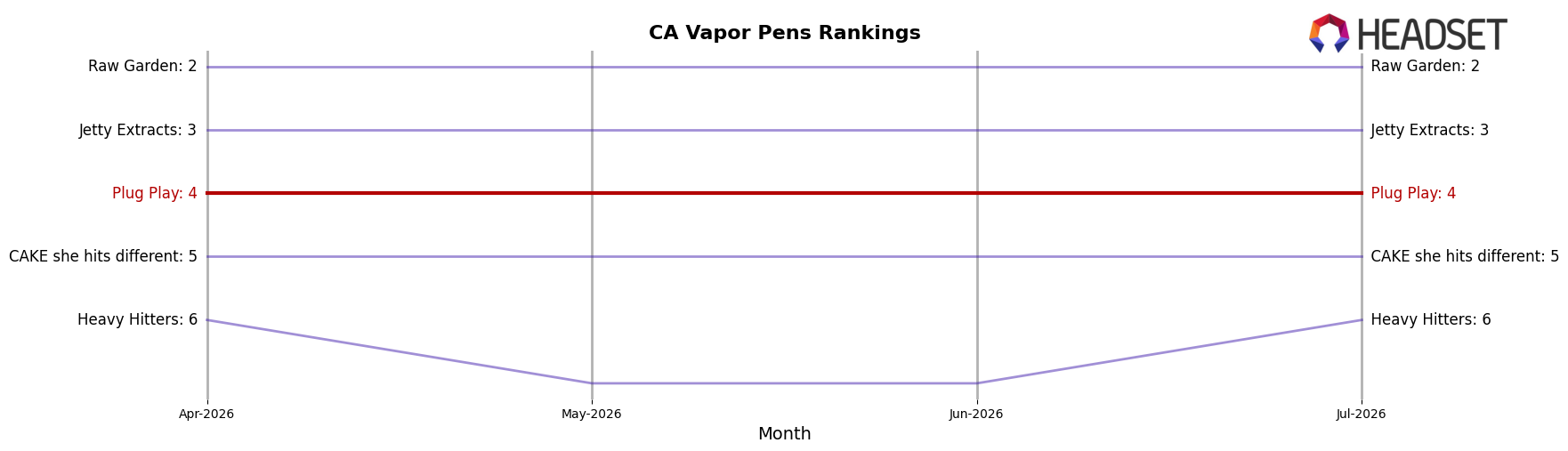

Plug Play sits at rank #4 in CA Vapor Pens in July 2026, down one spot from #3 year over year, with no change from April 2026 when it also held #4; compared with its category peak of #2 in February 2025, this two-position slide since peak contrasts with Jetty Extracts moving up from #4 to #3 and STIIIZY holding #1 despite a -6.8% year-over-year sales change. Against Raw Garden steady at #2 with +4.6% year-over-year growth, Plug Play’s flat three-month rank at #4 and year-over-year decline in rank by one position imply a consolidation phase where relative momentum has shifted toward faster risers, pressuring Plug Play to defend share rather than regain its former #2 slot.

Notable Products

Exotics - Berry Gang Distillate Plug (1g) posted the steepest decline in July 2026 at -15.7% MoM while holding rank 7, contrasting with Exotics - Melon Dew Distillate Plug (1g) up 39.5% MoM at rank 1 and DNA - Blue Dream Distillate Plug (1g) up 12.2% at rank 2. Eight of the top ten are Vapor Pens under the Exotics or DNA families, and the top four ranks are all Exotics or DNA SKUs, which indicates Plug Play is consolidating share within its own flavor-led sub-lines rather than diversifying. With Melon Dew generating $312,320 alongside Peach Ringz up 21.5% at rank 4, the momentum is skewed toward fruit-forward Exotics while a single laggard exposes flavor-cycling risk. The pattern implies Plug Play’s commercial direction leans into a few high-velocity Exotics flagships to anchor rank, accepting volatility in secondary SKUs to keep the line fresh.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.